What is Global Wafer Shipment Containers Market?

The Global Wafer Shipment Containers Market is a specialized segment within the semiconductor industry, focusing on the packaging and transportation of silicon wafers. These wafers are thin slices of semiconductor material, such as silicon, used in the fabrication of integrated circuits and other microdevices. The market for wafer shipment containers is crucial because it addresses the need for safe and secure transportation of these delicate wafers from manufacturers to assembly plants and various research facilities around the world. The containers are designed to protect the wafers from physical damage and contamination, which can compromise the integrity of the semiconductor devices. As the semiconductor industry continues to grow, driven by increasing demand for electronic devices, the need for efficient and reliable wafer shipment solutions becomes more pronounced. This market encompasses a range of products, including single wafer carriers, multi-wafer shipping boxes, and other specialized containers, each tailored to accommodate different sizes and quantities of wafers. The focus on innovation and technological advancement in wafer shipment solutions is aimed at enhancing the safety, efficiency, and cost-effectiveness of semiconductor logistics.

FOUP, FOSB in the Global Wafer Shipment Containers Market:

In the realm of the Global Wafer Shipment Containers Market, FOUP (Front Opening Unified Pod) and FOSB (Front Opening Shipping Box) stand out as pivotal components. FOUPs are specialized containers designed to transport and store 300mm wafers in a highly controlled environment, safeguarding them from contamination and physical damage. These containers are equipped with advanced features such as a purging system to maintain a particle-free atmosphere and an interface for automated handling systems, making them integral to modern semiconductor manufacturing facilities. On the other hand, FOSB containers are used for the shipment of both 200mm and 300mm wafers, offering a cost-effective solution for transporting wafers between manufacturing sites. FOSBs are designed to be stackable and durable, providing protection against environmental contaminants and physical shocks during transit. Both FOUPs and FOSBs play critical roles in the semiconductor supply chain, ensuring the safe and efficient movement of wafers, which are the foundational elements of all semiconductor devices. The evolution of these containers reflects the industry's ongoing efforts to improve wafer handling and logistics, addressing the growing demands for higher capacity, better contamination control, and increased compatibility with automated handling systems. As the semiconductor industry continues to advance, the development of more sophisticated wafer shipment containers, including FOUPs and FOSBs, remains a key focus area, driving innovations that align with the scaling needs of global semiconductor production.

300 mm Wafer, 200 mm Wafer in the Global Wafer Shipment Containers Market:

The usage of Global Wafer Shipment Containers in the semiconductor industry, particularly for 300mm and 200mm wafers, is a testament to the critical role these containers play in the safe and efficient transport of silicon wafers. For 300mm wafers, which are larger and used in the production of more advanced semiconductor devices, the containers are designed to offer enhanced protection against contamination and physical damage. This is crucial because any defect on the wafer surface can lead to significant yield losses during the chip manufacturing process. The containers used for 300mm wafers often feature advanced materials and sealing technologies to create a controlled environment that minimizes the risk of contamination. On the other hand, 200mm wafers, while smaller and used in less advanced applications, still require meticulous handling to maintain the integrity of the semiconductor devices they will become. The containers for 200mm wafers are designed to be robust and cost-effective, providing secure transportation while accommodating the slightly different handling requirements of these wafers. Both types of containers are integral to the logistics of semiconductor manufacturing, enabling the global distribution of wafers to fabrication plants and ensuring that the delicate wafers arrive in pristine condition, ready for the next stage of the semiconductor production process. The ongoing development and refinement of wafer shipment containers reflect the industry's commitment to quality and efficiency, addressing the evolving needs of semiconductor manufacturing with innovative packaging solutions.

Global Wafer Shipment Containers Market Outlook:

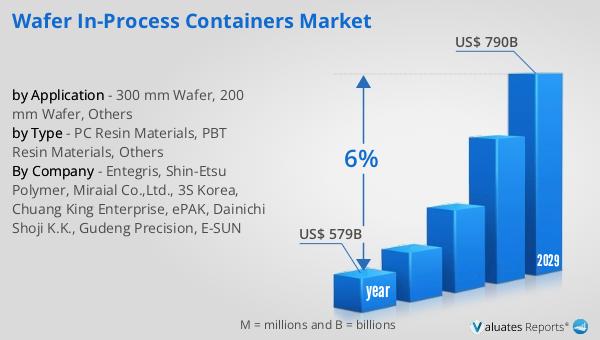

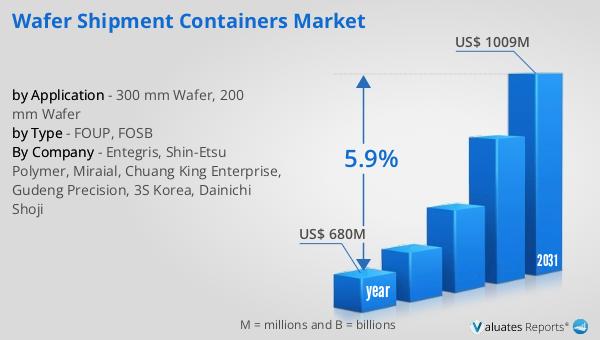

The market outlook for the Global Wafer Shipment Containers Market presents a promising future, with the market's value estimated at US$ 703 million in 2023, and projections suggesting growth to US$ 910.3 million by 2030. This anticipated growth, at a compound annual growth rate (CAGR) of 5.9% during the forecast period from 2024 to 2030, underscores the increasing demand and significance of wafer shipment containers in the semiconductor industry. Taiwan emerges as a major player in this market, accounting for nearly 19.75% of the global consumption of wafer cassettes in 2022, highlighting its pivotal role in the semiconductor manufacturing sector. Furthermore, the market is characterized by a high concentration of key players, with the top five companies collectively holding a staggering 96.32% of the global market share. This dominance by a few companies indicates a competitive landscape where innovation, quality, and efficiency are paramount. The growth and strategic positioning within the Global Wafer Shipment Containers Market reflect the critical importance of these containers in ensuring the safe and efficient transport of semiconductor wafers, a fundamental component of the global electronics and technology industry.

| Report Metric | Details |

| Report Name | Wafer Shipment Containers Market |

| Accounted market size in 2023 | US$ 703 million |

| Forecasted market size in 2030 | US$ 910.3 million |

| CAGR | 5.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Entegris, Shin-Etsu Polymer, Miraial, Chuang King Enterprise, Gudeng Precision, 3S Korea, Dainichi Shoji |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |