What is Global Hydroxyapatite Ceramics Market?

The Global Hydroxyapatite Ceramics Market is a specialized segment within the broader ceramics industry, focusing on the production and application of hydroxyapatite ceramics. Hydroxyapatite is a naturally occurring mineral form of calcium apatite, which is a major component of bone and teeth. This market is driven by the increasing demand for biocompatible materials in medical applications, particularly in orthopedics and dentistry. Hydroxyapatite ceramics are valued for their excellent biocompatibility, bioactivity, and osteoconductivity, making them ideal for use in bone grafts, dental implants, and other medical devices. The market is characterized by a growing interest in advanced materials that can enhance the performance and longevity of medical implants. As healthcare systems worldwide continue to evolve, there is a rising need for materials that can integrate seamlessly with human tissue, reduce recovery times, and improve patient outcomes. This demand is further fueled by an aging global population and the increasing prevalence of bone-related diseases and dental issues. The market is also witnessing innovations in manufacturing processes and material formulations, aimed at improving the mechanical properties and functionality of hydroxyapatite ceramics.

Porous Hydroxyapatite Ceramics, Dense Hydroxyapatite Ceramics in the Global Hydroxyapatite Ceramics Market:

Porous hydroxyapatite ceramics and dense hydroxyapatite ceramics are two primary types of materials within the Global Hydroxyapatite Ceramics Market, each with distinct characteristics and applications. Porous hydroxyapatite ceramics are designed with a network of interconnected pores, which mimic the natural structure of bone. This porosity is crucial for facilitating the growth of new bone tissue and the integration of the implant with the surrounding bone. The porous structure allows for the infiltration of bodily fluids and cells, promoting osteogenesis and vascularization. These ceramics are often used in bone grafts and scaffolds, where the goal is to support the regeneration of bone tissue. The porosity can be controlled during the manufacturing process to achieve the desired balance between mechanical strength and biological functionality. On the other hand, dense hydroxyapatite ceramics are characterized by their solid, non-porous structure. These ceramics are typically used in applications where high mechanical strength and wear resistance are required, such as in dental implants and load-bearing orthopedic implants. The dense structure provides durability and stability, making them suitable for long-term implantation. The manufacturing of dense hydroxyapatite ceramics involves processes that ensure the material's integrity and performance under stress. Both porous and dense hydroxyapatite ceramics are subject to ongoing research and development efforts aimed at enhancing their properties and expanding their applications. Innovations in material science and engineering are leading to the development of hybrid materials that combine the benefits of both porous and dense structures. For instance, some advanced ceramics feature a dense core for strength and a porous outer layer for biological integration. This dual-structure approach aims to optimize the performance of implants by addressing both mechanical and biological requirements. The choice between porous and dense hydroxyapatite ceramics depends on the specific application and the desired outcomes. In orthopedic applications, the focus is often on achieving a balance between strength and biological integration, while in dental applications, aesthetics and durability may take precedence. The versatility of hydroxyapatite ceramics makes them a valuable material in the medical field, with ongoing research exploring new ways to enhance their performance and expand their use. As the Global Hydroxyapatite Ceramics Market continues to grow, manufacturers are investing in advanced technologies and processes to meet the evolving needs of the healthcare industry. This includes the development of customized solutions tailored to specific patient needs and the exploration of new applications beyond traditional medical uses. The market is also influenced by regulatory considerations, as manufacturers must ensure that their products meet stringent safety and efficacy standards. Overall, the Global Hydroxyapatite Ceramics Market is a dynamic and evolving sector, driven by the demand for innovative materials that can improve patient outcomes and support the advancement of medical technology.

Orthopaedic, Dental, Biochemical Research, Others in the Global Hydroxyapatite Ceramics Market:

The Global Hydroxyapatite Ceramics Market finds extensive usage across various fields, including orthopedics, dental, biochemical research, and other areas. In orthopedics, hydroxyapatite ceramics are primarily used for bone grafts and implants. Their biocompatibility and osteoconductivity make them ideal for promoting bone growth and integration with existing bone tissue. These ceramics are often used in joint replacements, spinal surgeries, and fracture repairs, where they help in the regeneration of bone and provide structural support. The ability of hydroxyapatite to bond with natural bone tissue reduces the risk of implant rejection and enhances the healing process, making it a preferred choice for orthopedic surgeons. In the dental field, hydroxyapatite ceramics are used in dental implants, coatings, and fillers. Their natural resemblance to tooth enamel and bone makes them suitable for dental restorations and repairs. Dental implants made from hydroxyapatite provide a stable and durable solution for tooth replacement, offering both aesthetic and functional benefits. The ceramics' ability to integrate with jawbone tissue ensures a secure fit and long-lasting results. Additionally, hydroxyapatite is used in toothpaste and other oral care products for its remineralizing properties, helping to strengthen tooth enamel and prevent cavities. In biochemical research, hydroxyapatite ceramics serve as a valuable tool for studying bone biology and developing new medical treatments. Researchers use these ceramics to create models that mimic the natural bone environment, allowing for the study of cell behavior, drug delivery, and tissue engineering. The ceramics' ability to support cell growth and differentiation makes them an essential component in the development of new therapies for bone-related diseases and conditions. Beyond orthopedics, dental, and research applications, hydroxyapatite ceramics are also used in other areas such as cosmetics and environmental protection. In cosmetics, hydroxyapatite is used in skincare products for its gentle exfoliating properties and ability to enhance skin texture. In environmental applications, hydroxyapatite is explored for its potential in water purification and heavy metal removal, leveraging its adsorption capabilities. The versatility of hydroxyapatite ceramics and their wide range of applications highlight their importance in various industries. As the Global Hydroxyapatite Ceramics Market continues to expand, new uses and innovations are likely to emerge, driven by ongoing research and technological advancements. The market's growth is supported by the increasing demand for biocompatible materials that can improve patient outcomes and address the challenges of modern healthcare.

Global Hydroxyapatite Ceramics Market Outlook:

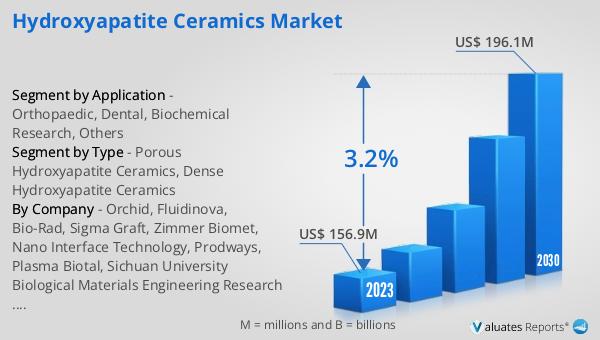

In 2024, the global market size for Hydroxyapatite Ceramics was valued at approximately US$ 167 million, with projections indicating it could reach around US$ 208 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.2% during the forecast period from 2025 to 2031. North America holds the largest share of the Hydroxyapatite Ceramics market, accounting for over 60% of the total market. Europe follows with a 25% market share. The industry is dominated by key players such as Zimmer Biomet, Bio-Rad, and Orchid, who collectively hold nearly 70% of the market share. These companies are at the forefront of innovation and development within the market, driving advancements in hydroxyapatite ceramics technology and applications. The market's growth is fueled by the increasing demand for biocompatible materials in medical applications, particularly in orthopedics and dentistry. As healthcare systems continue to evolve, there is a rising need for materials that can integrate seamlessly with human tissue, reduce recovery times, and improve patient outcomes. The market is also witnessing innovations in manufacturing processes and material formulations, aimed at improving the mechanical properties and functionality of hydroxyapatite ceramics. Overall, the Global Hydroxyapatite Ceramics Market is poised for steady growth, driven by the demand for advanced materials that can enhance the performance and longevity of medical implants.

| Report Metric | Details |

| Report Name | Hydroxyapatite Ceramics Market |

| Forecasted market size in 2031 | approximately US$ 208 million |

| CAGR | 3.2% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Orchid, Fluidinova, Bio-Rad, Sigma Graft, Zimmer Biomet, Nano Interface Technology, Prodways, Plasma Biotal, Sichuan University Biological Materials Engineering Research Center, Shanghai Bio-lu Biomaterials, CAM Bioceramics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |