What is Global Micro Programmable Logic Controller Market?

The Global Micro Programmable Logic Controller (PLC) Market is a dynamic segment within the broader automation industry, focusing on compact and versatile control devices used in various industrial applications. These micro PLCs are essentially small-scale computers designed to automate specific processes, offering a cost-effective solution for controlling machinery and processes in industries ranging from manufacturing to utilities. They are particularly valued for their ability to handle complex tasks with precision and reliability, despite their compact size. The market for these devices is driven by the increasing demand for automation across industries, as businesses seek to enhance efficiency, reduce human error, and improve overall productivity. As industries continue to evolve with technological advancements, the role of micro PLCs becomes even more critical, providing the necessary control and flexibility required in modern industrial operations. The global market for micro PLCs is characterized by continuous innovation, with manufacturers striving to develop more advanced and user-friendly models to meet the diverse needs of their clients. This market is expected to grow steadily as more industries recognize the benefits of integrating micro PLCs into their operations, thereby driving demand for these versatile control solutions.

Hardware, Services, Software in the Global Micro Programmable Logic Controller Market:

In the Global Micro Programmable Logic Controller Market, the components can be broadly categorized into hardware, services, and software, each playing a crucial role in the functionality and application of micro PLCs. Starting with hardware, this includes the physical components of the PLCs such as the processor, input/output modules, power supply, and communication interfaces. The hardware is designed to withstand harsh industrial environments, ensuring durability and reliability. The processor is the brain of the PLC, executing control instructions and managing data flow. Input/output modules facilitate interaction with external devices, allowing the PLC to receive signals from sensors and send commands to actuators. Communication interfaces enable connectivity with other devices and systems, supporting integration into larger automation networks. Moving on to services, these encompass a range of support activities that ensure the effective deployment and operation of micro PLCs. Services include installation, maintenance, and technical support, which are essential for optimizing the performance and longevity of the PLCs. Installation services ensure that the PLCs are correctly set up and configured to meet specific operational requirements. Maintenance services involve regular inspections and updates to prevent downtime and extend the lifespan of the devices. Technical support provides users with assistance in troubleshooting and resolving any issues that may arise during operation. Lastly, software is a critical component that enables the programming and customization of micro PLCs. Software tools allow users to create and modify control programs, tailoring the PLCs to perform specific tasks and processes. These tools often feature user-friendly interfaces and advanced functionalities, such as simulation and debugging, to facilitate efficient program development. Additionally, software updates are periodically released to enhance performance and introduce new features, ensuring that the PLCs remain up-to-date with the latest technological advancements. Together, hardware, services, and software form the backbone of the Global Micro Programmable Logic Controller Market, providing the necessary infrastructure and support for the widespread adoption and utilization of these versatile control devices across various industries.

Steel Industry, Petrochemical and Gas Industry, Power Industry, Automobile Industry, Others in the Global Micro Programmable Logic Controller Market:

The Global Micro Programmable Logic Controller Market finds extensive application across several key industries, each leveraging the unique capabilities of micro PLCs to enhance operational efficiency and productivity. In the steel industry, micro PLCs are used to automate processes such as material handling, temperature control, and quality inspection. By integrating micro PLCs into their operations, steel manufacturers can achieve precise control over production parameters, reduce waste, and improve product quality. In the petrochemical and gas industry, micro PLCs play a vital role in monitoring and controlling complex processes such as refining, distillation, and chemical reactions. These devices ensure the safe and efficient operation of critical equipment, minimizing the risk of accidents and optimizing resource utilization. The power industry also benefits from the use of micro PLCs, particularly in the management of power generation and distribution systems. Micro PLCs enable real-time monitoring and control of electrical parameters, facilitating the efficient operation of power plants and ensuring a stable supply of electricity. In the automobile industry, micro PLCs are employed in various stages of the manufacturing process, from assembly line automation to quality control. By automating repetitive tasks and enabling precise control over production processes, micro PLCs help automotive manufacturers improve production efficiency and maintain high standards of quality. Beyond these industries, micro PLCs are also used in a wide range of other applications, including water and wastewater treatment, food and beverage processing, and building automation. In each of these areas, micro PLCs provide the flexibility and reliability needed to optimize operations and achieve desired outcomes. As industries continue to embrace automation and digitalization, the demand for micro PLCs is expected to grow, driving further innovation and development in the Global Micro Programmable Logic Controller Market.

Global Micro Programmable Logic Controller Market Outlook:

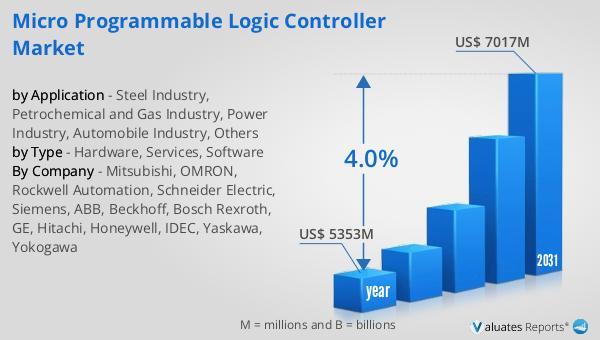

The global market for Micro Programmable Logic Controllers was valued at $5,353 million in 2024, with projections indicating it will expand to a revised size of $7,017 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.0% over the forecast period. This growth trajectory underscores the increasing adoption of micro PLCs across various industries, driven by the need for efficient and reliable automation solutions. As businesses strive to enhance productivity and reduce operational costs, the demand for compact and versatile control devices like micro PLCs is on the rise. These devices offer a cost-effective solution for automating complex processes, enabling industries to achieve greater precision and control over their operations. The projected growth of the Global Micro Programmable Logic Controller Market is also indicative of the ongoing technological advancements in the field, with manufacturers continuously innovating to develop more advanced and user-friendly models. As industries continue to evolve and embrace digitalization, the role of micro PLCs becomes increasingly critical, providing the necessary control and flexibility required in modern industrial operations. The steady growth of this market is a testament to the value and importance of micro PLCs in driving efficiency and productivity across a wide range of applications.

| Report Metric | Details |

| Report Name | Micro Programmable Logic Controller Market |

| Accounted market size in year | US$ 5353 million |

| Forecasted market size in 2031 | US$ 7017 million |

| CAGR | 4.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Mitsubishi, OMRON, Rockwell Automation, Schneider Electric, Siemens, ABB, Beckhoff, Bosch Rexroth, GE, Hitachi, Honeywell, IDEC, Yaskawa, Yokogawa |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |