What is Global Electronic Grade Bismaleimide Market?

The Global Electronic Grade Bismaleimide Market is a specialized segment within the broader chemical industry, focusing on the production and distribution of bismaleimide compounds that meet the stringent purity and performance standards required for electronic applications. Bismaleimides are a class of thermosetting polymers known for their excellent thermal stability, mechanical strength, and electrical insulation properties. These characteristics make them highly suitable for use in high-performance electronic components and systems. The market is driven by the increasing demand for advanced electronic devices, which require materials that can withstand high temperatures and harsh operating conditions. As technology continues to evolve, the need for reliable and efficient materials like electronic grade bismaleimide is expected to grow. This market is characterized by ongoing research and development efforts aimed at enhancing the properties of bismaleimide compounds to meet the ever-changing requirements of the electronics industry. Manufacturers in this market are focused on developing innovative solutions that offer improved performance, cost-effectiveness, and environmental sustainability. The global reach of this market is facilitated by a network of suppliers and distributors who ensure the availability of high-quality bismaleimide products to customers worldwide.

Diphenyl Methane Type, Alkyldiphenyl Methane Type, Other in the Global Electronic Grade Bismaleimide Market:

In the Global Electronic Grade Bismaleimide Market, different types of bismaleimide compounds are utilized, each offering unique properties and benefits. The Diphenyl Methane Type is one of the most commonly used variants. It is known for its excellent thermal stability and mechanical strength, making it ideal for applications that require materials to withstand high temperatures and mechanical stress. This type of bismaleimide is often used in the production of printed circuit boards (PCBs) and other electronic components that demand high reliability and performance. The Alkyldiphenyl Methane Type, on the other hand, offers a different set of advantages. It is characterized by its enhanced flexibility and toughness, which are crucial for applications where materials need to endure repeated mechanical stress without cracking or breaking. This type is particularly useful in flexible electronics and wearable devices, where durability and resilience are key considerations. Other types of bismaleimide compounds are also available in the market, each tailored to meet specific application requirements. These may include variations with improved electrical insulation properties, enhanced chemical resistance, or reduced environmental impact. The diversity of bismaleimide types available in the market allows manufacturers to select the most appropriate material for their specific needs, ensuring optimal performance and reliability of their electronic products. The choice of bismaleimide type is often influenced by factors such as the intended application, operating environment, and cost considerations. As the electronics industry continues to advance, the demand for specialized bismaleimide compounds is expected to grow, driving further innovation and development in this market. Manufacturers are continually exploring new formulations and processing techniques to enhance the properties of bismaleimide compounds, ensuring they meet the evolving needs of the electronics industry. This ongoing innovation is essential for maintaining the competitiveness of the Global Electronic Grade Bismaleimide Market and supporting the development of next-generation electronic devices.

Chip Packaging, Mobile Phone, Web Server, Other in the Global Electronic Grade Bismaleimide Market:

The Global Electronic Grade Bismaleimide Market plays a crucial role in various applications, including chip packaging, mobile phones, web servers, and other electronic devices. In chip packaging, bismaleimide compounds are used to encapsulate and protect semiconductor chips from environmental factors such as moisture, dust, and mechanical stress. The excellent thermal stability and electrical insulation properties of bismaleimide make it an ideal material for this application, ensuring the reliability and longevity of the packaged chips. In mobile phones, bismaleimide is used in the production of printed circuit boards (PCBs) and other components that require high thermal and mechanical performance. The material's ability to withstand high temperatures and mechanical stress makes it suitable for use in the compact and densely packed environments of modern smartphones. In web servers, bismaleimide compounds are used in the production of high-performance electronic components that require reliable operation under demanding conditions. The material's excellent thermal and electrical properties ensure the efficient and reliable operation of web servers, which are critical for the functioning of the internet and digital communication networks. Other applications of bismaleimide in the electronics industry include its use in aerospace and automotive electronics, where its high-performance characteristics are essential for ensuring the safety and reliability of electronic systems. The versatility and performance of bismaleimide compounds make them a valuable material for a wide range of electronic applications, supporting the development of advanced technologies and devices. As the demand for high-performance electronic devices continues to grow, the Global Electronic Grade Bismaleimide Market is expected to expand, driven by the need for materials that can meet the stringent requirements of modern electronics. Manufacturers in this market are focused on developing innovative solutions that offer improved performance, cost-effectiveness, and environmental sustainability, ensuring the continued growth and success of the market.

Global Electronic Grade Bismaleimide Market Outlook:

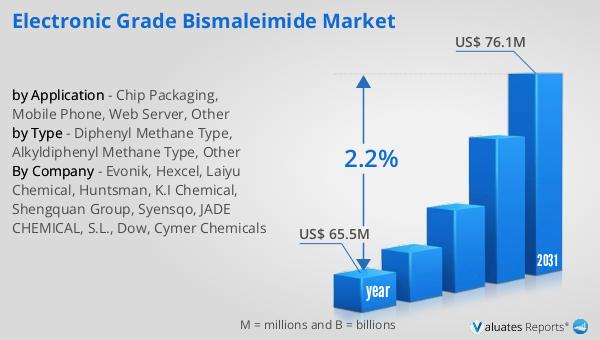

The global market for Electronic Grade Bismaleimide was valued at $65.5 million in 2024, with projections indicating it will reach approximately $76.1 million by 2031. This growth represents a compound annual growth rate (CAGR) of 2.2% over the forecast period. This steady increase in market size reflects the rising demand for high-performance materials in the electronics industry. As electronic devices become more advanced and complex, the need for materials that can withstand high temperatures and mechanical stress becomes increasingly important. Bismaleimide compounds, with their excellent thermal stability and mechanical strength, are well-suited to meet these demands. The market's growth is also driven by ongoing research and development efforts aimed at enhancing the properties of bismaleimide compounds to meet the evolving needs of the electronics industry. Manufacturers are continually exploring new formulations and processing techniques to improve the performance and cost-effectiveness of bismaleimide products. This focus on innovation is essential for maintaining the competitiveness of the Global Electronic Grade Bismaleimide Market and supporting the development of next-generation electronic devices. As the market continues to grow, it is expected to play a crucial role in the advancement of electronic technologies, providing the materials needed to support the development of more efficient, reliable, and sustainable electronic devices.

| Report Metric | Details |

| Report Name | Electronic Grade Bismaleimide Market |

| Accounted market size in year | US$ 65.5 million |

| Forecasted market size in 2031 | US$ 76.1 million |

| CAGR | 2.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Evonik, Hexcel, Laiyu Chemical, Huntsman, K.I Chemical, Shengquan Group, Syensqo, JADE CHEMICAL, S.L., Dow, Cymer Chemicals |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |