What is Global LED Insertion Machine Market?

The Global LED Insertion Machine Market refers to the industry focused on the production and distribution of machines specifically designed for inserting LED components into printed circuit boards (PCBs). These machines are crucial in the electronics manufacturing process, as they automate the placement of LED components, ensuring precision and efficiency. The market encompasses a variety of machine types, including semi-automatic and fully-automatic models, each catering to different production needs and scales. The demand for LED insertion machines is driven by the growing adoption of LED technology across various sectors, such as lighting, displays, and automotive electronics. As industries continue to shift towards energy-efficient and durable lighting solutions, the need for advanced manufacturing equipment like LED insertion machines is expected to rise. This market is characterized by technological advancements, with manufacturers continuously innovating to improve machine speed, accuracy, and versatility. The global reach of this market indicates its significance in the broader electronics manufacturing landscape, as companies worldwide seek to enhance their production capabilities and meet the increasing demand for LED-based products.

Semi-automatic, Fully-automatic in the Global LED Insertion Machine Market:

In the Global LED Insertion Machine Market, machines are categorized into semi-automatic and fully-automatic types, each offering distinct advantages and catering to different manufacturing needs. Semi-automatic LED insertion machines require some level of human intervention during the operation. These machines are typically used in smaller production environments where flexibility and cost-effectiveness are prioritized. Operators are responsible for loading components and sometimes aligning them, while the machine handles the insertion process. This type of machine is ideal for manufacturers who need to produce a variety of products in smaller batches, as it allows for quick changeovers and adjustments. The semi-automatic machines are generally more affordable than their fully-automatic counterparts, making them accessible to smaller businesses or those just starting in the LED manufacturing industry. On the other hand, fully-automatic LED insertion machines are designed for high-volume production environments where speed and precision are critical. These machines operate with minimal human intervention, as they are equipped with advanced technology that automates the entire insertion process. Fully-automatic machines are capable of handling large quantities of components with high accuracy, significantly reducing the risk of errors and increasing production efficiency. They are equipped with features such as automatic component feeding, alignment, and insertion, which streamline the manufacturing process and reduce labor costs. These machines are ideal for large-scale manufacturers who need to produce consistent, high-quality products at a rapid pace. The choice between semi-automatic and fully-automatic machines depends on several factors, including production volume, budget, and the level of flexibility required. While fully-automatic machines offer higher efficiency and lower labor costs, they require a significant initial investment and are best suited for large-scale operations. Semi-automatic machines, while less efficient in terms of speed, offer greater flexibility and lower upfront costs, making them suitable for smaller manufacturers or those with diverse product lines. Both types of machines play a crucial role in the Global LED Insertion Machine Market, as they enable manufacturers to meet the growing demand for LED products across various industries. As technology continues to advance, the capabilities of both semi-automatic and fully-automatic machines are expected to improve, further enhancing their efficiency and effectiveness in the manufacturing process.

LED Lighting, LED Display, Automotive Electronics, Electronic Drive Power Supplies, Others in the Global LED Insertion Machine Market:

The Global LED Insertion Machine Market finds its applications across various sectors, each utilizing the technology to enhance their production processes and product offerings. In the LED lighting industry, these machines are essential for manufacturing LED bulbs, tubes, and other lighting fixtures. The precision and efficiency of LED insertion machines ensure that the components are accurately placed, resulting in high-quality lighting products that are energy-efficient and durable. As the demand for LED lighting continues to grow due to its environmental benefits and cost savings, the use of LED insertion machines in this sector is expected to increase. In the LED display industry, insertion machines are used to produce screens for televisions, monitors, and digital signage. The accuracy of these machines is crucial in ensuring that the LED components are correctly aligned, which directly impacts the display quality. With the rise of high-definition and ultra-high-definition displays, the need for precise and efficient manufacturing processes has become more critical, driving the demand for advanced LED insertion machines. Automotive electronics is another area where the Global LED Insertion Machine Market plays a significant role. LED technology is increasingly being used in automotive lighting systems, dashboards, and infotainment displays. The use of LED insertion machines in this sector ensures that the components are reliably placed, contributing to the overall performance and safety of the vehicle. As the automotive industry continues to innovate and integrate more electronic components, the demand for LED insertion machines is likely to grow. In the production of electronic drive power supplies, LED insertion machines are used to assemble components that regulate and distribute power within electronic devices. The precision and reliability of these machines are crucial in ensuring that the power supplies function correctly and efficiently. As electronic devices become more complex and power demands increase, the need for advanced manufacturing equipment like LED insertion machines becomes more apparent. Other industries, such as telecommunications and consumer electronics, also benefit from the use of LED insertion machines. These machines enable manufacturers to produce a wide range of products, from smartphones to network equipment, with high precision and efficiency. The versatility of LED insertion machines makes them an invaluable asset in the production of various electronic devices, contributing to the overall growth and development of the Global LED Insertion Machine Market.

Global LED Insertion Machine Market Outlook:

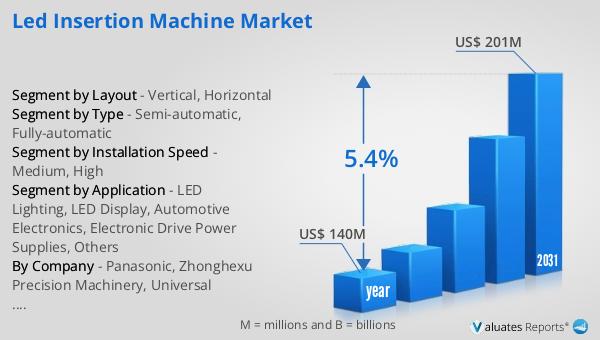

The global market for LED Insertion Machines was valued at approximately $140 million in 2024. This market is anticipated to expand, reaching an estimated size of $201 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.4% over the forecast period. The increasing demand for LED technology across various industries, such as lighting, displays, and automotive electronics, is a significant driver of this market growth. As more companies adopt LED technology for its energy efficiency and longevity, the need for advanced manufacturing equipment like LED insertion machines becomes more pronounced. These machines play a crucial role in the production process, ensuring precision and efficiency in the placement of LED components. The market's expansion is also fueled by technological advancements in LED insertion machines, which enhance their speed, accuracy, and versatility. Manufacturers are continuously innovating to meet the evolving needs of the electronics industry, further driving the market's growth. The global reach of this market highlights its importance in the broader electronics manufacturing landscape, as companies worldwide seek to enhance their production capabilities and meet the increasing demand for LED-based products. The projected growth of the Global LED Insertion Machine Market underscores the significance of these machines in the future of electronics manufacturing.

| Report Metric | Details |

| Report Name | LED Insertion Machine Market |

| Accounted market size in year | US$ 140 million |

| Forecasted market size in 2031 | US$ 201 million |

| CAGR | 5.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Installation Speed |

|

| Segment by Layout |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Panasonic, Zhonghexu Precision Machinery, Universal Instruments Corporation, JUKI CORPORATION, Fuji, Delta Electronics, Cencorp, Fuxing Intelligent, Tungson Electronic Machinery, South Jayong (DongGuan) Electronic, Dongguan Sciencgo Machinery Manufacturing, DZ Intelligence |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |