What is Global Mycology Immunoassays Testing Market?

The Global Mycology Immunoassays Testing Market is a specialized segment within the broader field of medical diagnostics, focusing on the detection and analysis of fungal infections. These infections, caused by fungi such as yeasts and molds, can lead to serious health issues, especially in individuals with weakened immune systems. Mycology immunoassays are laboratory tests that use antibodies to detect specific fungal antigens in a patient's sample, providing crucial information for diagnosis and treatment. The market for these tests is driven by the increasing prevalence of fungal infections, advancements in diagnostic technologies, and a growing awareness of the importance of early and accurate diagnosis. As healthcare systems worldwide strive to improve patient outcomes, the demand for reliable and efficient mycology immunoassays continues to rise. This market encompasses various testing methods, including enzyme-linked immunosorbent assays (ELISA), rapid tests, enzyme-linked immunospot assays (ELISPOT), and polymerase chain reaction (PCR) techniques, each offering unique advantages in terms of sensitivity, specificity, and speed. The global market is characterized by ongoing research and development efforts aimed at enhancing test accuracy and expanding the range of detectable fungal pathogens, ultimately contributing to better management of fungal diseases.

ELISA, Rapid Tests, ELISPOT, Polymerase Chain Reaction (PCR) in the Global Mycology Immunoassays Testing Market:

Enzyme-linked immunosorbent assays (ELISA) are a cornerstone of the Global Mycology Immunoassays Testing Market, known for their high sensitivity and specificity in detecting fungal antigens. ELISA tests work by using antibodies to bind to specific antigens present in a sample, such as blood or urine, and produce a measurable signal, often a color change, indicating the presence of the target fungus. This method is widely used due to its ability to process multiple samples simultaneously, making it efficient for large-scale screenings. Rapid tests, on the other hand, offer the advantage of speed, providing results in a matter of minutes. These tests are particularly useful in clinical settings where quick decision-making is crucial, such as emergency rooms or outpatient clinics. Rapid tests typically involve a simple procedure, often requiring just a drop of blood or a swab sample, and are designed to be user-friendly, even for non-specialist healthcare providers. ELISPOT assays, though less commonly used in mycology, are valuable for their ability to detect and quantify individual cells secreting specific cytokines in response to fungal antigens. This method is particularly useful in research settings, where understanding the immune response to fungal infections is critical. Polymerase chain reaction (PCR) is another powerful tool in the mycology immunoassays arsenal, known for its unparalleled sensitivity and specificity. PCR tests amplify the genetic material of fungi, allowing for the detection of even minute quantities of fungal DNA in a sample. This technique is especially beneficial for identifying hard-to-culture fungi or in cases where traditional methods fall short. PCR-based tests are increasingly being integrated into routine diagnostics due to their ability to provide definitive results, even in complex cases. Each of these testing methods plays a vital role in the comprehensive approach to diagnosing and managing fungal infections, catering to different needs and scenarios within the healthcare landscape.

Hospitals, Blood Banks, Others in the Global Mycology Immunoassays Testing Market:

The usage of Global Mycology Immunoassays Testing Market extends across various healthcare settings, including hospitals, blood banks, and other medical facilities, each with unique requirements and applications. In hospitals, mycology immunoassays are essential tools for diagnosing fungal infections in patients, particularly those with compromised immune systems, such as cancer patients undergoing chemotherapy, organ transplant recipients, or individuals with HIV/AIDS. Early and accurate detection of fungal infections in these patients is crucial, as it allows for timely intervention and treatment, reducing the risk of severe complications or mortality. Hospitals rely on a combination of ELISA, rapid tests, and PCR-based methods to ensure comprehensive and reliable diagnostics, often integrating these tests into routine screening protocols for high-risk patients. Blood banks also utilize mycology immunoassays to ensure the safety of blood products. Fungal contamination in blood supplies can pose significant health risks to recipients, particularly those who are already vulnerable due to illness or medical treatment. By employing rapid tests and PCR techniques, blood banks can quickly and accurately screen for fungal pathogens, ensuring that only safe and uncontaminated blood products are distributed for transfusion. This is especially important in regions with high prevalence rates of certain fungal infections, where the risk of contamination is elevated. Beyond hospitals and blood banks, other medical facilities, such as outpatient clinics and specialized laboratories, also benefit from the advancements in mycology immunoassays. These facilities often serve as the first point of contact for patients experiencing symptoms of fungal infections, making rapid and accurate diagnostics essential for effective patient management. In these settings, the availability of user-friendly rapid tests and ELISA kits enables healthcare providers to make informed decisions quickly, facilitating prompt treatment and improving patient outcomes. Additionally, research institutions and public health organizations utilize mycology immunoassays to monitor and study the epidemiology of fungal infections, contributing to a better understanding of disease patterns and the development of targeted interventions. Overall, the Global Mycology Immunoassays Testing Market plays a critical role in enhancing the quality of healthcare delivery across various settings, supporting the early detection, prevention, and management of fungal infections.

Global Mycology Immunoassays Testing Market Outlook:

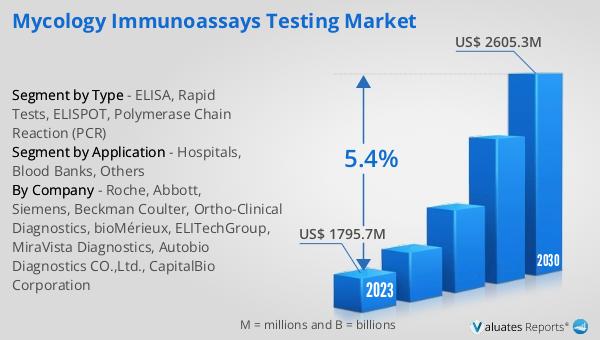

In 2024, the Global Mycology Immunoassays Testing Market was valued at approximately $1,993 million. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach around $2,865 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.4% throughout the forecast period. The expansion of this market can be attributed to several factors, including the increasing prevalence of fungal infections worldwide, advancements in diagnostic technologies, and a growing awareness of the importance of early and accurate diagnosis. As healthcare systems continue to prioritize patient outcomes, the demand for reliable and efficient mycology immunoassays is expected to rise. This market growth is also driven by ongoing research and development efforts aimed at enhancing test accuracy and expanding the range of detectable fungal pathogens. As a result, the Global Mycology Immunoassays Testing Market is poised to play an increasingly vital role in the diagnosis and management of fungal infections, ultimately contributing to improved healthcare delivery and patient outcomes.

| Report Metric | Details |

| Report Name | Mycology Immunoassays Testing Market |

| Accounted market size in year | US$ 1993 million |

| Forecasted market size in 2031 | US$ 2865 million |

| CAGR | 5.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Roche, Abbott, Siemens, Beckman Coulter, Ortho-Clinical Diagnostics, bioMérieux, ELITechGroup, MiraVista Diagnostics, Autobio Diagnostics CO.,Ltd., CapitalBio Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |