What is Global GNSS Module for Drone Market?

The Global GNSS Module for Drone Market is a rapidly evolving sector that plays a crucial role in the navigation and positioning of drones. GNSS, or Global Navigation Satellite System, modules are essential components that enable drones to determine their precise location by receiving signals from satellites. These modules are integral to the functioning of drones, providing them with the ability to navigate autonomously, maintain stability, and execute complex flight patterns. The market for GNSS modules in drones is driven by the increasing demand for drones across various industries, including agriculture, logistics, and surveillance. As drones become more sophisticated and their applications more diverse, the need for accurate and reliable GNSS modules has grown. This market is characterized by continuous technological advancements, with manufacturers striving to develop modules that offer higher precision, faster signal acquisition, and better resistance to interference. The growth of this market is also fueled by the increasing adoption of drones in emerging economies, where they are used for tasks ranging from crop monitoring to infrastructure inspection. Overall, the Global GNSS Module for Drone Market is poised for significant growth as the capabilities and applications of drones continue to expand.

Single-band Module, Dual-band Module in the Global GNSS Module for Drone Market:

The Global GNSS Module for Drone Market is segmented into Single-band and Dual-band modules, each offering distinct advantages and catering to different needs. Single-band GNSS modules operate on one frequency band, typically the L1 band, which is the most commonly used frequency for civilian GNSS applications. These modules are generally more affordable and are suitable for applications where high precision is not critical. They are widely used in consumer drones, where cost-effectiveness is a priority, and the level of accuracy provided by a single-band module is sufficient for recreational flying and basic photography. However, single-band modules can be susceptible to signal interference and multipath errors, which can affect their accuracy and reliability in challenging environments such as urban areas or dense forests. On the other hand, Dual-band GNSS modules operate on two frequency bands, usually the L1 and L5 bands. The addition of the L5 band provides several advantages, including improved accuracy, faster signal acquisition, and better resistance to interference and multipath errors. Dual-band modules are particularly beneficial in environments where signal quality is compromised, such as urban canyons or areas with dense foliage. They are increasingly being adopted in industrial and commercial drones, where precision and reliability are paramount. For instance, in applications such as surveying, mapping, and precision agriculture, the enhanced accuracy of dual-band modules can significantly improve the quality of data collected by drones. The choice between single-band and dual-band GNSS modules depends largely on the specific requirements of the drone application. While single-band modules offer a cost-effective solution for basic applications, dual-band modules provide the enhanced performance needed for more demanding tasks. As the technology continues to evolve, the gap between the capabilities of single-band and dual-band modules is expected to narrow, with improvements in signal processing and error correction techniques. This evolution will likely lead to broader adoption of dual-band modules across various sectors, as the benefits of increased accuracy and reliability become more accessible. In conclusion, the Global GNSS Module for Drone Market is characterized by a diverse range of products that cater to different needs and applications. Single-band modules offer a cost-effective solution for consumer drones and basic applications, while dual-band modules provide the enhanced performance required for industrial and commercial applications. As the market continues to grow and evolve, advancements in technology will likely lead to further improvements in the capabilities of GNSS modules, driving their adoption across a wider range of applications.

Consumer Drones, Industrial & Commercial Drones, Delivery Drones, Racing & FPV Drones, Others in the Global GNSS Module for Drone Market:

The Global GNSS Module for Drone Market finds applications across a wide range of areas, each with its unique requirements and challenges. Consumer drones, for instance, are primarily used for recreational purposes, photography, and videography. In this segment, GNSS modules are essential for providing basic navigation and positioning capabilities, allowing users to fly their drones with ease and capture stunning aerial footage. The affordability and ease of use of consumer drones have made them increasingly popular among hobbyists and amateur photographers, driving the demand for reliable and cost-effective GNSS modules. In the realm of industrial and commercial drones, GNSS modules play a critical role in enabling advanced functionalities such as autonomous flight, precision navigation, and data collection. These drones are used in a variety of industries, including agriculture, construction, and energy, where they perform tasks such as crop monitoring, infrastructure inspection, and environmental surveying. The accuracy and reliability of GNSS modules are crucial in these applications, as they directly impact the quality of the data collected and the efficiency of operations. Dual-band GNSS modules are often preferred in this segment due to their enhanced performance and ability to operate in challenging environments. Delivery drones represent another significant area of application for GNSS modules. As the demand for fast and efficient delivery services continues to grow, companies are increasingly turning to drones as a viable solution for last-mile delivery. GNSS modules are essential for enabling precise navigation and route optimization, ensuring that packages are delivered accurately and efficiently. The reliability and accuracy of GNSS modules are particularly important in urban areas, where signal interference and multipath errors can pose significant challenges. Racing and FPV (First Person View) drones are another exciting application of GNSS modules. These drones are used in competitive racing events, where speed, agility, and precision are paramount. GNSS modules provide the necessary navigation and positioning capabilities, allowing pilots to maneuver their drones with precision and compete at high speeds. The demand for high-performance GNSS modules in this segment is driven by the need for fast signal acquisition and minimal latency, ensuring that pilots have real-time control over their drones. In addition to these areas, GNSS modules are also used in a variety of other applications, including search and rescue operations, wildlife monitoring, and scientific research. The versatility and adaptability of GNSS modules make them an essential component in the expanding drone ecosystem, enabling a wide range of applications and driving innovation across multiple sectors. As the capabilities of drones continue to evolve, the demand for advanced GNSS modules is expected to grow, further expanding their usage across various industries.

Global GNSS Module for Drone Market Outlook:

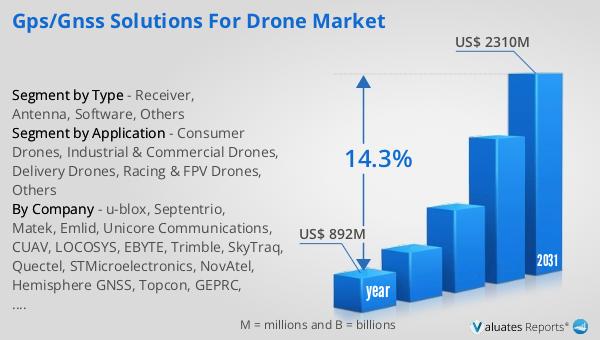

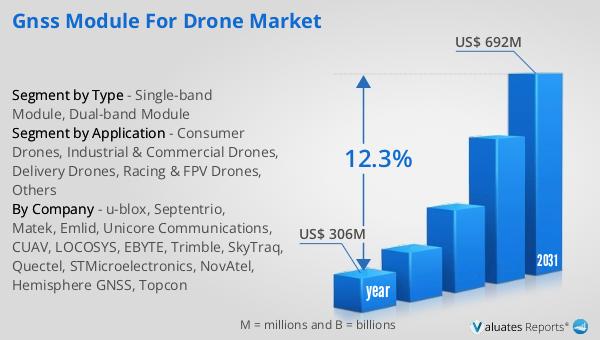

The outlook for the Global GNSS Module for Drone Market is promising, with significant growth anticipated over the coming years. In 2024, the market was valued at approximately US$ 306 million, reflecting the increasing demand for GNSS modules across various drone applications. This demand is driven by the growing adoption of drones in sectors such as agriculture, logistics, and surveillance, where accurate navigation and positioning are critical. As the capabilities of drones continue to expand, the need for reliable and high-performance GNSS modules is expected to rise, contributing to the market's growth. By 2031, the market is projected to reach a revised size of US$ 692 million, representing a compound annual growth rate (CAGR) of 12.3% during the forecast period. This growth is indicative of the ongoing advancements in GNSS technology, as well as the increasing recognition of the benefits that drones offer across various industries. The development of more sophisticated GNSS modules, with features such as dual-band operation and enhanced resistance to interference, is expected to further drive the market's expansion. The projected growth of the Global GNSS Module for Drone Market also reflects the broader trends in the drone industry, where innovation and technological advancements are leading to new applications and opportunities. As drones become more integrated into everyday operations, the demand for GNSS modules that can provide accurate and reliable navigation will continue to grow. This growth is likely to be supported by ongoing research and development efforts, as well as collaborations between manufacturers and industry stakeholders to address the evolving needs of the market. Overall, the outlook for the Global GNSS Module for Drone Market is positive, with significant growth expected over the coming years. The increasing adoption of drones across various sectors, coupled with advancements in GNSS technology, is set to drive the market's expansion and create new opportunities for manufacturers and stakeholders. As the market continues to evolve, the development of innovative GNSS modules will be key to meeting the demands of the growing drone industry and unlocking the full potential of drone technology.

| Report Metric | Details |

| Report Name | GNSS Module for Drone Market |

| Accounted market size in year | US$ 306 million |

| Forecasted market size in 2031 | US$ 692 million |

| CAGR | 12.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | u-blox, Septentrio, Matek, Emlid, Unicore Communications, CUAV, LOCOSYS, EBYTE, Trimble, SkyTraq, Quectel, STMicroelectronics, NovAtel, Hemisphere GNSS, Topcon |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |