What is Global Monitor Privacy Film Market?

The Global Monitor Privacy Film Market refers to the industry focused on producing and distributing privacy films for monitors. These films are designed to protect sensitive information displayed on screens from prying eyes. They work by limiting the viewing angle of the screen, so only the person directly in front of it can see the content clearly. This is particularly useful in environments where confidential information is frequently accessed, such as in offices, public spaces, and during travel. The market encompasses a variety of products tailored to different screen sizes and types, ensuring compatibility with a wide range of devices. As concerns about data privacy and security continue to grow, the demand for monitor privacy films is expected to increase, making this market a crucial component of the broader privacy and security industry.

11.6 Inches, 12.5 Inches, 13.3 Inches, 14 Inches, 14.1 Inches, 15.6 Inches, Others in the Global Monitor Privacy Film Market:

The Global Monitor Privacy Film Market includes products designed for various screen sizes, such as 11.6 inches, 12.5 inches, 13.3 inches, 14 inches, 14.1 inches, 15.6 inches, and others. Each size caters to specific devices, ensuring that users can find a privacy film that fits their monitor perfectly. For instance, 11.6-inch privacy films are commonly used for smaller laptops and portable devices, providing a compact solution for on-the-go privacy. The 12.5-inch and 13.3-inch films are popular among users of mid-sized laptops, offering a balance between portability and screen real estate. The 14-inch and 14.1-inch films cater to slightly larger laptops, often used by professionals who require more screen space for their work. The 15.6-inch films are designed for larger laptops and monitors, providing ample coverage for users who need a bigger display. Additionally, the market includes privacy films for other screen sizes, ensuring that all types of monitors, regardless of their dimensions, can benefit from enhanced privacy. These films are typically easy to install and remove, making them a convenient solution for users who need to protect their sensitive information. They are also available in various materials and finishes, such as matte and glossy, allowing users to choose a film that best suits their preferences and needs. The versatility and wide range of options available in the Global Monitor Privacy Film Market make it an essential resource for individuals and businesses looking to safeguard their digital information.

Online Sales, Offline Sales in the Global Monitor Privacy Film Market:

The usage of Global Monitor Privacy Film Market products can be categorized into two main areas: online sales and offline sales. Online sales refer to the purchase of privacy films through e-commerce platforms and websites. This method offers several advantages, such as convenience, a wide selection of products, and the ability to compare prices and read reviews from other customers. Online sales platforms often provide detailed product descriptions and specifications, helping customers make informed decisions. Additionally, online shopping allows customers to purchase privacy films from the comfort of their homes, without the need to visit physical stores. On the other hand, offline sales involve purchasing privacy films from brick-and-mortar stores, such as electronics retailers, office supply stores, and specialty shops. This method allows customers to physically inspect the products before making a purchase, ensuring that they choose the right size and type of film for their needs. Offline sales also provide the opportunity for customers to seek assistance from store staff, who can offer personalized recommendations and answer any questions. Both online and offline sales channels play a crucial role in the distribution of monitor privacy films, catering to different customer preferences and needs. The combination of these two sales methods ensures that privacy films are accessible to a wide range of users, from individual consumers to large organizations. As the demand for data privacy continues to grow, the Global Monitor Privacy Film Market is likely to see increased sales through both online and offline channels, further solidifying its importance in the privacy and security industry.

Global Monitor Privacy Film Market Outlook:

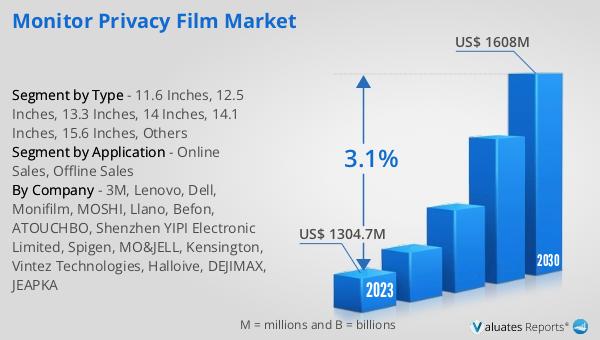

The global Monitor Privacy Film market was valued at US$ 1304.7 million in 2023 and is anticipated to reach US$ 1608 million by 2030, witnessing a CAGR of 3.1% during the forecast period 2024-2030. This market outlook highlights the steady growth expected in the industry over the coming years. The increasing awareness of data privacy and the need to protect sensitive information are key drivers of this growth. As more individuals and businesses recognize the importance of safeguarding their digital information, the demand for monitor privacy films is likely to rise. The projected growth rate of 3.1% CAGR indicates a consistent increase in market value, reflecting the ongoing expansion of the privacy and security sector. This positive market outlook underscores the significance of monitor privacy films in today's digital age, where data breaches and privacy concerns are becoming increasingly prevalent. The anticipated growth in the market value from US$ 1304.7 million in 2023 to US$ 1608 million by 2030 demonstrates the potential for continued innovation and development within the industry. As the market evolves, it is expected to introduce new and improved products that cater to the diverse needs of consumers and businesses alike.

| Report Metric | Details |

| Report Name | Monitor Privacy Film Market |

| Accounted market size in 2023 | US$ 1304.7 million |

| Forecasted market size in 2030 | US$ 1608 million |

| CAGR | 3.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | 3M, Lenovo, Dell, Monifilm, MOSHI, Llano, Befon, ATOUCHBO, Shenzhen YIPI Electronic Limited, Spigen, MO&JELL, Kensington, Vintez Technologies, Halloive, DEJIMAX, JEAPKA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |