What is Global Flow Wrap Machines Market?

The Global Flow Wrap Machines Market is a dynamic and essential segment of the packaging industry, focusing on machines designed to wrap products in a continuous roll of film. These machines are pivotal in ensuring that products are securely packaged, maintaining their quality and extending their shelf life. Flow wrap machines are versatile and can handle a wide range of products, from food items to pharmaceuticals, making them indispensable in various industries. The market for these machines is driven by the increasing demand for efficient packaging solutions that can cater to the growing consumer goods sector. As businesses strive to enhance their packaging processes, flow wrap machines offer a reliable solution that combines speed, efficiency, and precision. The global market is characterized by technological advancements, with manufacturers continually innovating to meet the evolving needs of their clients. This market is expected to grow as more industries recognize the benefits of flow wrap machines in improving packaging efficiency and product protection. The adaptability of these machines to different product types and sizes further fuels their demand, making them a crucial component in the global packaging landscape.

Horizontal, Vertical in the Global Flow Wrap Machines Market:

In the Global Flow Wrap Machines Market, horizontal and vertical machines play significant roles, each catering to specific packaging needs. Horizontal flow wrap machines are designed to wrap products that are typically uniform in shape and size, such as biscuits, chocolates, and other confectionery items. These machines operate by feeding the product horizontally into the machine, where it is wrapped in a film and sealed. The horizontal design is particularly advantageous for products that require a stable and consistent packaging process, ensuring that each item is securely wrapped without compromising its integrity. This type of machine is favored in industries where speed and efficiency are paramount, as it can handle high volumes of products with minimal downtime. On the other hand, vertical flow wrap machines are tailored for products that may not have a uniform shape or are more challenging to handle, such as loose items or products that need to be packaged in a standing position. These machines feed the product vertically, allowing gravity to assist in the packaging process. Vertical machines are often used for packaging snacks, cereals, and other items that require a more flexible approach. The versatility of vertical machines makes them ideal for industries that deal with a wide variety of product types and sizes. Both horizontal and vertical flow wrap machines are integral to the packaging industry, offering unique benefits that cater to different market needs. As the demand for efficient and reliable packaging solutions continues to grow, the importance of these machines in the global market cannot be overstated. Manufacturers are continually innovating to enhance the capabilities of both horizontal and vertical machines, ensuring they meet the ever-evolving demands of the packaging industry. The choice between horizontal and vertical machines often depends on the specific requirements of the product being packaged, with each type offering distinct advantages that can significantly impact the efficiency and effectiveness of the packaging process. As industries continue to expand and diversify, the role of horizontal and vertical flow wrap machines in meeting the diverse packaging needs of businesses worldwide remains crucial.

Food & Beverages, Pharmaceuticals, Other in the Global Flow Wrap Machines Market:

The Global Flow Wrap Machines Market finds extensive application across various sectors, including food and beverages, pharmaceuticals, and other industries. In the food and beverages sector, flow wrap machines are indispensable for packaging a wide range of products, from snacks and confectionery to fresh produce and ready-to-eat meals. These machines ensure that food products are securely wrapped, preserving their freshness and extending their shelf life. The ability to package products quickly and efficiently makes flow wrap machines a preferred choice for food manufacturers looking to meet the demands of a fast-paced market. In the pharmaceutical industry, flow wrap machines play a critical role in ensuring that medical products are packaged safely and hygienically. These machines are used to wrap items such as tablets, capsules, and medical devices, providing a protective barrier that safeguards against contamination and damage. The precision and reliability of flow wrap machines are essential in maintaining the integrity of pharmaceutical products, which is crucial for patient safety. Beyond food and pharmaceuticals, flow wrap machines are also used in various other industries, including cosmetics, electronics, and consumer goods. In these sectors, the machines are employed to package products ranging from beauty products and electronic components to household items and toys. The versatility of flow wrap machines allows them to adapt to different packaging requirements, making them a valuable asset for businesses looking to enhance their packaging processes. As industries continue to evolve and consumer expectations rise, the demand for efficient and reliable packaging solutions like flow wrap machines is expected to grow. The ability of these machines to cater to diverse packaging needs across multiple sectors underscores their importance in the global market.

Global Flow Wrap Machines Market Outlook:

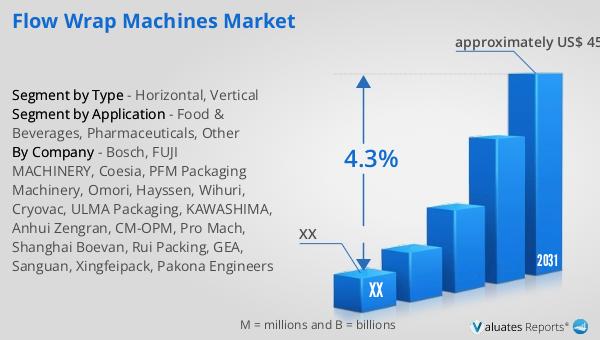

In 2024, the global market size for Flow Wrap Machines was valued at approximately US$ 3,367 million. Looking ahead, it is projected to grow significantly, reaching around US$ 4,502 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.3% during the forecast period from 2025 to 2031. The market is characterized by a concentration of key players, with the top five manufacturers holding a combined market share of about 20%. This indicates a competitive landscape where a few major companies dominate the market. In terms of product segmentation, vertical flow wrap machines represent the largest segment, accounting for approximately 70% of the market share. This dominance can be attributed to the versatility and efficiency of vertical machines in handling a wide range of products, making them a preferred choice for many industries. The significant market share held by vertical machines highlights their importance in the global flow wrap machines market, as they cater to diverse packaging needs across various sectors. As the market continues to evolve, the demand for innovative and efficient packaging solutions is expected to drive further growth, with vertical flow wrap machines playing a pivotal role in meeting these demands.

| Report Metric | Details |

| Report Name | Flow Wrap Machines Market |

| Forecasted market size in 2031 | approximately US$ 4502 million |

| CAGR | 4.3% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Bosch, FUJI MACHINERY, Coesia, PFM Packaging Machinery, Omori, Hayssen, Wihuri, Cryovac, ULMA Packaging, KAWASHIMA, Anhui Zengran, CM-OPM, Pro Mach, Shanghai Boevan, Rui Packing, GEA, Sanguan, Xingfeipack, Pakona Engineers |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |