What is Global Industrial Waste Liquid Treatment Robots Market?

The Global Industrial Waste Liquid Treatment Robots Market refers to the industry focused on the development and deployment of robotic systems designed to manage and treat liquid waste generated by various industrial processes. These robots are engineered to handle hazardous and non-hazardous liquid waste, ensuring that it is treated, neutralized, or disposed of in an environmentally friendly manner. The market encompasses a wide range of technologies and solutions aimed at automating the treatment process, thereby enhancing efficiency, safety, and compliance with environmental regulations. As industries worldwide continue to grow, the volume of liquid waste produced has increased, necessitating advanced solutions to manage this waste effectively. Industrial waste liquid treatment robots are equipped with sensors, AI, and machine learning capabilities to identify, categorize, and treat different types of waste. This market is driven by the need for sustainable waste management solutions, stringent environmental regulations, and the increasing adoption of automation in industrial processes. The robots not only help in reducing human exposure to hazardous materials but also optimize the treatment process, leading to cost savings and improved operational efficiency for industries.

Chemical Waste Liquid Treatment Robots, Heavy Metal Waste Liquid Treatment Robots, Highly Corrosive Waste Liquid Treatment Robots, General-purpose Waste Liquid Treatment Robots, Others in the Global Industrial Waste Liquid Treatment Robots Market:

Chemical Waste Liquid Treatment Robots are specialized robots designed to handle and treat liquid waste generated from chemical manufacturing processes. These robots are equipped with advanced sensors and AI technologies to identify and neutralize hazardous chemicals, ensuring they are treated in compliance with environmental standards. They play a crucial role in preventing chemical spills and reducing the environmental impact of chemical waste. Heavy Metal Waste Liquid Treatment Robots, on the other hand, are engineered to manage waste containing heavy metals such as lead, mercury, and cadmium. These robots use specialized filtration and separation techniques to extract and neutralize heavy metals from industrial effluents, preventing them from contaminating water bodies and soil. Highly Corrosive Waste Liquid Treatment Robots are designed to handle waste that is highly acidic or alkaline, which can corrode standard equipment. These robots are built with corrosion-resistant materials and are capable of neutralizing corrosive substances, ensuring safe disposal. General-purpose Waste Liquid Treatment Robots are versatile systems that can handle a variety of liquid waste types, making them suitable for industries with diverse waste streams. They are equipped with adaptable technologies that allow them to switch between different treatment processes as needed. Other types of robots in this market include those designed for specific industries or waste types, offering tailored solutions for unique waste management challenges. These robots collectively contribute to the efficient and sustainable management of industrial liquid waste, ensuring compliance with environmental regulations and reducing the ecological footprint of industrial activities.

Chemical Manufacturing, Metal Processing, Electronics and Semiconductors, Pharmaceutical Industry, Others in the Global Industrial Waste Liquid Treatment Robots Market:

The usage of Global Industrial Waste Liquid Treatment Robots Market spans several key industries, each with its unique waste management challenges. In the Chemical Manufacturing sector, these robots are essential for handling the vast amounts of hazardous liquid waste produced during chemical synthesis and processing. They ensure that toxic chemicals are treated and neutralized before disposal, preventing environmental contamination and ensuring compliance with stringent regulations. In Metal Processing, robots are used to treat waste containing heavy metals and other pollutants. They help in extracting valuable metals from waste streams, reducing the environmental impact of metal processing activities. The Electronics and Semiconductors industry generates waste containing various chemicals and heavy metals. Waste treatment robots in this sector are crucial for managing these complex waste streams, ensuring that harmful substances are effectively neutralized and valuable materials are recovered. In the Pharmaceutical Industry, waste liquid treatment robots handle waste containing active pharmaceutical ingredients and other hazardous substances. They ensure that pharmaceutical waste is treated to prevent contamination of water bodies and soil. Other industries, such as food and beverage, textiles, and oil and gas, also benefit from these robots, which help in managing diverse waste streams and ensuring sustainable waste management practices. Overall, the adoption of industrial waste liquid treatment robots across these industries leads to improved environmental compliance, reduced operational costs, and enhanced safety for workers.

Global Industrial Waste Liquid Treatment Robots Market Outlook:

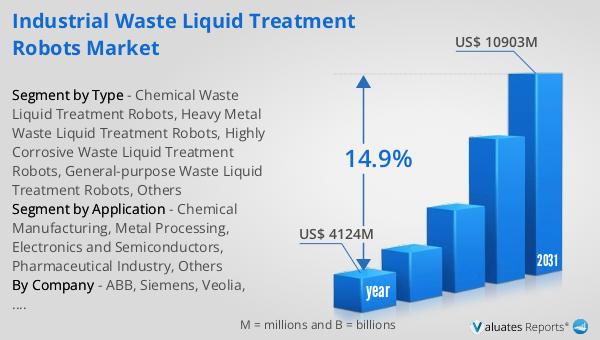

The global market for Industrial Waste Liquid Treatment Robots was valued at $4,124 million in 2024 and is anticipated to expand significantly, reaching an estimated $10,903 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 14.9% over the forecast period. This impressive growth is driven by several factors, including the increasing need for efficient and sustainable waste management solutions across various industries. As environmental regulations become more stringent, industries are compelled to adopt advanced technologies to manage their waste effectively. Industrial waste liquid treatment robots offer a viable solution by automating the treatment process, thereby enhancing efficiency and reducing human exposure to hazardous materials. The market's expansion is also fueled by the growing adoption of automation and robotics in industrial processes, which leads to cost savings and improved operational efficiency. As industries continue to evolve and expand, the demand for innovative waste management solutions is expected to rise, further propelling the growth of the industrial waste liquid treatment robots market. This market outlook highlights the significant potential for growth and innovation in this sector, driven by the need for sustainable and efficient waste management solutions.

| Report Metric | Details |

| Report Name | Industrial Waste Liquid Treatment Robots Market |

| Accounted market size in year | US$ 4124 million |

| Forecasted market size in 2031 | US$ 10903 million |

| CAGR | 14.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | ABB, Siemens, Veolia, SUEZ, Schneider Electric, Hitachi Zosen Inova, Mitsubishi Heavy Industries, GE Vernova, Ecolab, Xylem, Endress+Hauser, Yokogawa Electric, Rockwell Automation, Bosch Rexroth, Alfa Laval, Grundfos, Toshiba, Honeywell, Danaher, Emerson Electric, Pentair, Kurita Water Industries, Andritz AG, Ovivo |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |