What is Global SCARA Material Handling Robot Market?

The Global SCARA Material Handling Robot Market is a dynamic segment within the broader field of industrial automation. SCARA stands for Selective Compliance Assembly Robot Arm, a type of robot known for its speed, precision, and efficiency in handling tasks. These robots are particularly adept at performing pick-and-place tasks, assembly operations, and packaging, making them invaluable in various industries. The market for these robots is driven by the increasing demand for automation in manufacturing processes to enhance productivity and reduce labor costs. As industries strive for higher efficiency and precision, SCARA robots offer a compelling solution due to their ability to perform repetitive tasks with high accuracy. The market is also influenced by technological advancements, such as improved sensors and software, which enhance the capabilities of these robots. Additionally, the growing trend towards smart factories and Industry 4.0 is propelling the adoption of SCARA robots, as they can be easily integrated into automated systems. Overall, the Global SCARA Material Handling Robot Market is poised for growth as industries continue to seek innovative solutions to optimize their operations.

< 5 Kg, 5 - 10 Kg, > 10 Kg in the Global SCARA Material Handling Robot Market:

In the Global SCARA Material Handling Robot Market, robots are categorized based on their payload capacity, which refers to the maximum weight they can handle. This classification is crucial as it determines the suitability of a robot for specific tasks and industries. The first category, robots with a payload capacity of less than 5 Kg, is typically used for light-duty tasks. These robots are ideal for applications that require high speed and precision but involve handling small and lightweight items. Industries such as electronics and pharmaceuticals often utilize these robots for tasks like assembling small components or packaging delicate products. Their compact size and agility make them perfect for environments where space is limited, and precision is paramount. The second category includes robots with a payload capacity ranging from 5 to 10 Kg. These robots strike a balance between speed and strength, making them versatile for a variety of applications. They are commonly used in industries like automotive and food processing, where they handle tasks such as assembling medium-sized components or packaging products. Their ability to handle moderate weights without compromising on speed makes them a popular choice for manufacturers looking to enhance productivity. The third category consists of robots with a payload capacity of more than 10 Kg. These robots are designed for heavy-duty tasks and are often employed in industries such as metal and machinery, where they handle large and heavy components. Their robust design and powerful motors enable them to perform tasks that require significant force, such as welding or moving heavy parts. Despite their strength, these robots maintain a high level of precision, ensuring that even the most demanding tasks are completed accurately. In summary, the classification of SCARA robots based on payload capacity allows industries to select the right robot for their specific needs, ensuring optimal performance and efficiency.

Automotive, Chemical, Rubber and Plastic, Electrical and Electronics, Metal and Machinery, Food, Beverages and Pharmaceuticals, Others in the Global SCARA Material Handling Robot Market:

The Global SCARA Material Handling Robot Market finds extensive applications across various industries, each benefiting from the unique capabilities of these robots. In the automotive industry, SCARA robots are used for tasks such as assembling small parts, painting, and welding. Their speed and precision make them ideal for the high-paced environment of automotive manufacturing, where efficiency and accuracy are crucial. In the chemical industry, these robots handle hazardous materials, ensuring safety and reducing the risk of human exposure. Their ability to operate in harsh environments makes them indispensable for tasks such as mixing and packaging chemicals. The rubber and plastic industry also benefits from SCARA robots, which are used for tasks like injection molding and assembling plastic components. Their precision ensures that each product meets the required specifications, reducing waste and improving quality. In the electrical and electronics industry, SCARA robots are employed for assembling circuit boards and other delicate components. Their ability to handle small parts with high accuracy is essential for maintaining the quality and reliability of electronic products. The metal and machinery industry utilizes these robots for tasks such as welding, cutting, and assembling metal parts. Their strength and precision enable them to handle heavy components with ease, improving productivity and reducing labor costs. In the food, beverages, and pharmaceuticals industry, SCARA robots are used for packaging, sorting, and quality control. Their speed and hygiene make them ideal for handling food products and pharmaceuticals, ensuring that each product meets safety and quality standards. Finally, other industries, such as logistics and warehousing, also benefit from SCARA robots, which are used for tasks like sorting and transporting goods. Their versatility and efficiency make them a valuable asset in any industry looking to improve productivity and reduce costs.

Global SCARA Material Handling Robot Market Outlook:

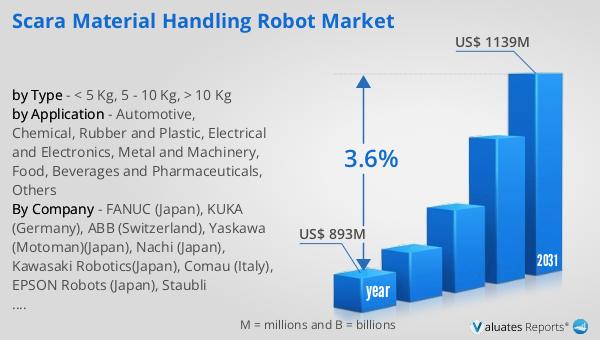

The outlook for the Global SCARA Material Handling Robot Market is promising, with significant growth anticipated in the coming years. In 2024, the market was valued at approximately US$ 893 million. By 2031, it is expected to expand to a revised size of around US$ 1139 million. This growth trajectory represents a compound annual growth rate (CAGR) of 3.6% over the forecast period. This steady growth can be attributed to several factors, including the increasing demand for automation across various industries and the ongoing advancements in robotic technology. As manufacturers continue to seek ways to enhance efficiency and reduce operational costs, the adoption of SCARA robots is likely to rise. These robots offer a compelling solution due to their ability to perform repetitive tasks with high speed and precision. Additionally, the trend towards smart factories and Industry 4.0 is expected to further drive the demand for SCARA robots, as they can be seamlessly integrated into automated systems. Overall, the Global SCARA Material Handling Robot Market is poised for growth, driven by the need for innovative solutions to optimize manufacturing processes and improve productivity.

| Report Metric | Details |

| Report Name | SCARA Material Handling Robot Market |

| Accounted market size in year | US$ 893 million |

| Forecasted market size in 2031 | US$ 1139 million |

| CAGR | 3.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | FANUC (Japan), KUKA (Germany), ABB (Switzerland), Yaskawa (Motoman)(Japan), Nachi (Japan), Kawasaki Robotics(Japan), Comau (Italy), EPSON Robots (Japan), Staubli (Switzerland), Omron Adept Technologies (US), DENSO Robotics (Japan), OTC Daihen (Japan), Toshiba (Japan), Mitsubishi Electric (Japan), Universal Robots (Denmark), Hyundai Robotics (Korea), Siasun (China), Anhui EFORT Intelligent Equipment (China), Estun Automation (China), Guangzhou CNC Equipment (China), STEP Electric Corporation (China) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |