What is Global Transparent PVC Granules Compound Market?

The Global Transparent PVC Granules Compound Market is a specialized segment within the broader PVC industry, focusing on the production and distribution of transparent polyvinyl chloride (PVC) granules. These granules are a type of thermoplastic material known for their clarity, flexibility, and durability. Transparent PVC granules are used in various applications due to their excellent properties, such as high impact resistance, chemical stability, and ease of processing. They are particularly valued in industries where visibility and aesthetic appeal are important, such as packaging, medical devices, and consumer goods. The market for these granules is driven by the increasing demand for lightweight and durable materials that can be easily molded into different shapes and sizes. Additionally, the growing awareness of sustainable and recyclable materials has further boosted the demand for transparent PVC granules, as they can be recycled and reused in various applications. The market is characterized by a diverse range of products, catering to different industry needs, and is supported by continuous innovations in material science and processing technologies. As industries continue to seek materials that offer both functionality and aesthetic appeal, the Global Transparent PVC Granules Compound Market is poised for steady growth.

Soft PVC, Hard PVC in the Global Transparent PVC Granules Compound Market:

Soft PVC and Hard PVC are two primary types of polyvinyl chloride materials used in the Global Transparent PVC Granules Compound Market, each with distinct characteristics and applications. Soft PVC, also known as flexible PVC, is made by adding plasticizers to the PVC compound, which increases its flexibility and elasticity. This type of PVC is commonly used in applications where flexibility is crucial, such as in the production of hoses, cables, and inflatable products. Soft PVC is valued for its ability to withstand bending and twisting without cracking, making it ideal for products that require frequent handling or movement. Additionally, its transparency allows for aesthetic appeal in consumer goods and packaging, where visibility of the product is important. On the other hand, Hard PVC, or rigid PVC, is produced without plasticizers, resulting in a more rigid and durable material. This type of PVC is used in applications where strength and stability are required, such as in construction materials, pipes, and window frames. Hard PVC is known for its excellent resistance to weathering, chemicals, and impact, making it suitable for outdoor and industrial applications. In the Global Transparent PVC Granules Compound Market, both Soft and Hard PVC play crucial roles in meeting the diverse needs of various industries. The choice between Soft and Hard PVC depends on the specific requirements of the application, such as flexibility, strength, and transparency. For instance, in the medical and healthcare industry, Soft PVC is often used for making flexible tubing and blood bags, where flexibility and clarity are essential. In contrast, Hard PVC is preferred in construction for making durable and weather-resistant profiles and panels. The versatility of PVC, whether soft or hard, lies in its ability to be tailored to specific applications through the use of additives and processing techniques. This adaptability makes PVC a popular choice in the Global Transparent PVC Granules Compound Market, as manufacturers can customize the material properties to suit the needs of different industries. Furthermore, advancements in PVC compounding technology have led to the development of new formulations that enhance the performance and sustainability of both Soft and Hard PVC. These innovations include the use of bio-based plasticizers for Soft PVC and the incorporation of impact modifiers for Hard PVC, which improve the material's environmental profile and mechanical properties. As the demand for high-performance and sustainable materials continues to grow, the Global Transparent PVC Granules Compound Market is expected to see increased adoption of both Soft and Hard PVC in various applications. The ability to balance flexibility, durability, and transparency makes PVC a versatile and valuable material in the modern industrial landscape.

Construction and Building Materials, Electrical and Electronics, Industrial Products, Consumer Goods and Packaging, Medical and Healthcare, Other in the Global Transparent PVC Granules Compound Market:

The Global Transparent PVC Granules Compound Market finds extensive usage across various sectors, including Construction and Building Materials, Electrical and Electronics, Industrial Products, Consumer Goods and Packaging, Medical and Healthcare, and other areas. In the Construction and Building Materials sector, transparent PVC granules are used to produce durable and weather-resistant profiles, panels, and fittings. These materials are valued for their clarity, which allows for aesthetic architectural designs, and their resistance to environmental factors, making them suitable for both indoor and outdoor applications. In the Electrical and Electronics industry, transparent PVC granules are used in the production of insulating materials for cables and wires, as well as in the manufacturing of electronic components that require visibility and protection. The material's excellent electrical insulation properties and flexibility make it ideal for these applications. In the Industrial Products sector, transparent PVC granules are used to manufacture a wide range of products, including hoses, seals, and gaskets, where durability and chemical resistance are important. The Consumer Goods and Packaging industry benefits from the use of transparent PVC granules in the production of clear packaging materials, toys, and household items. The material's transparency and flexibility allow for attractive packaging designs and durable consumer products. In the Medical and Healthcare sector, transparent PVC granules are used to produce medical devices, tubing, and containers that require clarity and biocompatibility. The material's ability to be sterilized and its resistance to chemicals make it suitable for medical applications. Other areas where transparent PVC granules are used include the automotive industry, where they are used in the production of interior components and trims, and the fashion industry, where they are used to create transparent accessories and footwear. The versatility and adaptability of transparent PVC granules make them a valuable material in various industries, offering a balance of functionality and aesthetic appeal. As industries continue to seek materials that offer both performance and sustainability, the Global Transparent PVC Granules Compound Market is expected to see increased adoption across these sectors.

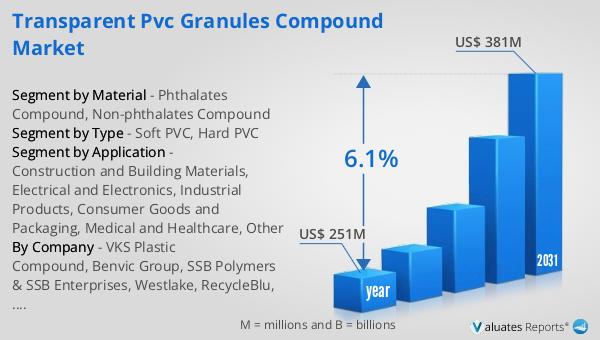

Global Transparent PVC Granules Compound Market Outlook:

The global market for Transparent PVC Granules Compound was valued at $251 million in 2024, and it is anticipated to grow significantly, reaching an estimated value of $381 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 6.1% over the forecast period. This upward trend in the market is indicative of the increasing demand for transparent PVC granules across various industries. The market's expansion can be attributed to several factors, including the rising need for lightweight and durable materials in construction, packaging, and consumer goods. Additionally, the growing awareness of sustainable and recyclable materials has further fueled the demand for transparent PVC granules, as they offer both functionality and environmental benefits. The market's growth is also supported by continuous innovations in material science and processing technologies, which have led to the development of new formulations that enhance the performance and sustainability of transparent PVC granules. As industries continue to seek materials that offer both performance and aesthetic appeal, the Global Transparent PVC Granules Compound Market is poised for steady growth. The ability to balance flexibility, durability, and transparency makes transparent PVC granules a versatile and valuable material in the modern industrial landscape.

| Report Metric | Details |

| Report Name | Transparent PVC Granules Compound Market |

| Accounted market size in year | US$ 251 million |

| Forecasted market size in 2031 | US$ 381 million |

| CAGR | 6.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Material |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | VKS Plastic Compound, Benvic Group, SSB Polymers & SSB Enterprises, Westlake, RecycleBlu, Polytech Middle East, Dhingra Polymers, Petrola, PlasticKar, TeraPlast, Ekmen Plastik, Tan Kauçuk, Zanbond Group, NAN YA PLASTICS, ZEON KASEI, Flychem Plastic, Jiahong, Jinlida, Cheerget Plastic Industrial |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |