What is Global BCG Vaccine Market?

The Global BCG Vaccine Market refers to the worldwide industry focused on the production, distribution, and utilization of the Bacillus Calmette-Guérin (BCG) vaccine. This vaccine is primarily used to prevent tuberculosis (TB), a serious infectious disease that mainly affects the lungs but can also impact other parts of the body. The BCG vaccine is one of the oldest vaccines still in use today, having been developed in the early 20th century. It is particularly important in countries where TB is prevalent, as it helps reduce the risk of severe forms of the disease in children. The market for BCG vaccines is influenced by factors such as the prevalence of TB, government vaccination programs, and the availability of alternative TB prevention methods. Additionally, the BCG vaccine has been explored for its potential benefits in other areas, such as bladder cancer treatment and boosting general immune responses, which can further impact market dynamics. The global market for BCG vaccines is characterized by a mix of public and private sector involvement, with organizations like the World Health Organization (WHO) and UNICEF playing significant roles in vaccine distribution and advocacy.

Immune Vaccine, Therapy Vaccine in the Global BCG Vaccine Market:

The BCG vaccine, originally developed to combat tuberculosis, has found applications beyond its initial purpose, particularly in the realm of immune and therapy vaccines. Immune vaccines are designed to enhance the body's immune response to specific pathogens or diseases. The BCG vaccine, in this context, is being studied for its potential to boost the immune system's ability to fight off various infections and even some non-infectious diseases. Research has suggested that the BCG vaccine may have non-specific effects on the immune system, potentially providing protection against a range of pathogens beyond Mycobacterium tuberculosis, the bacterium that causes TB. This has led to interest in using the BCG vaccine as a tool to enhance general immunity, particularly in populations at high risk of infectious diseases. In addition to its role as an immune vaccine, the BCG vaccine is also being explored as a therapy vaccine, particularly in the treatment of bladder cancer. In this context, the BCG vaccine is used as an intravesical therapy, where it is directly instilled into the bladder to provoke an immune response that targets cancer cells. This form of treatment has been shown to be effective in reducing the recurrence of superficial bladder cancer and is considered a standard treatment option for this condition. The mechanism by which the BCG vaccine exerts its therapeutic effects in bladder cancer is not fully understood, but it is believed to involve the activation of the immune system, leading to the destruction of cancer cells. The dual role of the BCG vaccine as both an immune and therapy vaccine highlights its versatility and potential in addressing a range of health challenges. The ongoing research into the broader applications of the BCG vaccine underscores the importance of continued investment in vaccine development and innovation. As the global health landscape evolves, the BCG vaccine's role may expand further, offering new opportunities for disease prevention and treatment. The exploration of the BCG vaccine's potential in immune and therapy applications is a testament to the dynamic nature of vaccine research and the continuous quest to harness the power of the immune system in combating disease. This ongoing research and development effort is crucial for addressing current and future health challenges, particularly in the face of emerging infectious diseases and the growing burden of non-communicable diseases. The BCG vaccine's potential to enhance immune responses and serve as a therapeutic agent in cancer treatment exemplifies the innovative approaches being pursued in the field of vaccinology. As scientists continue to unravel the complexities of the immune system and its interactions with vaccines, the BCG vaccine may serve as a valuable tool in the global effort to improve health outcomes and reduce the burden of disease. The exploration of the BCG vaccine's broader applications also highlights the importance of collaboration between researchers, healthcare providers, and policymakers in advancing vaccine research and ensuring access to life-saving interventions. The potential of the BCG vaccine to contribute to improved health outcomes underscores the need for continued investment in vaccine research and development, as well as the importance of global cooperation in addressing the world's most pressing health challenges.

Self-Procurement, UNICEF, Other in the Global BCG Vaccine Market:

The Global BCG Vaccine Market plays a crucial role in various areas, including self-procurement, UNICEF, and other distribution channels. Self-procurement refers to the process by which individual countries or regions purchase vaccines directly from manufacturers or suppliers. This approach allows countries to tailor their vaccine procurement strategies to their specific needs and priorities. In the context of the BCG vaccine, self-procurement is particularly important for countries with high TB prevalence, as it enables them to secure an adequate supply of vaccines to meet their public health goals. Countries that engage in self-procurement often have established healthcare infrastructure and resources to manage the logistics of vaccine distribution and administration. UNICEF, the United Nations Children's Fund, is another key player in the distribution of BCG vaccines. As part of its mission to improve the health and well-being of children worldwide, UNICEF works to ensure that vaccines, including the BCG vaccine, are accessible to children in low- and middle-income countries. UNICEF collaborates with governments, non-governmental organizations, and other partners to facilitate the procurement and distribution of vaccines, often at reduced costs, to reach vulnerable populations. Through its efforts, UNICEF helps to bridge the gap in vaccine access and equity, ensuring that children in resource-limited settings receive the protection they need against TB and other preventable diseases. In addition to self-procurement and UNICEF, other distribution channels also play a role in the Global BCG Vaccine Market. These channels may include international organizations, non-governmental organizations, and private sector entities that work to improve vaccine access and distribution. For example, the World Health Organization (WHO) provides guidance and support to countries in developing and implementing vaccination programs, including those involving the BCG vaccine. Private sector companies may also be involved in the production and distribution of BCG vaccines, contributing to the overall supply chain and availability of vaccines in the market. The collaboration between public and private sector entities is essential for ensuring a stable and reliable supply of BCG vaccines, particularly in regions with high demand. The Global BCG Vaccine Market's diverse distribution channels reflect the complexity and importance of ensuring vaccine access and equity worldwide. By leveraging the strengths and resources of various stakeholders, the market can better address the challenges of TB prevention and control, ultimately contributing to improved health outcomes for populations at risk. The continued collaboration and innovation in vaccine distribution are vital for overcoming barriers to access and ensuring that all individuals, regardless of their geographic location or socioeconomic status, have the opportunity to benefit from life-saving vaccines like the BCG vaccine.

Global BCG Vaccine Market Outlook:

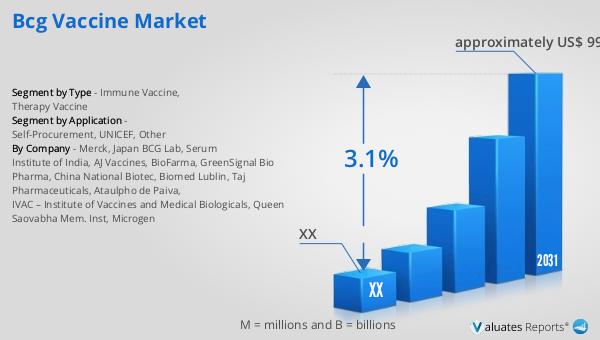

In the year 2024, the global market size for the BCG Vaccine was valued at approximately US$ 80.4 million. This figure represents the total worth of the market, encompassing all aspects of production, distribution, and sales of the BCG vaccine worldwide. Looking ahead, the market is projected to grow, reaching an estimated value of around US$ 99 million by the year 2031. This anticipated growth reflects a compound annual growth rate (CAGR) of 3.1% during the forecast period from 2025 to 2031. The projected increase in market size indicates a steady demand for the BCG vaccine, driven by factors such as the ongoing need for TB prevention, the exploration of new applications for the vaccine, and the expansion of vaccination programs in various regions. The growth of the BCG Vaccine Market also underscores the importance of continued investment in vaccine research and development, as well as the need for effective distribution strategies to ensure that vaccines reach those who need them most. As the market evolves, stakeholders across the public and private sectors will play a critical role in supporting the expansion and accessibility of the BCG vaccine, ultimately contributing to improved global health outcomes. The projected growth of the BCG Vaccine Market highlights the dynamic nature of the vaccine industry and the ongoing efforts to address public health challenges through innovative solutions. By understanding the market trends and drivers, stakeholders can better navigate the complexities of the vaccine landscape and work towards achieving the shared goal of reducing the burden of TB and other preventable diseases. The anticipated growth in the BCG Vaccine Market is a testament to the resilience and adaptability of the global health community in the face of evolving health needs and challenges.

| Report Metric | Details |

| Report Name | BCG Vaccine Market |

| Forecasted market size in 2031 | approximately US$ 99 million |

| CAGR | 3.1% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Merck, Japan BCG Lab, Serum Institute of India, AJ Vaccines, BioFarma, GreenSignal Bio Pharma, China National Biotec, Biomed Lublin, Taj Pharmaceuticals, Ataulpho de Paiva, IVAC – Institute of Vaccines and Medical Biologicals, Queen Saovabha Mem. Inst, Microgen |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |