What is Global Aluminium Dross Recycling Market?

The Global Aluminium Dross Recycling Market is an essential segment within the broader aluminum industry, focusing on the recovery and reuse of aluminum dross. Aluminum dross is a by-product of the aluminum smelting process, consisting of a mixture of aluminum metal and non-metallic materials. This market is driven by the increasing demand for sustainable and environmentally friendly practices in the aluminum industry. Recycling aluminum dross not only helps in reducing waste but also conserves energy and resources by recovering valuable aluminum content. The process involves separating the aluminum metal from the non-metallic components, which can then be reused in various applications. The market is witnessing growth due to the rising awareness of environmental issues and the need for efficient waste management solutions. Additionally, technological advancements in recycling processes are enhancing the efficiency and effectiveness of aluminum dross recycling, further propelling market growth. The global market for aluminum dross recycling is expected to expand as industries continue to prioritize sustainability and resource conservation. This market plays a crucial role in the circular economy by transforming waste into valuable resources, thereby contributing to environmental preservation and economic growth.

Primary Aluminium Dross, Secondary Aluminium Dross in the Global Aluminium Dross Recycling Market:

Primary aluminum dross and secondary aluminum dross are two distinct types of dross generated during the aluminum production process. Primary aluminum dross is produced during the initial smelting of aluminum, where raw aluminum ore is processed to extract pure aluminum metal. This type of dross contains a higher percentage of aluminum content, making it more valuable for recycling purposes. The recycling of primary aluminum dross involves processes such as milling, screening, and melting to recover the aluminum metal. The recovered aluminum can then be used in various applications, including the production of new aluminum products. On the other hand, secondary aluminum dross is generated during the recycling of aluminum scrap. This type of dross contains a lower percentage of aluminum content compared to primary dross, as it is derived from previously used aluminum products. The recycling process for secondary aluminum dross involves similar steps as primary dross, but with additional challenges due to the presence of impurities and contaminants. Despite these challenges, the recycling of secondary aluminum dross is crucial for maximizing resource efficiency and minimizing waste. Both primary and secondary aluminum dross recycling contribute significantly to the global aluminum dross recycling market by providing a sustainable solution for aluminum waste management. The market for aluminum dross recycling is driven by the increasing demand for aluminum products across various industries, including automotive, construction, and packaging. As the demand for aluminum continues to rise, the need for efficient recycling solutions becomes more critical. The recycling of aluminum dross not only helps in reducing the environmental impact of aluminum production but also provides economic benefits by recovering valuable aluminum content. Technological advancements in recycling processes are enhancing the efficiency and effectiveness of aluminum dross recycling, making it a viable solution for sustainable resource management. The global aluminum dross recycling market is expected to grow as industries continue to prioritize sustainability and resource conservation. This market plays a crucial role in the circular economy by transforming waste into valuable resources, thereby contributing to environmental preservation and economic growth. The recycling of primary and secondary aluminum dross is essential for achieving a sustainable aluminum industry and reducing the environmental impact of aluminum production. By recovering valuable aluminum content from dross, the industry can reduce its reliance on raw materials and minimize waste generation. The global aluminum dross recycling market is poised for growth as industries continue to adopt sustainable practices and prioritize resource efficiency. This market is an integral part of the aluminum industry, providing a sustainable solution for aluminum waste management and contributing to the circular economy.

Alumina, Aluminium Ingot, Construction Material, others in the Global Aluminium Dross Recycling Market:

The Global Aluminium Dross Recycling Market finds its usage in various areas, including alumina, aluminum ingot, construction material, and others. In the alumina sector, recycled aluminum dross is used as a raw material for producing alumina, which is a key component in the production of aluminum metal. The recycling of aluminum dross for alumina production helps in reducing the reliance on bauxite, the primary raw material for alumina, thereby conserving natural resources and reducing environmental impact. In the aluminum ingot sector, recycled aluminum dross is used to produce aluminum ingots, which are then used in various applications, including automotive, aerospace, and packaging. The use of recycled aluminum dross in ingot production helps in reducing energy consumption and greenhouse gas emissions, as recycling aluminum requires significantly less energy compared to primary aluminum production. In the construction material sector, recycled aluminum dross is used as an additive in the production of construction materials, such as cement and concrete. The use of aluminum dross in construction materials enhances the properties of the materials, such as strength and durability, while also providing a sustainable solution for waste management. Additionally, the use of recycled aluminum dross in construction materials helps in reducing the environmental impact of construction activities by minimizing waste generation and conserving natural resources. In other areas, recycled aluminum dross is used in the production of various products, including abrasives, refractories, and chemicals. The use of recycled aluminum dross in these applications provides a sustainable solution for waste management and resource conservation. The global aluminum dross recycling market is driven by the increasing demand for sustainable and environmentally friendly practices across various industries. As industries continue to prioritize sustainability and resource efficiency, the demand for recycled aluminum dross is expected to grow. The market for aluminum dross recycling plays a crucial role in the circular economy by transforming waste into valuable resources, thereby contributing to environmental preservation and economic growth. The recycling of aluminum dross not only helps in reducing the environmental impact of aluminum production but also provides economic benefits by recovering valuable aluminum content. Technological advancements in recycling processes are enhancing the efficiency and effectiveness of aluminum dross recycling, making it a viable solution for sustainable resource management. The global aluminum dross recycling market is poised for growth as industries continue to adopt sustainable practices and prioritize resource efficiency. This market is an integral part of the aluminum industry, providing a sustainable solution for aluminum waste management and contributing to the circular economy.

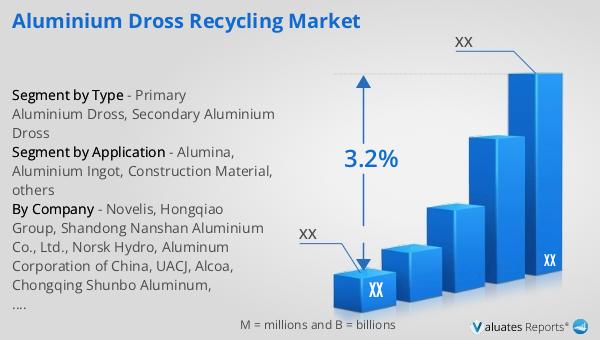

Global Aluminium Dross Recycling Market Outlook:

In 2024, the global market for aluminum dross recycling was valued at a certain amount in US dollars. Looking ahead, this market is anticipated to expand, reaching a new valuation by 2031. This growth trajectory is expected to follow a compound annual growth rate (CAGR) of 3.2% over the forecast period. This steady growth rate reflects the increasing importance of aluminum dross recycling in the global market. The market's expansion is driven by the rising demand for sustainable and environmentally friendly practices in the aluminum industry. As industries continue to prioritize sustainability and resource efficiency, the demand for recycled aluminum dross is expected to grow. The market for aluminum dross recycling plays a crucial role in the circular economy by transforming waste into valuable resources, thereby contributing to environmental preservation and economic growth. The recycling of aluminum dross not only helps in reducing the environmental impact of aluminum production but also provides economic benefits by recovering valuable aluminum content. Technological advancements in recycling processes are enhancing the efficiency and effectiveness of aluminum dross recycling, making it a viable solution for sustainable resource management. The global aluminum dross recycling market is poised for growth as industries continue to adopt sustainable practices and prioritize resource efficiency. This market is an integral part of the aluminum industry, providing a sustainable solution for aluminum waste management and contributing to the circular economy.

| Report Metric | Details |

| Report Name | Aluminium Dross Recycling Market |

| CAGR | 3.2% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Novelis, Hongqiao Group, Shandong Nanshan Aluminium Co., Ltd., Norsk Hydro, Aluminum Corporation of China, UACJ, Alcoa, Chongqing Shunbo Aluminum, Constellium, Hebei Sitong New Metal Material, Sigma Group, Huajin Aluminum, Ye Chiu |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |