What is Piezoelectric Ceramics - Global Market?

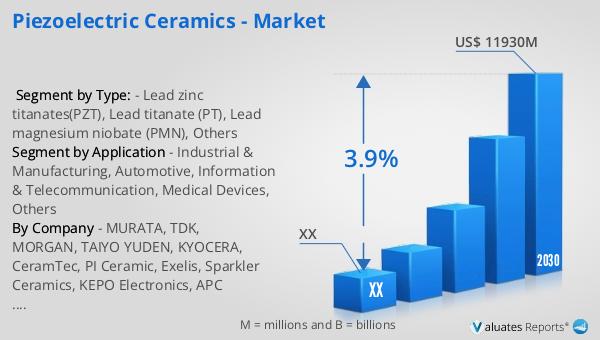

The global market for Piezoelectric Ceramics, a specialized sector within the broader ceramics industry, focuses on materials that exhibit piezoelectricity. These materials generate an electrical charge in response to mechanical stress and conversely, can mechanically deform when an electric field is applied. This unique property makes piezoelectric ceramics indispensable in a variety of applications, from electronic devices to industrial machinery. As of 2023, the market was valued at approximately US$ 9096 million, showcasing the significant demand and reliance industries have on these materials. With advancements in technology and an increasing array of applications, the market is projected to grow to US$ 11930 million by 2030, expanding at a compound annual growth rate (CAGR) of 3.9% during the forecast period from 2024 to 2030. This growth trajectory underscores the evolving nature of the market and the continuous innovation within the field. The market is somewhat concentrated, with the top three players holding about 35% of the global shares, indicating a competitive yet somewhat consolidated market landscape. Among the various types of piezoelectric ceramics, Lead magnesium niobate (PMN) emerges as the predominant variant, accounting for roughly 45% of the market. This preference is attributed to PMN's superior piezoelectric properties and versatility in applications. The Information & Telecommunication sector emerges as the primary application area, absorbing about 30% of the piezoelectric ceramics produced, which highlights the critical role these materials play in modern communication infrastructures.

Lead zinc titanates(PZT), Lead titanate (PT), Lead magnesium niobate (PMN), Others in the Piezoelectric Ceramics - Global Market:

Piezoelectric ceramics, a cornerstone of the global market, are categorized into several types based on their chemical composition and piezoelectric properties. Among these, Lead Zirconate Titanate (PZT), Lead Titanate (PT), and Lead Magnesium Niobate (PMN) are the most prominent, each serving distinct sectors due to their unique characteristics. PZT, known for its high piezoelectric constants and electromechanical coupling coefficients, is widely used in sensors, actuators, and transducers, making it a staple in both industrial and consumer electronics. Lead Titanate (PT), with its high Curie temperature and excellent ferroelectric properties, finds applications in high-temperature environments, serving as a critical component in devices operating under extreme conditions. Lead Magnesium Niobate (PMN), distinguished by its high dielectric constant and superior piezoelectric response at elevated temperatures, is predominantly used in precision actuators and optical devices. These materials, each with their specific advantages, cater to a broad spectrum of applications, from automotive to telecommunications, and from medical devices to defense systems. The versatility and adaptability of these ceramics have propelled the global market, ensuring their integral role in the advancement of modern technology and industry. The continuous research and development in this field aim to enhance the properties of these ceramics further, promising even broader applications and efficiency in the future.

Industrial & Manufacturing, Automotive, Information & Telecommunication, Medical Devices, Others in the Piezoelectric Ceramics - Global Market:

Piezoelectric ceramics find extensive usage across various sectors, including Industrial & Manufacturing, Automotive, Information & Telecommunication, Medical Devices, among others, due to their unique ability to convert mechanical stress into electrical signals and vice versa. In the Industrial & Manufacturing sector, these ceramics are pivotal in precision machining, vibration monitoring, and as components in ultrasonic equipment. The Automotive industry leverages piezoelectric materials for sensors and actuators that enhance vehicle performance, safety, and comfort. Information & Telecommunication relies on these ceramics for filters, resonators, and actuators, playing a crucial role in the functionality and reliability of communication devices. In the realm of Medical Devices, piezoelectric ceramics are instrumental in diagnostic equipment such as ultrasound machines, enabling non-invasive procedures and advancing healthcare delivery. Other applications include consumer electronics, where they contribute to the miniaturization and efficiency of devices, and in energy harvesting, where they offer potential for converting mechanical energy from vibrations into electrical energy, presenting a sustainable energy solution. The versatility and efficiency of piezoelectric ceramics across these diverse sectors underscore their significance in the global market, driving innovation and technological advancement.

Piezoelectric Ceramics - Global Market Outlook:

The outlook for the Piezoelectric Ceramics global market is promising, with a valuation of US$ 9096 million in 2023, and an anticipated growth to US$ 11930 million by 2030. This projection indicates a steady compound annual growth rate (CAGR) of 3.9% from 2024 to 2030. Such growth is reflective of the increasing demand for piezoelectric ceramics across various applications and industries. The market is characterized by a moderate level of concentration, with the top three players holding around 35% of the global shares, suggesting a competitive environment with significant room for innovation and expansion. Lead Magnesium Niobate (PMN) stands out as the predominant type of piezoelectric ceramic, making up about 45% of the market. This dominance is attributed to PMN's superior piezoelectric properties, which make it highly sought after for a wide range of applications. The Information & Telecommunication sector, in particular, emerges as a major consumer, accounting for approximately 30% of the market's demand. This highlights the critical role of piezoelectric ceramics in supporting and advancing communication technologies, further emphasizing the material's importance in the modern digital landscape. The market's growth trajectory and sectoral distribution underscore the ongoing relevance and potential of piezoelectric ceramics in addressing the needs of an increasingly technologically driven world.

| Report Metric | Details |

| Report Name | Piezoelectric Ceramics - Market |

| Forecasted market size in 2030 | US$ 11930 million |

| CAGR | 3.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | MURATA, TDK, MORGAN, TAIYO YUDEN, KYOCERA, CeramTec, PI Ceramic, Exelis, Sparkler Ceramics, KEPO Electronics, APC International, TRS, Noliac, SensorTech, Meggitt Sensing, Johnson Matthey, Kinetic Ceramics, Konghong Corporation, Jiakang Electronics, Datong Electronic, Audiowell, Honghua Electronic, Risun Electronic, Yuhai Electronic Ceramic, PANT |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |