What is Global Glass Fiber Reinforced Cable Trays and Ladders Market?

Global Glass Fiber Reinforced Cable Trays and Ladders Market refers to the industry focused on the production and distribution of cable management systems made from glass fiber reinforced plastics (GFRP). These systems are essential for supporting and organizing cables in various industrial and commercial settings. The use of glass fiber reinforcement provides these trays and ladders with enhanced strength, durability, and resistance to environmental factors such as corrosion, making them ideal for harsh environments. The market is driven by the increasing demand for reliable and efficient cable management solutions across various sectors, including construction, energy, and telecommunications. As industries continue to expand and modernize, the need for robust infrastructure to support complex wiring systems grows, thereby fueling the demand for GFRP cable trays and ladders. Additionally, the lightweight nature of these materials makes them easier to install and maintain compared to traditional metal alternatives, further boosting their popularity. The market is characterized by continuous innovation, with manufacturers focusing on developing products that offer improved performance and sustainability. As a result, the Global Glass Fiber Reinforced Cable Trays and Ladders Market is poised for significant growth in the coming years.

GRP Ladder Type, GRP Perforated Type, Other Types in the Global Glass Fiber Reinforced Cable Trays and Ladders Market:

The Global Glass Fiber Reinforced Cable Trays and Ladders Market encompasses various types of products, each designed to meet specific needs and applications. Among these, the GRP Ladder Type is a popular choice due to its robust construction and versatility. These ladder-type trays are designed to support heavy cable loads and are often used in environments where strength and durability are paramount. They are constructed with side rails and rungs, providing a ladder-like structure that offers excellent support and stability for cables. The GRP Ladder Type is particularly favored in industries such as oil and gas, where the infrastructure must withstand harsh conditions and heavy usage. Its design allows for easy installation and maintenance, making it a cost-effective solution for long-term cable management needs.

IT and Telecom, Manufacturing, Energy & Utility, Oil and Gas, Mining, Other in the Global Glass Fiber Reinforced Cable Trays and Ladders Market:

Another significant category within this market is the GRP Perforated Type. These trays feature a series of perforations or holes along their length, which serve multiple purposes. The perforations allow for better ventilation and heat dissipation, which is crucial in preventing overheating of cables, especially in high-density installations. This type of tray is often used in environments where thermal management is a concern, such as in data centers and telecommunications facilities. The perforated design also reduces the overall weight of the tray, making it easier to handle and install. Additionally, the open structure allows for flexibility in cable entry and exit points, providing a versatile solution for complex wiring systems. The GRP Perforated Type is valued for its balance of strength, weight, and functionality, making it a preferred choice in many industrial applications.

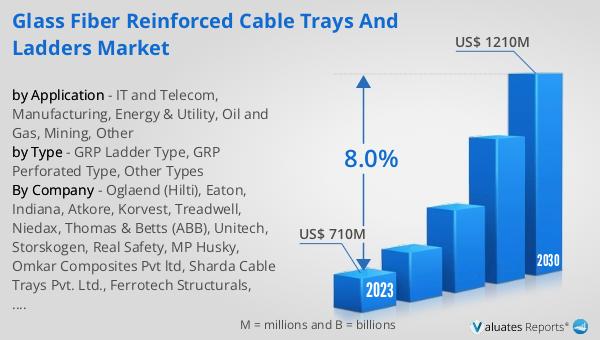

Global Glass Fiber Reinforced Cable Trays and Ladders Market Outlook:

Beyond these two primary types, the market also includes other variations designed to cater to specific requirements. These may include GRP channel trays, which offer a more enclosed structure for added protection against environmental factors, and GRP wire mesh trays, which provide a lightweight and flexible option for supporting smaller cable bundles. Each type of tray is engineered to deliver specific benefits, such as enhanced corrosion resistance, ease of installation, or improved load-bearing capacity. The diversity of products available in the Global Glass Fiber Reinforced Cable Trays and Ladders Market ensures that there is a suitable solution for virtually any cable management challenge. Manufacturers continue to innovate and expand their product offerings, incorporating advanced materials and design techniques to meet the evolving needs of their customers. As a result, the market remains dynamic and competitive, with a wide range of options available to end-users.

| Report Metric | Details |

| Report Name | Glass Fiber Reinforced Cable Trays and Ladders Market |

| Accounted market size in year | US$ 762 million |

| Forecasted market size in 2031 | US$ 1297 million |

| CAGR | 8.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Oglaend (Hilti), Eaton, Indiana, Atkore, Korvest, Treadwell, Niedax, Thomas & Betts (ABB), Unitech, Storskogen, Real Safety, MP Husky, Omkar Composites Pvt ltd, Sharda Cable Trays Pvt. Ltd., Ferrotech Structurals, Fiber Tech Composite Private Limited, Fibex, EPP Composites, ERCON Composites, Hebei Longxin, Jiansu Huapeng, Hebei Chuangye, Zhenjiang Shenlong, King Sitong, Legrand |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |