What is Global Recycled PA6 and PA66 Market?

Global Recycled PA6 and PA66 Market refers to the industry focused on the recycling and reuse of two specific types of polyamides, namely PA6 and PA66. These materials, commonly known as Nylon 6 and Nylon 66, are synthetic polymers widely used in various applications due to their strength, durability, and resistance to wear and chemicals. The recycling of these materials is gaining traction as industries and consumers become more environmentally conscious, seeking sustainable alternatives to traditional manufacturing processes. By recycling PA6 and PA66, the market aims to reduce waste, lower carbon footprints, and conserve resources, aligning with global sustainability goals. The recycled versions of these polyamides are utilized in numerous sectors, including textiles, automotive, electronics, and packaging, offering similar performance characteristics to their virgin counterparts but with a reduced environmental impact. As the demand for sustainable materials grows, the Global Recycled PA6 and PA66 Market is poised to expand, driven by technological advancements in recycling processes and increasing regulatory support for eco-friendly practices. This market not only contributes to environmental conservation but also offers economic benefits by creating new business opportunities and reducing dependency on raw materials.

PA6, PA66 in the Global Recycled PA6 and PA66 Market:

PA6, or Nylon 6, and PA66, or Nylon 66, are two types of polyamides that are extensively used in various industries due to their excellent mechanical properties and versatility. PA6 is produced through the polymerization of caprolactam, while PA66 is made from the polymerization of hexamethylenediamine and adipic acid. Both materials are known for their high tensile strength, abrasion resistance, and thermal stability, making them ideal for applications that require durability and reliability. In the context of the Global Recycled PA6 and PA66 Market, these materials are recycled to create sustainable alternatives to virgin polyamides. The recycling process involves collecting post-industrial and post-consumer waste, cleaning and sorting the materials, and then reprocessing them into new products. This not only helps in reducing environmental pollution but also conserves natural resources by minimizing the need for new raw materials. Recycled PA6 and PA66 are used in a wide range of applications, including automotive parts, electrical components, textiles, and consumer goods. The automotive industry, for instance, utilizes these recycled materials to manufacture components such as engine covers, air intake manifolds, and interior trims, contributing to the reduction of vehicle weight and improvement of fuel efficiency. In the textile industry, recycled PA6 and PA66 are used to produce fibers for clothing, carpets, and upholstery, offering a sustainable alternative to traditional materials. The electronics industry also benefits from these recycled polyamides, using them in the production of connectors, circuit breakers, and other components that require high-performance materials. The growing demand for sustainable products and the increasing awareness of environmental issues are driving the expansion of the Global Recycled PA6 and PA66 Market. As more companies and consumers prioritize sustainability, the market is expected to continue its growth trajectory, supported by advancements in recycling technologies and favorable government policies. By embracing recycled PA6 and PA66, industries can not only reduce their environmental impact but also enhance their brand image and meet the evolving expectations of eco-conscious consumers.

Apparels, Carpet, Baggage, Industrial, Others in the Global Recycled PA6 and PA66 Market:

The Global Recycled PA6 and PA66 Market finds significant applications across various sectors, including apparels, carpets, baggage, industrial uses, and others. In the apparel industry, recycled PA6 and PA66 are used to produce eco-friendly clothing and accessories. These materials offer the same durability and comfort as virgin polyamides but with a reduced environmental footprint. Brands are increasingly incorporating recycled polyamides into their collections to appeal to environmentally conscious consumers and meet sustainability goals. In the carpet industry, recycled PA6 and PA66 are used to manufacture sustainable flooring solutions. These materials provide excellent wear resistance and longevity, making them ideal for both residential and commercial applications. By using recycled polyamides, carpet manufacturers can reduce their reliance on virgin materials and contribute to waste reduction. The baggage industry also benefits from the use of recycled PA6 and PA66, as these materials are used to produce durable and lightweight luggage. Recycled polyamides offer the same strength and resilience as their virgin counterparts, ensuring that bags can withstand the rigors of travel while minimizing environmental impact. In industrial applications, recycled PA6 and PA66 are used to manufacture components for machinery, equipment, and infrastructure. These materials provide the necessary strength and durability for demanding industrial environments, while also supporting sustainability initiatives. Other applications of recycled PA6 and PA66 include consumer goods, packaging, and automotive parts. The versatility and performance of these materials make them suitable for a wide range of products, from household items to high-performance automotive components. As industries continue to prioritize sustainability, the demand for recycled PA6 and PA66 is expected to grow, driven by the need for eco-friendly materials and the desire to reduce environmental impact.

Global Recycled PA6 and PA66 Market Outlook:

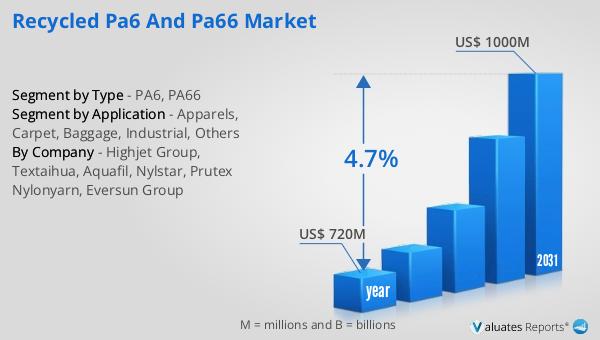

The global market for Recycled PA6 and PA66 was valued at approximately $720 million in 2024, and it is anticipated to grow significantly, reaching an estimated value of $1,000 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.7% over the forecast period. The increasing demand for sustainable materials and the growing awareness of environmental issues are key factors driving this market expansion. As industries and consumers alike seek to reduce their carbon footprints and embrace eco-friendly practices, the demand for recycled polyamides is expected to rise. The market's growth is further supported by advancements in recycling technologies, which enhance the quality and performance of recycled PA6 and PA66, making them viable alternatives to virgin materials. Additionally, favorable government policies and regulations promoting sustainability and waste reduction are expected to bolster market growth. As the market continues to evolve, companies operating in this space are likely to invest in research and development to improve recycling processes and expand their product offerings. By doing so, they can capitalize on the growing demand for recycled polyamides and contribute to a more sustainable future.

| Report Metric | Details |

| Report Name | Recycled PA6 and PA66 Market |

| Accounted market size in year | US$ 720 million |

| Forecasted market size in 2031 | US$ 1000 million |

| CAGR | 4.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Highjet Group, Textaihua, Aquafil, Nylstar, Prutex Nylonyarn, Eversun Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |