What is Global Zika Virus Testing Market?

The Global Zika Virus Testing Market is a specialized segment within the broader healthcare diagnostics industry, focusing on the detection and management of the Zika virus. This market has gained significant attention due to the outbreaks of the Zika virus, which is primarily transmitted through the bite of an infected Aedes species mosquito. The virus can also be transmitted through sexual contact, blood transfusion, and from mother to child during pregnancy, leading to severe birth defects. The market encompasses various testing methods designed to identify the presence of the virus in individuals, thereby aiding in timely diagnosis and management. These tests are crucial for controlling the spread of the virus, especially in regions prone to outbreaks. The market is driven by the need for accurate and rapid testing solutions, advancements in diagnostic technologies, and increased awareness about the virus and its potential health impacts. As global travel and climate change continue to influence the spread of mosquito-borne diseases, the demand for effective Zika virus testing solutions is expected to remain significant. The market is characterized by a mix of established diagnostic companies and emerging players, all striving to develop innovative testing solutions to meet the growing demand.

Molecular Test, Serologic Test in the Global Zika Virus Testing Market:

Molecular tests and serologic tests are the two primary methods used in the Global Zika Virus Testing Market, each serving distinct purposes in the detection and management of the virus. Molecular tests, such as the Reverse Transcription Polymerase Chain Reaction (RT-PCR), are designed to detect the genetic material of the Zika virus. These tests are highly sensitive and can identify the virus in the early stages of infection, typically within the first week after the onset of symptoms. Molecular tests are considered the gold standard for Zika virus detection due to their accuracy and ability to provide definitive results. They are particularly useful in diagnosing acute infections and are often used in conjunction with serologic tests to confirm the presence of the virus. On the other hand, serologic tests are used to detect antibodies produced by the immune system in response to the Zika virus. These tests are valuable for identifying past infections and determining immunity levels in individuals. Serologic tests can detect Immunoglobulin M (IgM) and Immunoglobulin G (IgG) antibodies, which appear in the blood after the initial infection. While serologic tests are less effective in the early stages of infection, they play a crucial role in epidemiological studies and in assessing the spread of the virus within populations. Both molecular and serologic tests have their advantages and limitations. Molecular tests require sophisticated laboratory equipment and trained personnel, making them more expensive and less accessible in resource-limited settings. However, their high sensitivity and specificity make them indispensable for accurate diagnosis. Serologic tests, while more accessible and cost-effective, can sometimes produce cross-reactivity with other flaviviruses, such as dengue, leading to false-positive results. Despite these challenges, ongoing research and technological advancements are continually improving the accuracy and reliability of both testing methods. The choice between molecular and serologic tests often depends on the clinical context, the stage of infection, and the resources available. In many cases, a combination of both tests is used to provide a comprehensive diagnosis. As the Global Zika Virus Testing Market continues to evolve, the development of rapid, point-of-care testing solutions is becoming increasingly important. These innovations aim to provide accurate results in a shorter time frame, making them ideal for use in outbreak situations and remote areas. The integration of digital technologies and data analytics is also enhancing the efficiency and effectiveness of Zika virus testing, enabling better tracking and management of the disease. Overall, molecular and serologic tests are integral components of the Global Zika Virus Testing Market, each contributing to the timely and accurate diagnosis of the Zika virus.

Diagnostic Centers, Hospitals, Pathology Labs in the Global Zika Virus Testing Market:

The Global Zika Virus Testing Market plays a vital role in various healthcare settings, including diagnostic centers, hospitals, and pathology labs. Each of these settings utilizes Zika virus testing in unique ways to address the needs of patients and the broader community. Diagnostic centers are often the first point of contact for individuals seeking testing for the Zika virus. These centers are equipped with specialized equipment and trained personnel to conduct both molecular and serologic tests. Diagnostic centers focus on providing accurate and timely results, which are crucial for initiating appropriate treatment and preventing further transmission of the virus. They also play a key role in public health surveillance by collecting and analyzing data on Zika virus cases, which helps in understanding the spread and impact of the virus. Hospitals, on the other hand, integrate Zika virus testing into their broader healthcare services. In hospitals, testing is often part of a comprehensive diagnostic workup for patients presenting with symptoms consistent with Zika virus infection. Pregnant women, in particular, are a high-priority group for testing due to the risk of congenital Zika syndrome, which can lead to severe birth defects. Hospitals utilize both molecular and serologic tests to ensure accurate diagnosis and to guide clinical management. In addition to individual patient care, hospitals contribute to public health efforts by reporting confirmed cases to health authorities, thereby aiding in the monitoring and control of outbreaks. Pathology labs are essential for the detailed analysis and confirmation of Zika virus cases. These labs are equipped with advanced diagnostic technologies and staffed by skilled professionals who specialize in the detection and characterization of infectious diseases. Pathology labs often serve as reference centers, providing confirmatory testing for cases identified in other healthcare settings. They play a critical role in quality assurance, ensuring that testing methods are accurate and reliable. Pathology labs also contribute to research efforts aimed at improving testing methodologies and understanding the virus's behavior and impact. Across all these settings, the Global Zika Virus Testing Market is instrumental in supporting public health initiatives aimed at controlling the spread of the virus. By providing accurate and timely testing, these healthcare facilities help to identify and isolate cases, prevent transmission, and protect vulnerable populations. The integration of Zika virus testing into routine healthcare services also enhances the overall capacity of health systems to respond to emerging infectious diseases. As the market continues to evolve, the development of innovative testing solutions and the expansion of testing capabilities in resource-limited settings remain key priorities.

Global Zika Virus Testing Market Outlook:

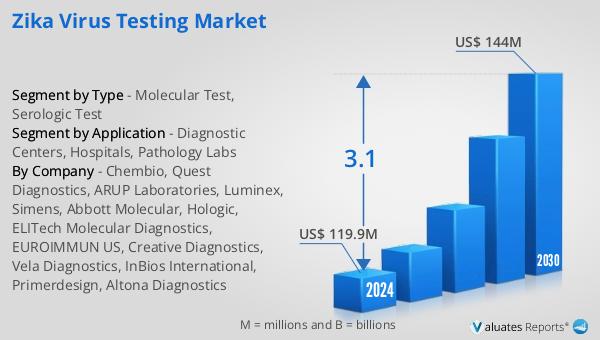

In 2024, the global market size for Zika Virus Testing was valued at approximately $123 million, with projections indicating it could reach around $152 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.1% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold about 55% of the market share. North America emerges as the largest regional market, accounting for roughly 45% of the global share, followed by Europe, which holds about 30%. In terms of product segmentation, the Molecular Test segment stands out as the largest, commanding approximately 90% of the market share. This dominance is attributed to the high accuracy and reliability of molecular tests in detecting the Zika virus, making them the preferred choice for healthcare providers. The market dynamics are influenced by various factors, including advancements in diagnostic technologies, increased awareness about the virus, and the need for rapid and accurate testing solutions. As the market continues to grow, the focus remains on developing innovative testing methods that can enhance the efficiency and effectiveness of Zika virus detection, ultimately contributing to better disease management and control.

| Report Metric | Details |

| Report Name | Zika Virus Testing Market |

| CAGR | 3.1% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Chembio, Quest Diagnostics, ARUP Laboratories, Luminex, Simens, Abbott Molecular, Hologic, ELITech Molecular Diagnostics, EUROIMMUN US, Creative Diagnostics, Vela Diagnostics, InBios International, Primerdesign, Altona Diagnostics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |