What is Global NiCd Battery Charging IC Market?

The Global NiCd Battery Charging IC Market is a specialized segment within the broader semiconductor industry, focusing on integrated circuits (ICs) designed to charge nickel-cadmium (NiCd) batteries. NiCd batteries, known for their durability and ability to deliver high discharge rates, are used in various applications, from consumer electronics to industrial equipment. The charging ICs are crucial for managing the charging process, ensuring that the batteries are charged efficiently and safely. These ICs help prevent overcharging, which can lead to reduced battery life or even damage. The market for these charging ICs is driven by the demand for reliable and efficient power solutions across different sectors. As technology advances, the need for more sophisticated charging solutions grows, pushing the development of ICs that can handle complex charging algorithms and provide better energy management. The market is characterized by continuous innovation, with manufacturers striving to improve the efficiency, size, and cost-effectiveness of their products. This market is also influenced by the broader trends in the semiconductor industry, including the push for miniaturization and the integration of more functionalities into single chips. Overall, the Global NiCd Battery Charging IC Market plays a vital role in supporting the energy needs of various industries by providing advanced charging solutions.

Linear Battery Chargers, Switching Battery Chargers, Module Battery Chargers, Buck/Boost Battery Chargers, Other in the Global NiCd Battery Charging IC Market:

In the Global NiCd Battery Charging IC Market, several types of battery chargers are utilized, each with its unique characteristics and applications. Linear battery chargers are among the simplest and most cost-effective solutions. They operate by using a linear regulator to control the charging current, making them ideal for low-power applications where efficiency is not the primary concern. These chargers are easy to design and implement, but they tend to generate more heat and are less efficient compared to other types. Switching battery chargers, on the other hand, use a switching regulator to convert the input voltage to the desired charging voltage. This method is more efficient than linear charging, as it reduces power loss and heat generation. Switching chargers are suitable for applications where efficiency and thermal management are critical, such as in portable electronics and automotive systems. Module battery chargers are pre-packaged solutions that integrate all the necessary components for charging a battery. These modules simplify the design process and reduce time-to-market for manufacturers. They are often used in applications where space is limited, and a compact solution is required. Buck/Boost battery chargers are versatile solutions that can handle a wide range of input and output voltages. They are capable of stepping up or stepping down the voltage as needed, making them ideal for applications with varying power requirements. These chargers are commonly used in devices that need to operate over a wide range of conditions, such as in renewable energy systems and electric vehicles. Other types of chargers in the market include those designed for specific applications or battery chemistries, offering tailored solutions to meet the unique needs of different industries. Each type of charger plays a crucial role in the Global NiCd Battery Charging IC Market, providing the necessary technology to ensure efficient and reliable battery charging across various applications.

Consumer Electronics, Automotive, Power Industry, Other in the Global NiCd Battery Charging IC Market:

The Global NiCd Battery Charging IC Market finds its usage across several key areas, including consumer electronics, automotive, power industry, and others. In consumer electronics, NiCd battery charging ICs are used in devices such as cordless phones, power tools, and remote controls. These ICs ensure that the batteries in these devices are charged efficiently, providing users with reliable power and extending the lifespan of the batteries. The demand for portable and wireless devices continues to drive the need for advanced charging solutions in this sector. In the automotive industry, NiCd battery charging ICs are used in various applications, including electric vehicles (EVs), hybrid vehicles, and automotive accessories. These ICs help manage the charging of batteries used in these vehicles, ensuring optimal performance and safety. As the automotive industry shifts towards more sustainable and energy-efficient solutions, the demand for sophisticated charging ICs is expected to grow. In the power industry, NiCd battery charging ICs are used in backup power systems, uninterruptible power supplies (UPS), and renewable energy systems. These ICs play a critical role in ensuring that the batteries in these systems are charged and maintained properly, providing reliable power during outages or when renewable energy sources are unavailable. Other areas where NiCd battery charging ICs are used include industrial equipment, medical devices, and telecommunications. In these applications, the ICs provide the necessary technology to ensure that batteries are charged efficiently and safely, supporting the reliable operation of critical systems and devices. Overall, the Global NiCd Battery Charging IC Market plays a vital role in supporting the energy needs of various industries by providing advanced charging solutions that enhance the performance and reliability of battery-powered devices.

Global NiCd Battery Charging IC Market Outlook:

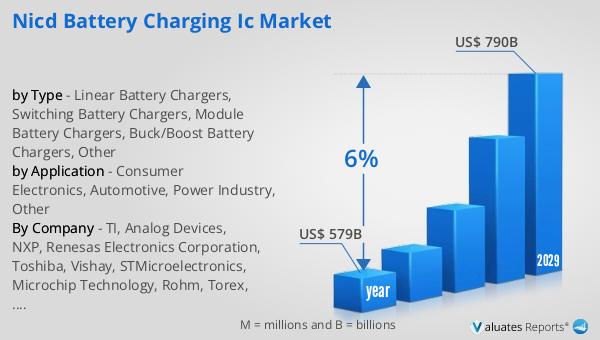

The global semiconductor market, which includes the Global NiCd Battery Charging IC Market, was valued at approximately $579 billion in 2022. This market is projected to grow significantly, reaching around $790 billion by 2029, with a compound annual growth rate (CAGR) of 6% during the forecast period. This growth is driven by the increasing demand for semiconductors across various industries, including consumer electronics, automotive, and industrial applications. The rise in demand for advanced technologies, such as artificial intelligence, the Internet of Things (IoT), and 5G connectivity, is also contributing to the expansion of the semiconductor market. As these technologies become more prevalent, the need for efficient and reliable power solutions, such as NiCd battery charging ICs, is expected to increase. The market is characterized by continuous innovation, with manufacturers striving to develop more efficient, compact, and cost-effective solutions to meet the evolving needs of their customers. The growth of the semiconductor market presents significant opportunities for companies operating in the Global NiCd Battery Charging IC Market, as they can leverage advancements in semiconductor technology to enhance their products and expand their market reach. Overall, the outlook for the Global NiCd Battery Charging IC Market is positive, with strong growth potential driven by the increasing demand for advanced charging solutions across various industries.

| Report Metric | Details |

| Report Name | NiCd Battery Charging IC Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TI, Analog Devices, NXP, Renesas Electronics Corporation, Toshiba, Vishay, STMicroelectronics, Microchip Technology, Rohm, Torex, Servoflo, FTDI Chip, Diodes Incorporated, Semtech, Maxim Integrated, New Japan Radio, ON Semiconductor |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |