What is Global Helicobacter Pylori Testing Market?

The Global Helicobacter Pylori Testing Market is a specialized segment within the broader medical diagnostics industry, focusing on the detection and management of Helicobacter pylori infections. Helicobacter pylori is a type of bacteria that infects the stomach lining and is known to cause various gastrointestinal issues, including peptic ulcers and even stomach cancer if left untreated. The market for testing this bacterium is driven by the increasing prevalence of gastrointestinal disorders, growing awareness about the health implications of H. pylori infections, and advancements in diagnostic technologies. Various testing methods are employed, ranging from non-invasive breath and stool tests to invasive endoscopic procedures. The market is characterized by a mix of established players and emerging companies, all striving to offer more accurate, faster, and cost-effective testing solutions. As healthcare systems worldwide emphasize early detection and preventive care, the demand for H. pylori testing is expected to grow, making it a critical area of focus for healthcare providers and diagnostic companies alike. The market's growth is also supported by increasing healthcare expenditure and the rising adoption of advanced diagnostic tools in emerging economies.

With Endoscopy, Without Endoscopy in the Global Helicobacter Pylori Testing Market:

In the Global Helicobacter Pylori Testing Market, testing methods are broadly categorized into two types: with endoscopy and without endoscopy. Endoscopy-based testing involves the use of an endoscope, a flexible tube with a camera, to visually examine the stomach lining and obtain tissue samples for biopsy. This method is highly accurate and allows for direct observation of the stomach's condition, making it a preferred choice for diagnosing severe cases or when other tests yield inconclusive results. However, endoscopy is invasive, requires specialized equipment and trained personnel, and is generally more expensive than non-invasive methods. On the other hand, non-endoscopic testing methods include urea breath tests, stool antigen tests, and blood antibody tests. These methods are less invasive, more convenient, and often more cost-effective, making them suitable for routine screening and initial diagnosis. The urea breath test, for instance, is highly accurate and involves the patient ingesting a urea solution labeled with a carbon isotope. If H. pylori is present, the bacteria will metabolize the urea, releasing carbon dioxide that can be detected in the patient's breath. Stool antigen tests detect the presence of H. pylori antigens in a patient's feces, providing a direct indication of infection. Blood antibody tests, while useful for initial screening, are less reliable for confirming active infections as they detect antibodies that may persist long after the bacteria have been eradicated. The choice between endoscopic and non-endoscopic methods often depends on the patient's symptoms, medical history, and the healthcare provider's preference. In many cases, non-invasive tests are used for initial screening, with endoscopy reserved for cases where more detailed examination is necessary. The availability of these diverse testing options allows healthcare providers to tailor their diagnostic approach to each patient's needs, improving the overall effectiveness of H. pylori management. As technology advances, the accuracy and convenience of both endoscopic and non-endoscopic tests continue to improve, further enhancing their role in the global market.

Physical Examination Center, Hospitals, Others in the Global Helicobacter Pylori Testing Market:

The usage of the Global Helicobacter Pylori Testing Market spans various healthcare settings, including physical examination centers, hospitals, and other medical facilities. In physical examination centers, H. pylori testing is often part of routine health check-ups, especially in regions with a high prevalence of the infection. These centers typically use non-invasive testing methods, such as urea breath tests or stool antigen tests, due to their convenience and quick turnaround times. The ability to detect H. pylori infections early during routine examinations allows for timely intervention, reducing the risk of complications such as ulcers or gastric cancer. In hospitals, H. pylori testing plays a crucial role in diagnosing and managing patients with gastrointestinal symptoms. Hospitals are equipped to perform both non-invasive and invasive tests, including endoscopy, providing comprehensive diagnostic services. For patients presenting with severe symptoms or those who have not responded to initial treatment, endoscopic examination and biopsy may be necessary to confirm the presence of H. pylori and assess the extent of gastric damage. Hospitals also serve as referral centers for complex cases, where specialized testing and treatment are required. Beyond physical examination centers and hospitals, H. pylori testing is utilized in various other healthcare settings, including clinics, research institutions, and public health programs. Clinics often provide testing as part of their outpatient services, catering to patients seeking diagnosis and treatment for gastrointestinal issues. Research institutions may use H. pylori testing in clinical studies aimed at understanding the bacterium's role in gastric diseases and developing new treatment strategies. Public health programs, particularly in regions with high infection rates, may incorporate H. pylori testing as part of broader initiatives to improve population health and reduce the burden of gastric diseases. The widespread use of H. pylori testing across these diverse settings underscores its importance in modern healthcare, facilitating early detection, effective treatment, and improved patient outcomes.

Global Helicobacter Pylori Testing Market Outlook:

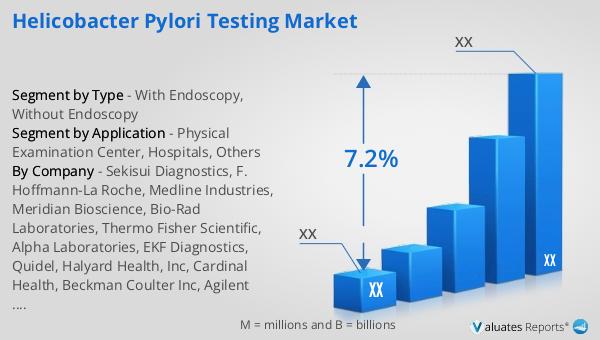

In 2024, the global market size for Helicobacter Pylori Testing was valued at approximately US$ 794 million, with projections indicating it could reach around US$ 1,284 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 7.2% during the forecast period from 2025 to 2031. The Asia-Pacific region holds the largest share of the Helicobacter Pylori Testing market, accounting for about 30%, followed by Europe and North America. Key manufacturers in this industry include Sekisui Diagnostics, F. Hoffmann-La Roche, Medline Industries, Meridian Bioscience, and Bio-Rad Laboratories. Despite the presence of these major players, the top 10 companies collectively hold less than 25% of the market share, indicating a competitive landscape with opportunities for new entrants and innovation. The market's growth is driven by factors such as increasing awareness of H. pylori infections, advancements in diagnostic technologies, and rising healthcare expenditures. As the demand for accurate and efficient testing solutions continues to rise, companies are focusing on developing innovative products and expanding their market presence. The competitive nature of the market encourages continuous improvement and adaptation, ensuring that healthcare providers have access to the best possible diagnostic tools for managing H. pylori infections.

| Report Metric | Details |

| Report Name | Helicobacter Pylori Testing Market |

| CAGR | 7.2% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Sekisui Diagnostics, F. Hoffmann-La Roche, Medline Industries, Meridian Bioscience, Bio-Rad Laboratories, Thermo Fisher Scientific, Alpha Laboratories, EKF Diagnostics, Quidel, Halyard Health, Inc, Cardinal Health, Beckman Coulter Inc, Agilent Technologies, Coris BioConcept |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |