What is Global Light Guide Plate for LCTV Market?

The Global Light Guide Plate (LGP) for Liquid Crystal Television (LCTV) Market is a crucial component in the display technology industry. Light Guide Plates are essential in distributing light evenly across the screen, ensuring that the display is bright and clear. These plates are used in LCD TVs to guide the light from the backlight to the viewer's eyes, enhancing the overall viewing experience. The market for these plates is driven by the increasing demand for high-quality displays in televisions, which are becoming larger and more advanced. As consumers seek better picture quality and more immersive viewing experiences, the demand for efficient and effective light guide plates continues to grow. The market is characterized by technological advancements and innovations aimed at improving the efficiency and performance of these plates. Manufacturers are focusing on developing plates that offer better light distribution, reduced energy consumption, and enhanced durability. The global market for LGPs is competitive, with several key players striving to gain a larger market share by offering innovative solutions and superior products. As the television industry continues to evolve, the role of light guide plates becomes increasingly important in delivering the high-quality displays that consumers expect.

Print LGP, Print-less LGP in the Global Light Guide Plate for LCTV Market:

In the Global Light Guide Plate for LCTV Market, there are two primary types of LGPs: Print LGP and Print-less LGP. Print LGPs are traditional light guide plates that use a printed pattern to distribute light evenly across the screen. This pattern is typically printed on the surface of the plate and is designed to reflect and refract light in a way that ensures uniform brightness across the display. Print LGPs have been widely used in the industry due to their effectiveness and relatively low cost. However, they have certain limitations, such as the potential for uneven light distribution and the need for precise manufacturing processes to ensure quality. On the other hand, Print-less LGPs represent a more modern approach to light guide plate technology. These plates do not rely on printed patterns to distribute light. Instead, they use advanced optical designs and materials to achieve uniform light distribution. Print-less LGPs offer several advantages over their printed counterparts, including improved light efficiency, reduced manufacturing complexity, and enhanced durability. They are particularly well-suited for use in larger displays, where uniform light distribution is critical. The shift towards Print-less LGPs is driven by the demand for higher-quality displays and the need for more efficient and sustainable manufacturing processes. As the market for LCTV continues to grow, the adoption of Print-less LGPs is expected to increase, as manufacturers seek to meet the demands of consumers for better picture quality and more energy-efficient products. The competition between Print and Print-less LGPs is a key dynamic in the market, with manufacturers continually innovating to improve the performance and cost-effectiveness of their products. This competition is likely to drive further advancements in light guide plate technology, benefiting consumers with better and more affordable display options.

Below 40 inch LCTV, 40-50 inch LCTV, 50-70 inch LCTV, Above 70 inch LCTV in the Global Light Guide Plate for LCTV Market:

The usage of Global Light Guide Plates in LCTV varies significantly across different screen sizes, each with its unique requirements and challenges. For LCTVs below 40 inches, the focus is primarily on cost-effectiveness and compact design. Light guide plates for these smaller screens need to be efficient in light distribution while maintaining a low profile to fit within the slim design of modern televisions. Manufacturers often prioritize affordability and energy efficiency for this segment, as consumers in this category are typically more price-sensitive. In the 40-50 inch LCTV range, the demand for better picture quality becomes more pronounced. Light guide plates for these mid-sized screens must balance performance with cost, providing uniform light distribution to enhance the viewing experience. This segment often sees a mix of both Print and Print-less LGPs, as manufacturers aim to offer a variety of options to meet different consumer preferences. For larger screens, such as those in the 50-70 inch range, the requirements for light guide plates become more complex. These screens demand high-performance LGPs that can deliver consistent brightness and color accuracy across the entire display. Print-less LGPs are increasingly popular in this segment due to their superior light distribution capabilities and efficiency. As consumers in this category are often willing to pay a premium for better picture quality, manufacturers focus on developing advanced LGPs that enhance the overall viewing experience. Finally, for LCTVs above 70 inches, the challenge lies in maintaining uniform light distribution across a very large screen. Light guide plates for these ultra-large displays must be exceptionally efficient and durable, as any inconsistencies in light distribution can significantly impact the viewing experience. Print-less LGPs are the preferred choice for this segment, as they offer the best performance in terms of light efficiency and distribution. Manufacturers in this category invest heavily in research and development to create LGPs that meet the high standards expected by consumers of large-screen televisions. Overall, the usage of light guide plates in LCTV varies across different screen sizes, with manufacturers tailoring their products to meet the specific needs and preferences of consumers in each segment.

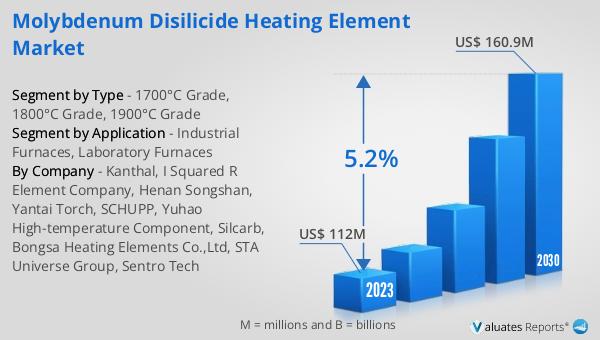

Global Light Guide Plate for LCTV Market Outlook:

In 2024, the global market for Light Guide Plates used in LCTV was valued at approximately $908 million. This market is anticipated to expand, reaching an estimated value of $1,288 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.2% over the forecast period. This growth is indicative of the increasing demand for high-quality display technologies in the television industry. The market is dominated by a few major players, with the top three companies accounting for over 40% of the global market share. This concentration highlights the competitive nature of the industry, where leading companies leverage their technological expertise and innovation capabilities to maintain their market positions. The growth in this market is driven by several factors, including advancements in display technology, increasing consumer demand for larger and more advanced televisions, and the ongoing shift towards more energy-efficient and sustainable products. As the market continues to evolve, companies are expected to focus on developing new and improved light guide plate technologies that offer better performance, efficiency, and durability. This competitive landscape encourages continuous innovation, benefiting consumers with access to higher-quality and more affordable display options. The projected growth of the Light Guide Plate market underscores the importance of these components in the future of television technology, as they play a critical role in delivering the high-quality viewing experiences that consumers increasingly demand.

| Report Metric | Details |

| Report Name | Light Guide Plate for LCTV Market |

| Accounted market size in year | US$ 908 million |

| Forecasted market size in 2031 | US$ 1288 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Mitsubishi Riyang, Chimei, Fensheng Opto-electronics, Sumitomo Chemical, Asahi Kasei, Kuraray, Seronics, S. Polytech Co., Ltd, Global Lighting Technologies, Entire, Kolon Industries |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |