What is Global Mechanical Presses Market?

The Global Mechanical Presses Market is a significant segment within the manufacturing industry, focusing on machines that shape or cut materials using mechanical force. These presses are essential in various industrial applications, providing the necessary force to mold, cut, or shape metal and other materials into desired forms. Mechanical presses are widely used due to their efficiency, precision, and ability to handle high-volume production tasks. They come in various sizes and capacities, catering to different industrial needs, from small-scale operations to large manufacturing plants. The market is driven by the demand for high-quality, durable products in industries such as automotive, aerospace, and general machinery. As technology advances, mechanical presses are becoming more sophisticated, incorporating features like automation and digital controls to enhance productivity and safety. The global market for mechanical presses is expanding as industries seek to improve production efficiency and product quality. This growth is supported by the increasing adoption of advanced manufacturing technologies and the need for cost-effective production solutions. As a result, the mechanical presses market is poised for continued development, offering numerous opportunities for manufacturers and end-users alike.

Less than 2500KN, 2500KN-10000KN, More than 10000KN in the Global Mechanical Presses Market:

The Global Mechanical Presses Market can be categorized based on the force capacity of the presses, which is measured in kilonewtons (KN). The first category, less than 2500KN, represents smaller presses that are typically used for light to medium-duty applications. These presses are ideal for small-scale manufacturing operations or industries that require precision in shaping or cutting smaller components. They are often used in the production of small automotive parts, electronic components, and other precision-engineered products. The demand for these presses is driven by industries that prioritize precision and efficiency in their production processes. The second category, 2500KN-10000KN, includes medium-sized presses that are versatile and suitable for a wide range of applications. These presses are commonly used in industries such as automotive, aerospace, and general machinery, where they are employed to produce larger components or assemblies. The versatility of these presses makes them a popular choice for manufacturers looking to balance production capacity with cost-effectiveness. The third category, more than 10000KN, encompasses large presses designed for heavy-duty applications. These presses are used in industries that require significant force to shape or cut large, thick materials, such as shipbuilding, heavy machinery, and large-scale automotive manufacturing. The demand for these presses is driven by industries that require robust and durable equipment to handle demanding production tasks. As the global manufacturing landscape evolves, the demand for mechanical presses across these categories is expected to grow, driven by the need for efficient, high-capacity production solutions. Manufacturers are continually innovating to develop presses that offer enhanced performance, reliability, and safety features, catering to the diverse needs of industries worldwide.

Automotive industry, Ship Building industry, Aerospace industry, General Machine industry, Home appliances, Others in the Global Mechanical Presses Market:

Mechanical presses play a crucial role in various industries, providing the force needed to shape, cut, or mold materials into desired forms. In the automotive industry, mechanical presses are used extensively to produce a wide range of components, from body panels to engine parts. The precision and efficiency of these presses make them ideal for high-volume production, ensuring that automotive manufacturers can meet the demands of the market. In the shipbuilding industry, mechanical presses are used to shape large metal sheets and components that form the hulls and structures of ships. The ability to handle large, thick materials makes these presses indispensable in the construction of durable and robust vessels. In the aerospace industry, mechanical presses are used to produce critical components that require high precision and strength. The aerospace sector demands materials that can withstand extreme conditions, and mechanical presses provide the necessary force to shape these materials accurately. In the general machine industry, mechanical presses are used to manufacture a variety of machinery components, from gears to frames. The versatility of these presses allows manufacturers to produce components for different types of machinery, catering to a wide range of industrial needs. In the home appliances sector, mechanical presses are used to produce components for products such as refrigerators, washing machines, and ovens. The demand for high-quality, durable home appliances drives the need for efficient production processes, and mechanical presses provide the necessary capabilities to meet these demands. Other industries, such as electronics and construction, also rely on mechanical presses to produce components that require precision and durability. As industries continue to evolve, the usage of mechanical presses is expected to expand, driven by the need for efficient, high-quality production solutions.

Global Mechanical Presses Market Outlook:

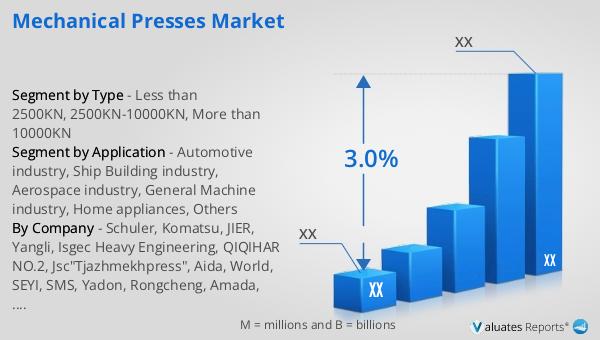

In 2024, the global market size for mechanical presses was valued at approximately US$ 9,567 million. This market is projected to grow, reaching an estimated value of around US$ 11,730 million by 2031, with a compound annual growth rate (CAGR) of 3.0% during the forecast period from 2025 to 2031. The market is characterized by a concentration of leading manufacturers, with the top five companies holding a combined market share of about 30%. Among the various product segments, presses with a capacity of less than 2500KN represent the largest share, accounting for approximately 65% of the market. This segment's dominance is attributed to the widespread use of smaller presses in industries that require precision and efficiency in their production processes. The growth of the mechanical presses market is driven by the increasing demand for high-quality, durable products across various industries, including automotive, aerospace, and general machinery. As manufacturers continue to innovate and develop advanced mechanical presses, the market is expected to offer numerous opportunities for growth and expansion. The focus on enhancing productivity, safety, and cost-effectiveness will further drive the adoption of mechanical presses in diverse industrial applications.

| Report Metric | Details |

| Report Name | Mechanical Presses Market |

| CAGR | 3.0% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Schuler, Komatsu, JIER, Yangli, Isgec Heavy Engineering, QIQIHAR NO.2, Jsc"Tjazhmekhpress", Aida, World, SEYI, SMS, Yadon, Rongcheng, Amada, Xuduan, Hitachi Zosen, Fagor Arrasate, Chin Fong |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |