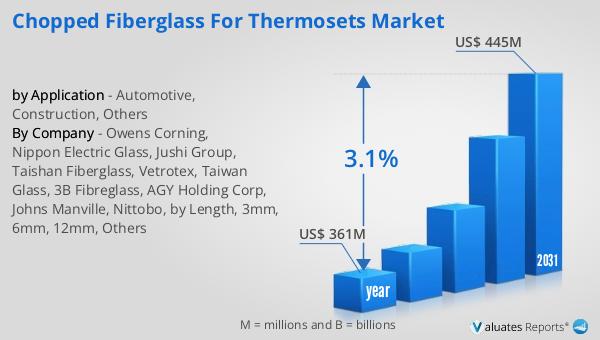

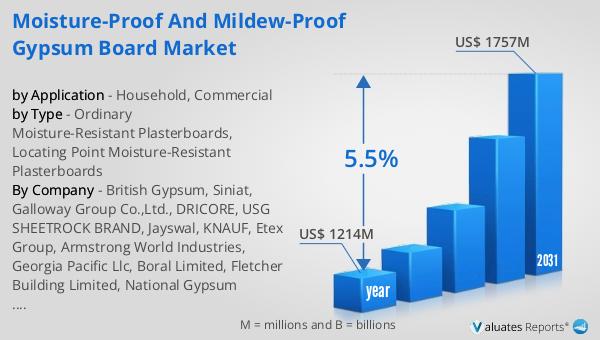

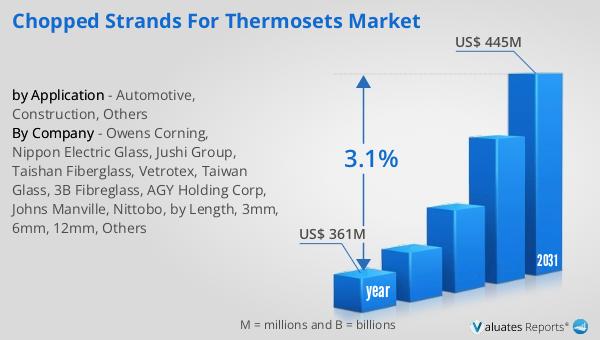

What is Global Chopped Fiberglass for Thermoplastics Market?

The Global Chopped Fiberglass for Thermoplastics Market is a specialized segment within the broader fiberglass industry, focusing on the production and application of chopped fiberglass strands used in thermoplastic composites. These composites are materials made by combining chopped fiberglass with thermoplastic resins, resulting in a product that boasts enhanced strength, durability, and resistance to various environmental factors. The market for these materials is driven by their increasing demand across multiple industries, including automotive, construction, and electronics, where they are used to improve the performance and longevity of products. Chopped fiberglass for thermoplastics is particularly valued for its lightweight nature, which contributes to energy efficiency and cost savings in manufacturing and product usage. The market is characterized by continuous innovation and development, as manufacturers strive to improve the properties of fiberglass composites to meet the evolving needs of end-users. This includes advancements in the production processes, as well as the development of new resin formulations that enhance the compatibility and performance of fiberglass composites. As industries continue to seek materials that offer a balance of strength, weight, and cost-effectiveness, the Global Chopped Fiberglass for Thermoplastics Market is poised for sustained growth and innovation.

10μm, 11μm, 13μm, Others in the Global Chopped Fiberglass for Thermoplastics Market:

In the Global Chopped Fiberglass for Thermoplastics Market, the dimensions of the fiberglass strands, such as 10μm, 11μm, and 13μm, play a crucial role in determining the properties and applications of the resulting composites. The term "μm" refers to micrometers, a unit of measurement that indicates the diameter of the fiberglass strands. Each size offers distinct characteristics that make them suitable for different applications. For instance, 10μm fiberglass strands are typically used in applications where a high surface area is required, such as in the automotive industry, where they contribute to the production of lightweight yet strong components. The smaller diameter allows for a greater number of fibers to be packed into a given volume, enhancing the mechanical properties of the composite. On the other hand, 11μm fiberglass strands strike a balance between strength and flexibility, making them ideal for use in construction materials where both durability and adaptability are essential. These strands are often used in the production of reinforced concrete and other building materials that require enhanced tensile strength. Meanwhile, 13μm fiberglass strands are favored in applications where maximum strength is paramount, such as in the production of heavy-duty electrical and electronic components. The larger diameter of these strands provides superior load-bearing capacity, making them suitable for use in environments where the materials are subjected to significant stress and strain. Beyond these specific sizes, the market also includes other dimensions of fiberglass strands, each tailored to meet the unique requirements of various industries. The choice of strand size is influenced by factors such as the desired mechanical properties, the type of thermoplastic resin used, and the specific application requirements. Manufacturers in the Global Chopped Fiberglass for Thermoplastics Market continuously explore new combinations of strand sizes and resin formulations to develop composites that offer improved performance and cost-effectiveness. This ongoing innovation is driven by the need to address the challenges faced by industries in terms of material performance, environmental impact, and production efficiency. As a result, the market is characterized by a diverse range of products that cater to the specific needs of different sectors, ensuring that the benefits of chopped fiberglass composites are accessible to a wide array of applications.

Automotive, Construction, Electrical and Electronics, Others in the Global Chopped Fiberglass for Thermoplastics Market:

The usage of Global Chopped Fiberglass for Thermoplastics Market spans several key industries, each benefiting from the unique properties of fiberglass composites. In the automotive sector, chopped fiberglass is used to produce lightweight components that contribute to improved fuel efficiency and reduced emissions. These composites are used in the manufacturing of various parts, including bumpers, dashboards, and under-the-hood components, where their strength and durability enhance vehicle performance and safety. The lightweight nature of fiberglass composites also allows for greater design flexibility, enabling manufacturers to create complex shapes and structures that would be difficult to achieve with traditional materials. In the construction industry, chopped fiberglass is used to reinforce concrete and other building materials, providing enhanced strength and durability. This is particularly important in applications where materials are exposed to harsh environmental conditions, such as in bridges, tunnels, and high-rise buildings. The use of fiberglass composites in construction also contributes to sustainability efforts, as they can reduce the overall weight of structures, leading to lower material consumption and energy use during construction. In the electrical and electronics sector, chopped fiberglass is used to produce components that require high strength and thermal resistance. These composites are used in the manufacturing of circuit boards, enclosures, and other electronic components, where their insulating properties and resistance to heat and moisture are critical. The use of fiberglass composites in this industry also supports the miniaturization of electronic devices, as they allow for the production of smaller, more efficient components. Beyond these specific industries, chopped fiberglass for thermoplastics is also used in a variety of other applications, including consumer goods, sports equipment, and industrial machinery. In each of these areas, the unique properties of fiberglass composites, such as their strength, durability, and lightweight nature, provide significant advantages over traditional materials. As industries continue to seek materials that offer a balance of performance, cost-effectiveness, and environmental sustainability, the usage of chopped fiberglass for thermoplastics is expected to expand, driving further innovation and development in the market.

Global Chopped Fiberglass for Thermoplastics Market Outlook:

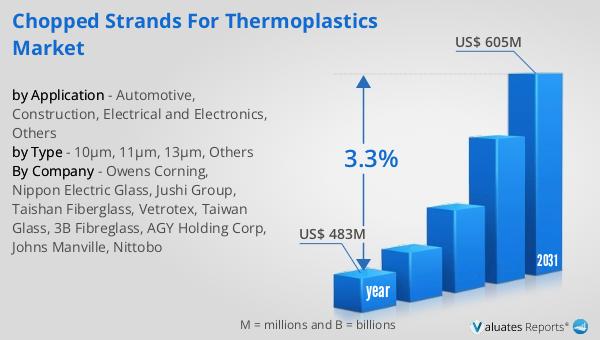

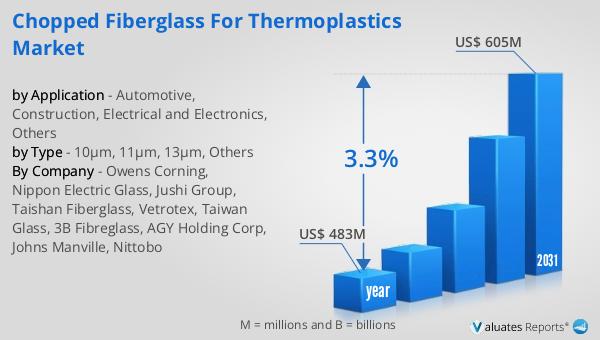

The outlook for the Global Chopped Fiberglass for Thermoplastics Market indicates a positive growth trajectory over the coming years. In 2024, the market was valued at approximately US$ 483 million, reflecting the significant demand for fiberglass composites across various industries. This demand is driven by the need for materials that offer a combination of strength, durability, and lightweight properties, which are essential for improving the performance and efficiency of products. Looking ahead, the market is projected to reach a revised size of US$ 605 million by 2031, growing at a compound annual growth rate (CAGR) of 3.3% during the forecast period. This growth is expected to be fueled by ongoing advancements in fiberglass production technologies and the development of new resin formulations that enhance the compatibility and performance of fiberglass composites. As industries continue to prioritize sustainability and cost-effectiveness, the demand for chopped fiberglass for thermoplastics is likely to increase, supporting the market's expansion. The positive outlook for the market also reflects the broader trends in the materials industry, where there is a growing emphasis on developing innovative solutions that address the challenges of modern manufacturing and product design. As a result, the Global Chopped Fiberglass for Thermoplastics Market is well-positioned to capitalize on these trends, offering a range of products that meet the evolving needs of industries worldwide.

| Report Metric | Details |

| Report Name | Chopped Fiberglass for Thermoplastics Market |

| Accounted market size in year | US$ 483 million |

| Forecasted market size in 2031 | US$ 605 million |

| CAGR | 3.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Owens Corning, Nippon Electric Glass, Jushi Group, Taishan Fiberglass, Vetrotex, Taiwan Glass, 3B Fibreglass, AGY Holding Corp, Johns Manville, Nittobo |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |