What is Global Continuous Optical Parametric Oscillator (OPO) Market?

The Global Continuous Optical Parametric Oscillator (OPO) Market is a specialized segment within the broader photonics industry, focusing on devices that convert laser light into different wavelengths through a nonlinear optical process. These devices are highly valued for their ability to produce coherent light across a wide range of wavelengths, from the ultraviolet to the infrared spectrum. This versatility makes them indispensable in various scientific and industrial applications. The market is driven by the increasing demand for advanced laser technologies in fields such as spectroscopy, medical diagnostics, and military applications. Continuous OPOs are particularly favored for their ability to provide a stable and tunable light source, which is crucial for precision tasks. As industries continue to seek more efficient and adaptable laser solutions, the demand for continuous OPOs is expected to grow. The market is characterized by ongoing research and development efforts aimed at enhancing the performance and efficiency of these devices, as well as expanding their application range. Companies operating in this market are also focusing on developing cost-effective solutions to make these advanced technologies more accessible to a broader range of users.

Femtosecond, Picosecond in the Global Continuous Optical Parametric Oscillator (OPO) Market:

Femtosecond and picosecond lasers are integral to the Global Continuous Optical Parametric Oscillator (OPO) Market, offering unique capabilities that cater to various high-precision applications. Femtosecond lasers emit pulses with durations in the femtosecond range, which is one quadrillionth of a second. This ultra-short pulse duration allows for extremely precise material processing, minimizing thermal damage and enabling applications in delicate environments such as biological tissues. In the context of OPOs, femtosecond lasers are used to generate a broad spectrum of wavelengths, which can be tuned to specific frequencies for applications like spectroscopy and microscopy. The ability to produce such short pulses also makes femtosecond lasers ideal for time-resolved studies, where observing rapid processes at the molecular or atomic level is crucial. On the other hand, picosecond lasers, with pulse durations in the picosecond range (one trillionth of a second), offer a balance between precision and power. They are particularly useful in applications requiring high peak power and moderate pulse durations, such as micromachining and medical procedures. In the OPO market, picosecond lasers are valued for their ability to produce high-quality beams with minimal pulse broadening, which is essential for maintaining the integrity of the generated wavelengths. Both femtosecond and picosecond lasers are pivotal in advancing the capabilities of continuous OPOs, enabling them to meet the growing demands of various industries. As technology continues to evolve, the integration of these lasers into OPO systems is expected to enhance their performance, making them even more versatile and efficient. The ongoing research and development in this field aim to improve the pulse quality, stability, and tunability of these lasers, further expanding their application potential. Companies in the OPO market are investing in innovative solutions to harness the full potential of femtosecond and picosecond lasers, ensuring they remain at the forefront of laser technology advancements. This focus on innovation is crucial for maintaining a competitive edge in the rapidly evolving photonics industry, where the demand for high-performance laser systems continues to rise. As industries increasingly rely on precise and adaptable laser technologies, the role of femtosecond and picosecond lasers in the OPO market is set to become even more significant.

Spectroscopy, Infrared Medicine, Military and Security, Quantum Optics, Others in the Global Continuous Optical Parametric Oscillator (OPO) Market:

The Global Continuous Optical Parametric Oscillator (OPO) Market finds extensive usage across various fields, each benefiting from the unique capabilities of these devices. In spectroscopy, continuous OPOs are invaluable for their ability to provide a tunable light source that can cover a wide range of wavelengths. This tunability is crucial for identifying and analyzing different substances based on their spectral signatures. Researchers and scientists rely on OPOs to conduct precise measurements and gain insights into the molecular composition of materials. In infrared medicine, continuous OPOs are used for non-invasive diagnostic procedures and therapeutic applications. Their ability to generate specific wavelengths allows for targeted treatments, such as laser surgery and phototherapy, minimizing damage to surrounding tissues. The precision and adaptability of OPOs make them ideal for medical applications where accuracy is paramount. In the military and security sectors, continuous OPOs are employed for applications such as laser range finding, target designation, and countermeasure systems. Their ability to produce coherent light at various wavelengths enhances the effectiveness of these systems, providing a strategic advantage in defense operations. The versatility of OPOs also makes them suitable for use in quantum optics, where they are used to study and manipulate quantum states of light. This field of research holds the potential for groundbreaking advancements in quantum computing and secure communication technologies. Beyond these specific areas, continuous OPOs are also utilized in other industries, such as telecommunications and environmental monitoring. Their ability to generate a wide range of wavelengths makes them suitable for applications like fiber optic communication and remote sensing. As industries continue to seek advanced laser solutions, the demand for continuous OPOs is expected to grow, driven by their versatility and precision. The ongoing research and development efforts in this market aim to enhance the performance and efficiency of OPOs, making them even more adaptable to the evolving needs of various sectors. Companies operating in this market are focused on developing innovative solutions to expand the application range of OPOs, ensuring they remain at the forefront of laser technology advancements. This commitment to innovation is crucial for maintaining a competitive edge in the rapidly evolving photonics industry, where the demand for high-performance laser systems continues to rise. As industries increasingly rely on precise and adaptable laser technologies, the role of continuous OPOs in various applications is set to become even more significant.

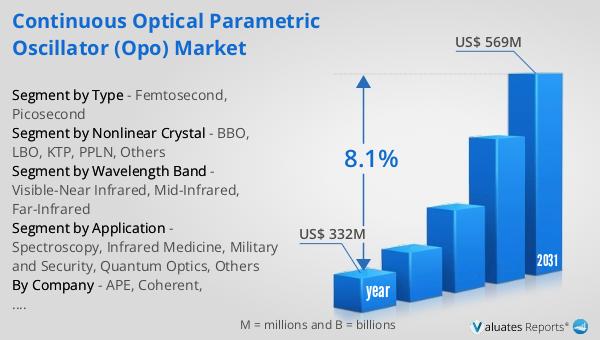

Global Continuous Optical Parametric Oscillator (OPO) Market Outlook:

In 2024, the global market for Continuous Optical Parametric Oscillators (OPOs) was valued at approximately $332 million. Looking ahead, this market is anticipated to expand significantly, reaching an estimated value of $569 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 8.1% over the forecast period. The increasing demand for advanced laser technologies across various industries is a key driver of this market expansion. Continuous OPOs are highly sought after for their ability to provide stable and tunable light sources, which are essential for precision tasks in fields such as spectroscopy, medical diagnostics, and military applications. As industries continue to seek more efficient and adaptable laser solutions, the demand for continuous OPOs is expected to grow. Companies operating in this market are focusing on developing cost-effective solutions to make these advanced technologies more accessible to a broader range of users. The ongoing research and development efforts in this market aim to enhance the performance and efficiency of OPOs, making them even more adaptable to the evolving needs of various sectors. This commitment to innovation is crucial for maintaining a competitive edge in the rapidly evolving photonics industry, where the demand for high-performance laser systems continues to rise. As industries increasingly rely on precise and adaptable laser technologies, the role of continuous OPOs in various applications is set to become even more significant.

| Report Metric | Details |

| Report Name | Continuous Optical Parametric Oscillator (OPO) Market |

| Accounted market size in year | US$ 332 million |

| Forecasted market size in 2031 | US$ 569 million |

| CAGR | 8.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Nonlinear Crystal |

|

| Segment by Wavelength Band |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | APE, Coherent, Newport, Qioptiq, Excelitas, Radiantis, Shanghai EachWave Photoelectric Technology, Bonphot Optoelectronic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |