What is Global Critical Limb Ischemia Drug Market?

The Global Critical Limb Ischemia Drug Market is a specialized segment within the pharmaceutical industry focused on developing and providing medications for critical limb ischemia (CLI), a severe obstruction of the arteries which significantly reduces blood flow to the extremities, particularly the legs and feet. This condition can lead to severe pain, ulcers, and even gangrene, often necessitating amputation if not treated effectively. The market for these drugs is driven by the increasing prevalence of peripheral artery disease (PAD), aging populations, and the rising incidence of diabetes, which is a significant risk factor for CLI. Pharmaceutical companies are investing in research and development to create more effective treatments that can improve blood flow, reduce symptoms, and ultimately save limbs. The market is characterized by a mix of established drugs and innovative therapies in various stages of clinical trials, aiming to address the unmet medical needs of patients suffering from this debilitating condition. As healthcare systems worldwide recognize the importance of early intervention and effective management of CLI, the demand for these specialized drugs is expected to grow, offering hope for improved patient outcomes.

HC-016, JVS-100, NFx-101, NK-104 NP, Others in the Global Critical Limb Ischemia Drug Market:

HC-016, JVS-100, NFx-101, NK-104 NP, and other drugs represent a diverse array of therapeutic approaches within the Global Critical Limb Ischemia Drug Market, each with unique mechanisms of action and potential benefits for patients. HC-016 is a promising candidate that focuses on enhancing blood flow and tissue regeneration. It works by targeting specific pathways involved in angiogenesis, the process of forming new blood vessels, which is crucial for restoring circulation in ischemic limbs. Clinical trials have shown that HC-016 can significantly improve blood flow and reduce the risk of amputation in patients with CLI. JVS-100, on the other hand, is a gene therapy-based approach that aims to promote tissue repair and regeneration by delivering a therapeutic gene directly to the affected area. This innovative treatment has shown potential in preclinical studies to enhance healing and improve limb salvage rates. NFx-101 is another novel therapy that targets inflammation, a key factor in the progression of CLI. By reducing inflammation, NFx-101 helps to alleviate pain and prevent further tissue damage, offering a new avenue for managing this challenging condition. NK-104 NP is a nanoparticle-based drug that delivers a potent anti-inflammatory agent directly to the site of ischemia, maximizing its therapeutic effects while minimizing systemic side effects. This targeted approach has demonstrated promising results in early-stage trials, with patients experiencing significant improvements in symptoms and quality of life. In addition to these innovative therapies, the market also includes a range of other drugs that focus on different aspects of CLI management, such as pain relief, infection control, and wound healing. These treatments are often used in combination to provide a comprehensive approach to patient care, addressing the multifaceted nature of CLI and improving overall outcomes. As research continues to advance, the Global Critical Limb Ischemia Drug Market is poised to offer an expanding array of options for patients and healthcare providers, each contributing to the goal of reducing the burden of this debilitating condition.

Hospital, Home Care, ASCs in the Global Critical Limb Ischemia Drug Market:

The usage of drugs from the Global Critical Limb Ischemia Drug Market spans various healthcare settings, including hospitals, home care, and ambulatory surgical centers (ASCs), each playing a crucial role in the management and treatment of CLI. In hospitals, these drugs are often administered as part of a comprehensive treatment plan for patients with severe CLI, who may require intensive monitoring and intervention. Hospitals provide the necessary infrastructure for administering complex therapies, such as gene therapy or nanoparticle-based treatments, which may require specialized equipment and expertise. Additionally, hospitals are equipped to handle potential complications and provide immediate care, making them a critical setting for the initial management of CLI. In the home care setting, the focus shifts to maintaining and improving the patient's condition through ongoing medication management and monitoring. Home care allows patients to receive treatment in a comfortable and familiar environment, which can enhance adherence to medication regimens and improve overall quality of life. Nurses and healthcare professionals play a vital role in educating patients and caregivers about the proper administration of drugs, potential side effects, and the importance of regular follow-up appointments. This setting is particularly beneficial for patients with mobility issues or those who prefer to avoid frequent hospital visits. Ambulatory surgical centers (ASCs) offer a middle ground between hospital and home care, providing a convenient and cost-effective option for patients requiring minor surgical interventions or procedures related to CLI. ASCs are equipped to perform procedures such as angioplasty or stent placement, which can improve blood flow and complement the effects of pharmacological treatments. The use of CLI drugs in ASCs is often part of a broader treatment strategy, aimed at optimizing patient outcomes and reducing the need for more invasive surgeries. Overall, the integration of CLI drugs across these diverse healthcare settings highlights the importance of a multidisciplinary approach to managing this complex condition, ensuring that patients receive the most appropriate and effective care at every stage of their treatment journey.

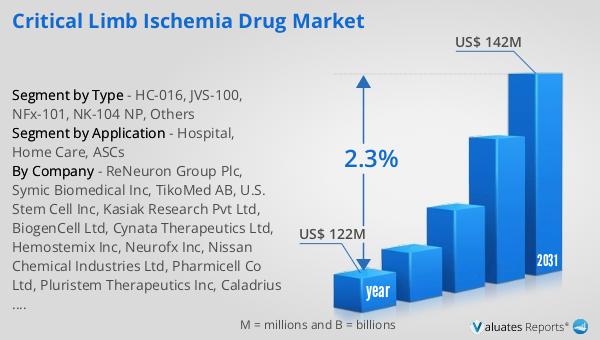

Global Critical Limb Ischemia Drug Market Outlook:

The global market for Critical Limb Ischemia Drugs was valued at approximately $122 million in 2024, with projections indicating an increase to around $142 million by 2031, reflecting a compound annual growth rate (CAGR) of 2.3% over the forecast period. This growth is indicative of the rising demand for effective treatments for critical limb ischemia, driven by factors such as an aging population and the increasing prevalence of diabetes and peripheral artery disease. In the broader context, the global pharmaceutical market was valued at $1,475 billion in 2022, with an expected CAGR of 5% over the next six years. This growth trajectory underscores the expanding scope of the pharmaceutical industry as a whole, driven by advancements in drug development and an increasing focus on personalized medicine. Comparatively, the chemical drug market has also shown significant growth, increasing from $1,005 billion in 2018 to $1,094 billion in 2022. This growth reflects the ongoing demand for chemical-based therapies across various therapeutic areas, including critical limb ischemia. The steady growth of the Critical Limb Ischemia Drug Market, in particular, highlights the importance of continued investment in research and development to address the unmet medical needs of patients suffering from this debilitating condition. As the market evolves, it is expected to offer a wider range of treatment options, improving patient outcomes and enhancing the quality of life for those affected by CLI.

| Report Metric | Details |

| Report Name | Critical Limb Ischemia Drug Market |

| Accounted market size in year | US$ 122 million |

| Forecasted market size in 2031 | US$ 142 million |

| CAGR | 2.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ReNeuron Group Plc, Symic Biomedical Inc, TikoMed AB, U.S. Stem Cell Inc, Kasiak Research Pvt Ltd, BiogenCell Ltd, Cynata Therapeutics Ltd, Hemostemix Inc, Neurofx Inc, Nissan Chemical Industries Ltd, Pharmicell Co Ltd, Pluristem Therapeutics Inc, Caladrius Biosciences Inc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |