What is Global ALD and CVD Precursors for Semiconductor Market?

The global ALD and CVD precursors for the semiconductor market represent a critical segment in the semiconductor manufacturing industry. ALD (Atomic Layer Deposition) and CVD (Chemical Vapor Deposition) are advanced techniques used to deposit thin films on semiconductor wafers, which are essential for creating integrated circuits and other semiconductor devices. These precursors are specialized chemicals that react to form the desired thin films with high precision and uniformity. The market for these precursors is driven by the increasing demand for smaller, more efficient, and more powerful electronic devices. As technology advances, the need for high-quality, reliable, and efficient deposition processes becomes even more crucial, making ALD and CVD precursors indispensable in the semiconductor manufacturing process. The market is characterized by continuous innovation and development to meet the evolving needs of the semiconductor industry, ensuring that the latest devices can be produced with the highest standards of performance and reliability.

ALD Precursors, CVD Precursors in the Global ALD and CVD Precursors for Semiconductor Market:

ALD precursors are specialized chemicals used in the Atomic Layer Deposition process, which is a technique for depositing thin films one atomic layer at a time. This method allows for precise control over film thickness and composition, making it ideal for applications requiring high uniformity and conformality, such as in semiconductor manufacturing. ALD precursors typically include metal-organic compounds, metal halides, and other reactive gases that can form thin films through surface reactions. On the other hand, CVD precursors are used in the Chemical Vapor Deposition process, where thin films are formed through chemical reactions between gaseous precursors and the substrate surface. CVD precursors can include a wide range of chemicals, such as silanes, metal-organic compounds, and hydrides, depending on the desired film properties. Both ALD and CVD precursors are essential for creating high-performance semiconductor devices, as they enable the deposition of materials with excellent electrical, optical, and mechanical properties. The global market for these precursors is driven by the increasing demand for advanced electronic devices, such as smartphones, tablets, and wearable technology, which require high-quality thin films for their operation. Additionally, the growing adoption of the Internet of Things (IoT) and the expansion of 5G networks are further fueling the demand for ALD and CVD precursors, as these technologies rely on advanced semiconductor components. The market is also characterized by ongoing research and development efforts to improve the performance and efficiency of ALD and CVD processes, leading to the introduction of new and innovative precursors. As a result, the global ALD and CVD precursors market is expected to continue growing, driven by the need for high-performance semiconductor devices and the continuous advancement of deposition technologies.

Integrated Circuit Chip, Flat Panel Display, Solar Photovoltaic, others in the Global ALD and CVD Precursors for Semiconductor Market:

The usage of global ALD and CVD precursors for the semiconductor market spans several key areas, including integrated circuit chips, flat panel displays, solar photovoltaics, and other applications. In the realm of integrated circuit chips, ALD and CVD precursors are crucial for depositing thin films that form the various layers of the chip, such as the gate oxide, interconnects, and passivation layers. These thin films are essential for the chip's performance, reliability, and power efficiency. The precise control offered by ALD and CVD processes ensures that the films have the required thickness, uniformity, and composition, which is critical for the miniaturization and enhanced functionality of modern integrated circuits. In flat panel displays, ALD and CVD precursors are used to deposit thin films that form the active layers of the display, such as the thin-film transistors (TFTs) and the transparent conductive oxides (TCOs). These films are essential for the display's performance, including its brightness, contrast, and response time. The high uniformity and conformality of ALD and CVD films ensure that the displays have consistent performance across the entire panel, which is crucial for high-resolution and large-size displays. In the solar photovoltaic industry, ALD and CVD precursors are used to deposit thin films that form the active layers of solar cells, such as the absorber layer, buffer layer, and transparent conductive oxide layer. These films are essential for the solar cell's efficiency in converting sunlight into electricity. The precise control offered by ALD and CVD processes ensures that the films have the required thickness, composition, and uniformity, which is critical for achieving high conversion efficiencies. Additionally, ALD and CVD precursors are used in other applications, such as in the production of sensors, MEMS devices, and advanced packaging. In these applications, the thin films deposited using ALD and CVD processes provide the necessary electrical, optical, and mechanical properties required for the device's performance. Overall, the usage of global ALD and CVD precursors in these areas highlights their importance in enabling the production of high-performance semiconductor devices and advanced electronic components.

Global ALD and CVD Precursors for Semiconductor Market Outlook:

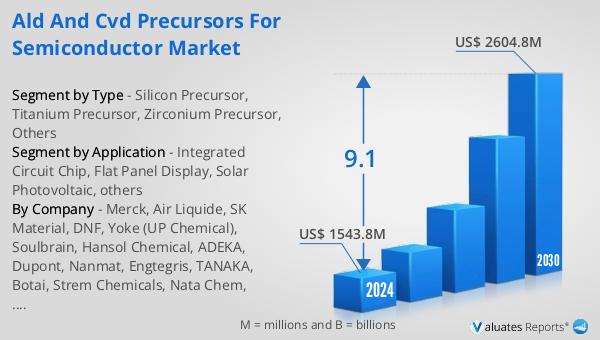

The global ALD and CVD precursors for the semiconductor market were valued at approximately US$ 1,324 million in 2023 and are projected to reach around US$ 2,603.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 9.1% during the forecast period from 2024 to 2030. Additionally, the market was estimated at US$ 1,543.80 million in 2023 and is expected to grow to a revised size of US$ 2,604.57 million by 2029, with a CAGR of 9.11% during the forecast period from 2023 to 2029. In 2022, the top five players in the global market held a significant share of approximately 82.08% in terms of revenue. This data underscores the robust growth and increasing importance of ALD and CVD precursors in the semiconductor industry, driven by the continuous demand for advanced electronic devices and the ongoing advancements in deposition technologies.

| Report Metric | Details |

| Report Name | ALD and CVD Precursors for Semiconductor Market |

| Accounted market size in 2023 | US$ 1324 million |

| Forecasted market size in 2030 | US$ 2603.5 million |

| CAGR | 9.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Merck, Air Liquide, SK Material, DNF, Yoke (UP Chemical), Soulbrain, Hansol Chemical, ADEKA, Dupont, Nanmat, Engtegris, TANAKA, Botai, Strem Chemicals, Nata Chem, Gelest, Adchem-tech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |