What is Global Swine Vaccines Market?

The Global Swine Vaccines Market is a crucial segment of the animal healthcare industry, focusing on the development and distribution of vaccines specifically designed for pigs. These vaccines play a vital role in preventing and controlling diseases that can significantly impact swine populations, thereby ensuring the health and productivity of these animals. The market encompasses a wide range of vaccines targeting various diseases, including Classical Swine Fever (CSF), Foot and Mouth Disease (FMD), Porcine Circovirus, and Porcine Reproductive and Respiratory Syndrome (PRRS), among others. The demand for swine vaccines is driven by the need to maintain animal health, improve meat quality, and enhance the overall efficiency of swine production. As the global population continues to grow, the demand for pork and pork products is also on the rise, further fueling the need for effective vaccination programs. The market is characterized by continuous research and development efforts aimed at improving vaccine efficacy and safety, as well as expanding the range of diseases that can be effectively managed through vaccination. This dynamic market is influenced by various factors, including advancements in biotechnology, regulatory frameworks, and the increasing awareness of animal health issues among farmers and producers.

CSF Vaccines, FMD Vaccines, Porcine Circovirus Vaccines, PRRS Vaccines, Others in the Global Swine Vaccines Market:

CSF Vaccines, or Classical Swine Fever Vaccines, are essential in the Global Swine Vaccines Market as they target a highly contagious viral disease that affects pigs. Classical Swine Fever, also known as hog cholera, can lead to significant economic losses due to high mortality rates and decreased productivity in infected herds. CSF vaccines are designed to provide immunity against the virus, thereby preventing outbreaks and ensuring the health of swine populations. These vaccines are typically administered to piglets and breeding sows to establish herd immunity. FMD Vaccines, or Foot and Mouth Disease Vaccines, are another critical component of the swine vaccines market. Foot and Mouth Disease is a severe, highly contagious viral disease that affects cloven-hoofed animals, including pigs. The disease can spread rapidly, causing significant economic losses due to trade restrictions and decreased productivity. FMD vaccines are used to control and prevent outbreaks, thereby safeguarding the health of swine populations and ensuring the stability of the pork industry. Porcine Circovirus Vaccines target the Porcine Circovirus, a virus that can cause a range of diseases in pigs, including Postweaning Multisystemic Wasting Syndrome (PMWS) and Porcine Dermatitis and Nephropathy Syndrome (PDNS). These diseases can lead to significant economic losses due to decreased growth rates, increased mortality, and reduced reproductive performance. Porcine Circovirus Vaccines are designed to provide immunity against the virus, thereby preventing these diseases and ensuring the health and productivity of swine populations. PRRS Vaccines, or Porcine Reproductive and Respiratory Syndrome Vaccines, are crucial in the swine vaccines market as they target a viral disease that affects the reproductive and respiratory systems of pigs. PRRS can lead to significant economic losses due to decreased reproductive performance, increased mortality, and reduced growth rates. PRRS vaccines are designed to provide immunity against the virus, thereby preventing outbreaks and ensuring the health and productivity of swine populations. Other vaccines in the Global Swine Vaccines Market target a range of diseases, including Swine Influenza, Mycoplasma Hyopneumoniae, and Erysipelas. These vaccines are essential in maintaining the health and productivity of swine populations, thereby ensuring the stability of the pork industry. The development and distribution of these vaccines are driven by continuous research and development efforts aimed at improving vaccine efficacy and safety, as well as expanding the range of diseases that can be effectively managed through vaccination. The Global Swine Vaccines Market is characterized by a diverse range of vaccines targeting various diseases, each playing a crucial role in maintaining the health and productivity of swine populations.

Government Tender, Market Sales in the Global Swine Vaccines Market:

The usage of the Global Swine Vaccines Market is significant in areas such as government tenders and market sales. Government tenders play a crucial role in the distribution and administration of swine vaccines, as governments often procure vaccines in bulk to ensure the health and productivity of swine populations within their jurisdictions. These tenders are typically awarded to manufacturers and suppliers who meet specific criteria, including vaccine efficacy, safety, and cost-effectiveness. Government tenders are essential in ensuring the widespread availability of vaccines, particularly in regions where swine farming is a significant economic activity. By procuring vaccines through tenders, governments can ensure that farmers and producers have access to the necessary vaccines to maintain the health of their swine populations, thereby safeguarding the stability of the pork industry. Market sales, on the other hand, refer to the distribution and sale of swine vaccines through various channels, including veterinary clinics, agricultural supply stores, and online platforms. Market sales are driven by the demand for vaccines among farmers and producers who seek to maintain the health and productivity of their swine populations. The demand for swine vaccines is influenced by various factors, including the prevalence of diseases, the size of swine populations, and the level of awareness among farmers and producers regarding the importance of vaccination. Market sales are also influenced by the availability of vaccines, as well as the pricing and marketing strategies employed by manufacturers and suppliers. The Global Swine Vaccines Market is characterized by a competitive landscape, with numerous manufacturers and suppliers vying for market share. This competition drives innovation and research and development efforts aimed at improving vaccine efficacy and safety, as well as expanding the range of diseases that can be effectively managed through vaccination. The usage of the Global Swine Vaccines Market in government tenders and market sales is essential in ensuring the health and productivity of swine populations, thereby safeguarding the stability of the pork industry.

Global Swine Vaccines Market Outlook:

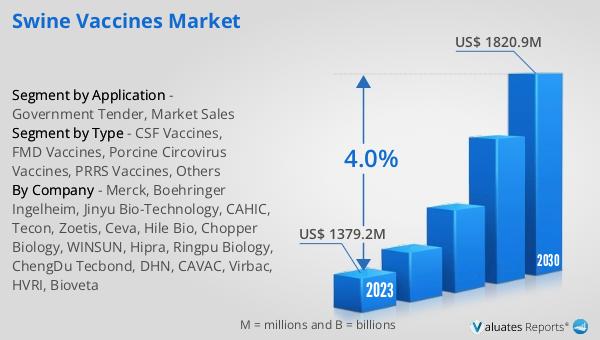

In 2024, the global market size of Swine Vaccines was valued at approximately US$ 1491 million, with projections indicating it could reach around US$ 1954 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.0% during the forecast period from 2025 to 2031. China stands out as the largest region for Swine Vaccines, holding a market share exceeding 40%, followed by Europe and North America. The market is dominated by a few key players, with Merck, Boehringer Ingelheim, Jinyu BioTechnology, CAHIC, and Tecon being the top five manufacturers. Together, these companies account for more than 55% of the total market share. This concentration of market power among a few major players highlights the competitive nature of the industry and the importance of innovation and strategic partnerships in maintaining and expanding market presence. The growth of the Swine Vaccines Market is driven by factors such as increasing demand for pork and pork products, advancements in vaccine technology, and the need to control and prevent swine diseases. As the market continues to evolve, manufacturers are likely to focus on developing new and improved vaccines, expanding their product portfolios, and exploring new markets to sustain growth and maintain their competitive edge.

| Report Metric | Details |

| Report Name | Swine Vaccines Market |

| CAGR | 4.0% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Merck, Boehringer Ingelheim, Jinyu Bio-Technology, CAHIC, Tecon, Zoetis, Ceva, Hile Bio, Chopper Biology, WINSUN, Hipra, Ringpu Biology, ChengDu Tecbond, DHN, CAVAC, Virbac, HVRI, Bioveta |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |