What is Global Near IR Cameras Market?

The Global Near IR Cameras Market refers to the worldwide industry focused on the production and distribution of near-infrared (NIR) cameras. These cameras are designed to capture images using near-infrared light, which is just beyond the visible spectrum for humans. NIR cameras are particularly useful in various applications because they can see through certain materials and detect heat, making them valuable in fields like surveillance, agriculture, and industrial inspection. The market for these cameras is driven by technological advancements, increasing demand for high-quality imaging, and the growing need for surveillance and security solutions. As industries continue to adopt automation and advanced imaging technologies, the demand for NIR cameras is expected to rise. These cameras are also becoming more affordable, which further fuels their adoption across different sectors. The global market is characterized by a mix of established players and new entrants, all striving to innovate and capture a larger share of the market. The competition is intense, with companies focusing on improving camera sensitivity, resolution, and integration capabilities to meet the diverse needs of their customers.

CCD NIR Cameras, CMOS NIR Cameras, Others in the Global Near IR Cameras Market:

CCD NIR Cameras, CMOS NIR Cameras, and other types of NIR cameras each have unique characteristics and applications within the Global Near IR Cameras Market. CCD (Charge-Coupled Device) NIR Cameras are known for their high-quality image capture and sensitivity to light. They are often used in scientific research and industrial applications where precision is crucial. CCD cameras excel in low-light conditions and provide excellent image clarity, making them ideal for applications such as astronomy, microscopy, and medical imaging. However, they tend to be more expensive and consume more power compared to other types of cameras. On the other hand, CMOS (Complementary Metal-Oxide-Semiconductor) NIR Cameras are gaining popularity due to their cost-effectiveness and lower power consumption. CMOS sensors are integrated into a single chip, which makes them more compact and easier to produce in large quantities. These cameras are widely used in consumer electronics, automotive industries, and security systems. CMOS NIR cameras offer faster processing speeds and are more adaptable to different lighting conditions, although they may not always match the image quality of CCD cameras. Other types of NIR cameras include InGaAs (Indium Gallium Arsenide) cameras, which are specifically designed for short-wave infrared imaging. These cameras are used in specialized applications such as telecommunications, spectroscopy, and military surveillance. InGaAs cameras are highly sensitive to infrared light and can detect wavelengths that other cameras cannot, making them invaluable in certain niche markets. Despite their advantages, they are often more expensive and less widely used than CCD and CMOS cameras. The choice between these types of NIR cameras depends largely on the specific requirements of the application, including factors such as budget, image quality, and environmental conditions. As technology continues to evolve, manufacturers are working to improve the performance and affordability of all types of NIR cameras, thereby expanding their potential applications and market reach.

Industry, Measurement & Detection, Others in the Global Near IR Cameras Market:

The usage of Global Near IR Cameras Market spans various areas, including industry, measurement and detection, and other specialized fields. In industrial settings, NIR cameras are employed for quality control and inspection processes. They can detect defects in products that are not visible to the naked eye, such as cracks, contamination, or inconsistencies in materials. This capability is particularly valuable in manufacturing sectors like electronics, automotive, and pharmaceuticals, where precision and quality assurance are paramount. NIR cameras are also used in process monitoring, helping to optimize production lines and reduce waste by providing real-time feedback on the manufacturing process. In the realm of measurement and detection, NIR cameras play a crucial role in scientific research and environmental monitoring. They are used to measure temperature variations, detect gas leaks, and monitor plant health in agriculture. By capturing images in the near-infrared spectrum, these cameras can provide insights into phenomena that are not visible in the standard visible light spectrum. For instance, in agriculture, NIR cameras can assess crop health by detecting variations in plant reflectance, which can indicate stress or disease. This information is invaluable for farmers looking to optimize yield and reduce the use of pesticides. Beyond industry and measurement, NIR cameras find applications in other areas such as security and surveillance, where they are used to enhance visibility in low-light conditions. They are also used in medical imaging, where their ability to penetrate tissues can aid in non-invasive diagnostics. In the entertainment industry, NIR cameras are used in special effects and virtual reality applications, where they can create immersive experiences by capturing images that are not possible with traditional cameras. The versatility of NIR cameras makes them a valuable tool across a wide range of applications, and as technology advances, their usage is likely to expand even further.

Global Near IR Cameras Market Outlook:

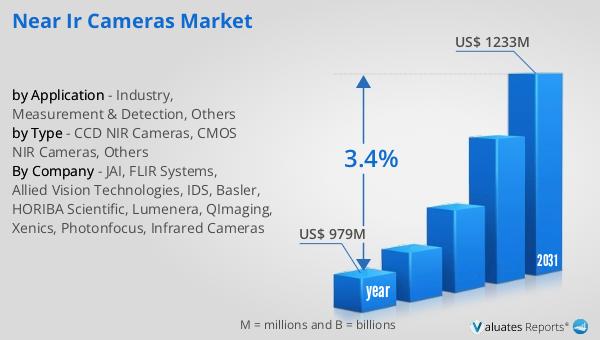

The global market for Near IR Cameras was valued at approximately $979 million in 2024, and it is anticipated to grow to a revised size of around $1,233 million by 2031. This growth represents a compound annual growth rate (CAGR) of 3.4% over the forecast period. The market is characterized by a high level of competition, with the top five manufacturers holding a significant share of over 55%. This indicates a concentrated market where a few key players dominate, driving innovation and setting industry standards. The growth in the market can be attributed to several factors, including the increasing demand for advanced imaging solutions across various sectors such as security, industrial inspection, and scientific research. As industries continue to embrace automation and digitalization, the need for high-quality, reliable imaging technologies like NIR cameras is expected to rise. Additionally, technological advancements are making these cameras more accessible and affordable, further fueling market growth. The competitive landscape of the market is shaped by the efforts of leading manufacturers to enhance their product offerings and expand their market presence. Companies are investing in research and development to improve camera performance, such as enhancing sensitivity, resolution, and integration capabilities. This focus on innovation is crucial for maintaining a competitive edge in a rapidly evolving market. As the market continues to grow, it presents opportunities for both established players and new entrants to capture a share of the expanding demand for NIR cameras.

| Report Metric | Details |

| Report Name | Near IR Cameras Market |

| Accounted market size in year | US$ 979 million |

| Forecasted market size in 2031 | US$ 1233 million |

| CAGR | 3.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | JAI, FLIR Systems, Allied Vision Technologies, IDS, Basler, HORIBA Scientific, Lumenera, QImaging, Xenics, Photonfocus, Infrared Cameras |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |