What is Global Empty Capsule Market?

The Global Empty Capsule Market is a significant segment within the pharmaceutical and nutraceutical industries, focusing on the production and distribution of empty capsules used for encapsulating various substances. These capsules serve as a vital component in the delivery of medications, vitamins, and supplements, offering a convenient and efficient method for oral consumption. The market encompasses a wide range of capsule types, including gelatin and vegetarian-based capsules, catering to diverse consumer preferences and dietary restrictions. The demand for empty capsules is driven by the growing pharmaceutical industry, increasing health consciousness among consumers, and the rising popularity of dietary supplements. Additionally, advancements in capsule manufacturing technologies have led to the development of innovative capsule designs, enhancing their functionality and appeal. The market is characterized by a competitive landscape, with numerous manufacturers striving to offer high-quality, customizable capsule solutions to meet the evolving needs of their clients. As the global population continues to grow and age, the demand for pharmaceuticals and nutraceuticals is expected to rise, further propelling the expansion of the Global Empty Capsule Market. This market plays a crucial role in supporting the healthcare and wellness sectors by providing essential tools for effective drug delivery and nutritional supplementation.

Gelatin (Hard)-based Capsules, Vegetarian-based Capsules in the Global Empty Capsule Market:

Gelatin (Hard)-based Capsules and Vegetarian-based Capsules are two primary types of capsules within the Global Empty Capsule Market, each offering unique benefits and applications. Gelatin capsules, traditionally made from animal-derived gelatin, are widely used due to their excellent film-forming properties, which ensure a robust and reliable encapsulation of active ingredients. These capsules are favored for their ability to dissolve quickly in the stomach, allowing for rapid release and absorption of the encapsulated substances. Gelatin capsules are particularly popular in the pharmaceutical industry for encapsulating drugs that require precise dosage and controlled release. However, the use of animal-derived gelatin has raised concerns among certain consumer groups, leading to the development and increasing popularity of vegetarian-based capsules. Vegetarian capsules are typically made from plant-derived materials such as hydroxypropyl methylcellulose (HPMC) or pullulan, offering a suitable alternative for individuals with dietary restrictions or ethical concerns regarding animal products. These capsules provide similar benefits to gelatin capsules, including excellent stability and compatibility with a wide range of substances. Vegetarian capsules are particularly favored in the nutraceutical and dietary supplement industries, where consumer demand for plant-based and vegan-friendly products is on the rise. The choice between gelatin and vegetarian capsules often depends on factors such as the nature of the encapsulated substance, target consumer preferences, and regulatory requirements. Manufacturers in the Global Empty Capsule Market continue to innovate and expand their product offerings to cater to the diverse needs of their clients, ensuring that both gelatin and vegetarian capsules remain integral components of the encapsulation industry. As consumer awareness and demand for transparency in product sourcing increase, the market for vegetarian capsules is expected to grow, providing a sustainable and ethical alternative to traditional gelatin capsules. This shift in consumer preferences is driving manufacturers to invest in research and development to enhance the performance and appeal of vegetarian capsules, ensuring they meet the rigorous standards of the pharmaceutical and nutraceutical industries. The Global Empty Capsule Market is poised for continued growth as it adapts to changing consumer demands and advances in encapsulation technology, offering a wide range of solutions to meet the diverse needs of the healthcare and wellness sectors.

Pharmaceuticals Companies, Cosmetics & Nutraceuticals Companies, Clinical Research Organisations (CROs) in the Global Empty Capsule Market:

The Global Empty Capsule Market finds extensive usage across various sectors, including Pharmaceuticals Companies, Cosmetics & Nutraceuticals Companies, and Clinical Research Organisations (CROs), each leveraging the unique benefits of empty capsules for their specific applications. In the pharmaceutical industry, empty capsules are a critical component in the formulation and delivery of medications. Pharmaceutical companies utilize these capsules to encapsulate active pharmaceutical ingredients (APIs), ensuring precise dosage and controlled release of drugs. The versatility of empty capsules allows for the encapsulation of a wide range of substances, including powders, granules, and even certain liquids, making them an essential tool in drug development and manufacturing. Additionally, the ability to customize capsules in terms of size, color, and imprinting provides pharmaceutical companies with the flexibility to differentiate their products and enhance brand recognition. In the cosmetics and nutraceuticals sectors, empty capsules are used to encapsulate vitamins, minerals, herbal extracts, and other dietary supplements, catering to the growing consumer demand for health and wellness products. These capsules offer a convenient and efficient method for delivering nutritional supplements, ensuring optimal absorption and bioavailability of the active ingredients. The use of vegetarian capsules in this sector is particularly noteworthy, as it aligns with the increasing consumer preference for plant-based and vegan-friendly products. Clinical Research Organisations (CROs) also rely on empty capsules for their research and development activities. CROs use these capsules to encapsulate investigational drugs and placebos for clinical trials, ensuring consistent and accurate dosing for study participants. The ability to produce customized capsules in small batches is particularly advantageous for CROs, as it allows for flexibility in trial design and rapid iteration of formulations. Overall, the Global Empty Capsule Market plays a vital role in supporting the pharmaceutical, cosmetics, and nutraceutical industries, providing essential tools for drug delivery, nutritional supplementation, and clinical research. As these industries continue to evolve and expand, the demand for high-quality, customizable empty capsules is expected to grow, driving innovation and development within the market.

Global Empty Capsule Market Outlook:

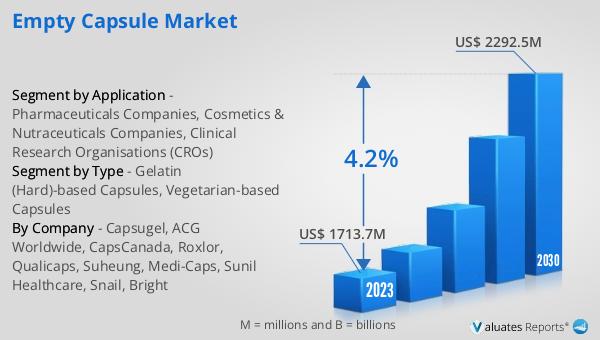

In 2024, the global market for empty capsules was valued at approximately $1,859 million. This market is anticipated to experience growth over the coming years, with projections indicating that it will reach an estimated size of $2,469 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.2% during the forecast period. The expansion of this market can be attributed to several factors, including the increasing demand for pharmaceuticals and dietary supplements, advancements in capsule manufacturing technologies, and the rising consumer preference for convenient and efficient drug delivery methods. As the global population continues to grow and age, the need for effective healthcare solutions is expected to rise, further driving the demand for empty capsules. Additionally, the growing awareness of health and wellness among consumers is fueling the demand for nutraceuticals and dietary supplements, contributing to the expansion of the empty capsule market. Manufacturers in this market are focusing on innovation and product development to meet the evolving needs of their clients, offering a wide range of capsule solutions that cater to diverse consumer preferences and regulatory requirements. The competitive landscape of the Global Empty Capsule Market is characterized by the presence of numerous manufacturers striving to offer high-quality, customizable capsule solutions. As the market continues to grow, manufacturers are investing in research and development to enhance the performance and appeal of their products, ensuring they meet the rigorous standards of the pharmaceutical and nutraceutical industries. The Global Empty Capsule Market is poised for continued growth as it adapts to changing consumer demands and advances in encapsulation technology, offering a wide range of solutions to meet the diverse needs of the healthcare and wellness sectors.

| Report Metric | Details |

| Report Name | Empty Capsule Market |

| Accounted market size in year | US$ 1859 million |

| Forecasted market size in 2031 | US$ 2469 million |

| CAGR | 4.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Capsugel, ACG Worldwide, CapsCanada, Roxlor, Qualicaps, Suheung, Medi-Caps, Sunil Healthcare, Snail, Bright |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |