What is Global Pharma Grade Glycine Market?

The Global Pharma Grade Glycine Market refers to the segment of the pharmaceutical industry that deals with the production and distribution of glycine, a non-essential amino acid, in its purest form for pharmaceutical applications. Glycine is a simple amino acid that plays a crucial role in various metabolic processes and is used in the synthesis of proteins. In the pharmaceutical industry, pharma grade glycine is utilized for its therapeutic properties, including its role as a neurotransmitter and its involvement in the synthesis of other important compounds like glutathione, creatine, and collagen. The market for pharma grade glycine is driven by its demand in the production of drugs and supplements that aim to improve health outcomes, particularly in areas such as neurology, oncology, and metabolic disorders. Additionally, glycine's role in enhancing the solubility and stability of certain drugs makes it a valuable component in pharmaceutical formulations. The global market for pharma grade glycine is influenced by factors such as advancements in pharmaceutical research, increasing prevalence of chronic diseases, and the growing demand for effective and safe therapeutic solutions. As the pharmaceutical industry continues to evolve, the demand for high-quality glycine is expected to rise, further driving the growth of this market segment.

Chloroacetic Acid Amide Solution, Biosynthesis in the Global Pharma Grade Glycine Market:

Chloroacetic Acid Amide Solution, Biosynthesis based on the Global Pharma Grade Glycine Market, represents a significant aspect of the pharmaceutical and chemical industries. Chloroacetic acid amide, commonly known as glycine, is synthesized through various methods, including chemical synthesis and biosynthesis. The biosynthesis of glycine involves the use of biological processes to produce this amino acid, which is essential for numerous physiological functions. In the context of the global pharma grade glycine market, biosynthesis offers a sustainable and efficient approach to producing high-quality glycine for pharmaceutical applications. The process of biosynthesis involves the use of microorganisms or enzymes to catalyze the conversion of precursor compounds into glycine. This method is considered environmentally friendly and cost-effective compared to traditional chemical synthesis, which often involves harsh chemicals and energy-intensive processes. The use of biosynthesis in the production of pharma grade glycine aligns with the growing trend towards green chemistry and sustainable manufacturing practices in the pharmaceutical industry. The demand for biosynthesized glycine is driven by its application in the formulation of drugs and supplements that target various health conditions. Glycine's role as a neurotransmitter and its involvement in the synthesis of important biomolecules make it a valuable component in the development of therapeutic solutions for neurological disorders, metabolic diseases, and cancer. Additionally, glycine's ability to enhance the solubility and stability of certain drugs further underscores its importance in pharmaceutical formulations. The global market for pharma grade glycine is characterized by the presence of several key players who are actively engaged in research and development to improve the efficiency and yield of biosynthesis processes. These companies are investing in advanced technologies and innovative approaches to enhance the production of glycine and meet the growing demand for high-quality pharmaceutical ingredients. The competitive landscape of the global pharma grade glycine market is shaped by factors such as technological advancements, regulatory frameworks, and market dynamics. Companies operating in this market are focused on expanding their product portfolios and strengthening their distribution networks to gain a competitive edge. The increasing prevalence of chronic diseases and the rising demand for effective therapeutic solutions are expected to drive the growth of the global pharma grade glycine market in the coming years. As the pharmaceutical industry continues to evolve, the adoption of biosynthesis as a sustainable and efficient method for producing glycine is likely to gain momentum, further propelling the growth of this market segment.

Hospitals, Labs in the Global Pharma Grade Glycine Market:

The usage of Global Pharma Grade Glycine Market in hospitals and labs is integral to the advancement of medical and scientific research. In hospitals, pharma grade glycine is utilized in various therapeutic applications due to its role as a neurotransmitter and its involvement in the synthesis of critical biomolecules. Glycine is often used in the formulation of drugs that target neurological disorders, such as epilepsy and schizophrenia, due to its ability to modulate neurotransmission and improve cognitive function. Additionally, glycine's anti-inflammatory and cytoprotective properties make it a valuable component in the treatment of metabolic disorders and cancer. In the hospital setting, glycine is also used as an irrigating solution during surgical procedures, particularly in urology, to prevent tissue damage and reduce the risk of complications. The demand for high-quality glycine in hospitals is driven by the need for effective and safe therapeutic solutions that can improve patient outcomes and enhance the quality of care. In laboratories, pharma grade glycine is used extensively in research and development activities. Glycine serves as a building block for the synthesis of proteins and other important biomolecules, making it an essential component in various biochemical assays and experiments. Researchers use glycine to study its role in cellular metabolism, neurotransmission, and disease pathogenesis. The availability of high-purity glycine is crucial for ensuring the accuracy and reliability of experimental results. In addition to its use in basic research, glycine is also employed in the development of new drugs and therapeutic agents. The pharmaceutical industry relies on glycine to enhance the solubility and stability of drug formulations, thereby improving their efficacy and safety. The global market for pharma grade glycine is characterized by the presence of several key players who are actively engaged in research and development to improve the quality and availability of glycine for hospital and laboratory use. These companies are investing in advanced technologies and innovative approaches to enhance the production of glycine and meet the growing demand for high-quality pharmaceutical ingredients. The competitive landscape of the global pharma grade glycine market is shaped by factors such as technological advancements, regulatory frameworks, and market dynamics. As the demand for effective therapeutic solutions and innovative research tools continues to rise, the usage of pharma grade glycine in hospitals and labs is expected to increase, further driving the growth of this market segment.

Global Pharma Grade Glycine Market Outlook:

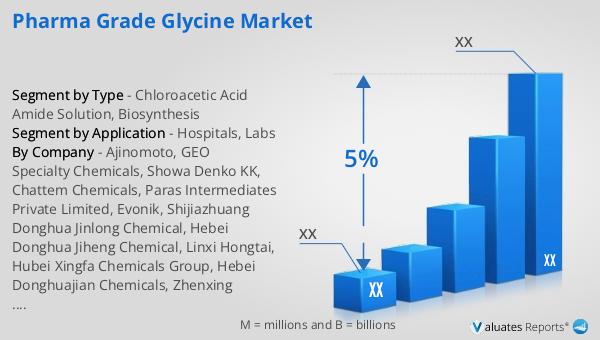

The outlook for the Global Pharma Grade Glycine Market is closely tied to the broader trends in the pharmaceutical industry. In 2022, the global pharmaceutical market was valued at approximately 1,475 billion USD, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth is indicative of the increasing demand for pharmaceutical products and the continuous advancements in medical research and drug development. In comparison, the chemical drug market experienced growth from 1,005 billion USD in 2018 to 1,094 billion USD in 2022. This expansion reflects the rising need for chemical-based therapeutic solutions and the ongoing innovation in drug formulations. The Global Pharma Grade Glycine Market is expected to benefit from these trends, as glycine plays a crucial role in the development of various pharmaceutical products. The demand for high-quality glycine is driven by its application in the formulation of drugs and supplements that target a wide range of health conditions, including neurological disorders, metabolic diseases, and cancer. As the pharmaceutical industry continues to evolve, the need for effective and safe therapeutic solutions is expected to drive the growth of the Global Pharma Grade Glycine Market. Companies operating in this market are focused on expanding their product portfolios and strengthening their distribution networks to meet the growing demand for high-quality pharmaceutical ingredients. The competitive landscape of the Global Pharma Grade Glycine Market is shaped by factors such as technological advancements, regulatory frameworks, and market dynamics. As the demand for effective therapeutic solutions and innovative research tools continues to rise, the outlook for the Global Pharma Grade Glycine Market remains positive, with significant growth opportunities on the horizon.

| Report Metric | Details |

| Report Name | Pharma Grade Glycine Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Ajinomoto, GEO Specialty Chemicals, Showa Denko KK, Chattem Chemicals, Paras Intermediates Private Limited, Evonik, Shijiazhuang Donghua Jinlong Chemical, Hebei Donghua Jiheng Chemical, Linxi Hongtai, Hubei Xingfa Chemicals Group, Hebei Donghuajian Chemicals, Zhenxing Chemical, Newtrend Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |