What is Global Motorcycle Half Helmet Market?

The Global Motorcycle Half Helmet Market is a segment of the broader motorcycle helmet industry, focusing specifically on half helmets. These helmets are designed to cover the top of the head and provide protection while allowing for more ventilation and a wider field of vision compared to full-face helmets. They are popular among riders who prefer a lighter, less restrictive option. The market for these helmets is driven by several factors, including the increasing popularity of motorcycles as a mode of transportation and leisure activity, particularly in urban areas where traffic congestion is a concern. Additionally, the rising awareness of road safety and the implementation of stringent regulations regarding helmet use in many countries have contributed to the growth of this market. Manufacturers are continuously innovating to improve the safety features, comfort, and aesthetics of half helmets, which further fuels consumer interest. The market is also influenced by fashion trends, as many riders seek helmets that not only provide safety but also complement their personal style. Overall, the Global Motorcycle Half Helmet Market is a dynamic and evolving sector, responding to changes in consumer preferences, technological advancements, and regulatory landscapes.

Polycarbonate, ABS Alloy, Carbon Fiber, Other in the Global Motorcycle Half Helmet Market:

Polycarbonate, ABS Alloy, Carbon Fiber, and other materials play a crucial role in the Global Motorcycle Half Helmet Market, each offering distinct advantages and characteristics that cater to different consumer needs. Polycarbonate is a popular choice due to its excellent impact resistance and affordability. It is a type of thermoplastic polymer that can absorb significant amounts of energy upon impact, making it an ideal material for helmets. Polycarbonate helmets are lightweight, which enhances rider comfort, and they are also easy to mold, allowing manufacturers to create various designs and styles. However, they may not offer the same level of durability as some other materials over time. ABS Alloy, or Acrylonitrile Butadiene Styrene, is another widely used material in the production of motorcycle half helmets. It is known for its toughness and resistance to physical impacts, making it a reliable choice for safety gear. ABS helmets are generally more affordable than those made from advanced materials like carbon fiber, making them accessible to a broader range of consumers. They also offer good resistance to heat and chemicals, which can be beneficial in various riding conditions. Carbon Fiber is considered a premium material in the helmet market due to its exceptional strength-to-weight ratio. Helmets made from carbon fiber are incredibly strong and lightweight, providing superior protection without compromising on comfort. The material's high tensile strength ensures that it can withstand significant impacts, making it a preferred choice for riders who prioritize safety. However, carbon fiber helmets tend to be more expensive, which can limit their accessibility to some consumers. Despite the higher cost, many riders are willing to invest in carbon fiber helmets for their enhanced safety features and sleek appearance. Other materials used in the production of motorcycle half helmets include fiberglass and composite materials. Fiberglass helmets offer a good balance between strength and weight, providing adequate protection while remaining relatively lightweight. They are often reinforced with additional materials to enhance their durability and impact resistance. Composite materials, on the other hand, are engineered to combine the best properties of different materials, resulting in helmets that offer a high level of protection and comfort. These materials are often used in high-end helmets, where performance and safety are paramount. In conclusion, the choice of material in the Global Motorcycle Half Helmet Market is influenced by factors such as safety, comfort, cost, and consumer preferences. Manufacturers continue to explore new materials and technologies to enhance the performance and appeal of their products, ensuring that riders have access to helmets that meet their specific needs and preferences.

Online, Offline in the Global Motorcycle Half Helmet Market:

The usage of Global Motorcycle Half Helmet Market products can be categorized into two main areas: online and offline. In the online segment, e-commerce platforms have become a significant channel for purchasing motorcycle half helmets. The convenience of online shopping, coupled with the ability to compare prices and read reviews, has made it an attractive option for consumers. Online retailers often offer a wide range of helmet brands and models, allowing customers to find products that suit their preferences and budget. Additionally, the rise of digital marketing and social media has enabled manufacturers and retailers to reach a broader audience, promoting their products to potential customers worldwide. Online platforms also provide detailed product descriptions and specifications, helping consumers make informed purchasing decisions. However, the inability to physically try on helmets before purchase can be a drawback for some buyers, leading to potential issues with fit and comfort. In the offline segment, traditional brick-and-mortar stores continue to play a vital role in the distribution of motorcycle half helmets. Physical stores offer the advantage of allowing customers to try on helmets and assess their fit and comfort before making a purchase. This hands-on experience can be crucial for ensuring that the helmet provides the necessary protection and comfort for the rider. Additionally, in-store staff can offer personalized advice and recommendations based on the customer's needs and preferences. Many consumers prefer the assurance of purchasing from a physical store, where they can directly interact with the product and receive immediate assistance if needed. Moreover, offline channels often include specialty motorcycle shops and dealerships, which may offer a curated selection of high-quality helmets and accessories. These stores often cater to motorcycle enthusiasts who value expert advice and a personalized shopping experience. In conclusion, both online and offline channels play a significant role in the Global Motorcycle Half Helmet Market, each offering unique advantages and catering to different consumer preferences. The choice between online and offline shopping often depends on factors such as convenience, the desire for a hands-on experience, and the level of customer service required. As the market continues to evolve, manufacturers and retailers are likely to adopt a multi-channel approach, leveraging the strengths of both online and offline platforms to reach a diverse customer base.

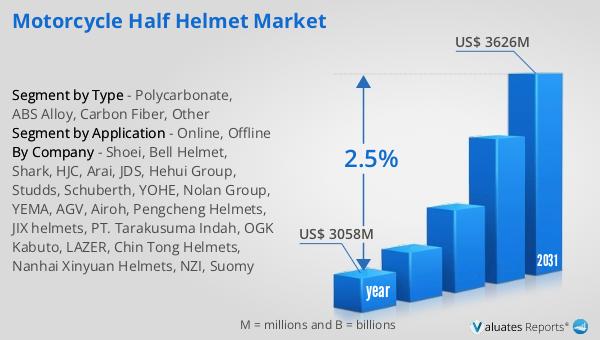

Global Motorcycle Half Helmet Market Outlook:

The outlook for the Global Motorcycle Half Helmet Market indicates a steady growth trajectory over the coming years. In 2024, the market was valued at approximately $3,058 million, reflecting the demand for these helmets among motorcycle enthusiasts and safety-conscious riders. By 2031, the market is expected to expand to a revised size of around $3,626 million, driven by a compound annual growth rate (CAGR) of 2.5% during the forecast period. This growth can be attributed to several factors, including the increasing popularity of motorcycles as a convenient and economical mode of transportation, particularly in urban areas where traffic congestion is a significant concern. Additionally, the rising awareness of road safety and the implementation of stringent regulations mandating helmet use in many countries have contributed to the market's expansion. Manufacturers are also focusing on innovation, developing helmets with enhanced safety features, improved comfort, and stylish designs to attract a broader range of consumers. As a result, the Global Motorcycle Half Helmet Market is poised for continued growth, driven by a combination of regulatory support, consumer demand, and technological advancements.

| Report Metric | Details |

| Report Name | Motorcycle Half Helmet Market |

| Accounted market size in year | US$ 3058 million |

| Forecasted market size in 2031 | US$ 3626 million |

| CAGR | 2.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Shoei, Bell Helmet, Shark, HJC, Arai, JDS, Hehui Group, Studds, Schuberth, YOHE, Nolan Group, YEMA, AGV, Airoh, Pengcheng Helmets, JIX helmets, PT. Tarakusuma Indah, OGK Kabuto, LAZER, Chin Tong Helmets, Nanhai Xinyuan Helmets, NZI, Suomy |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |