What is Global Shunt Resistor Market?

The Global Shunt Resistor Market is a crucial segment within the electronics industry, focusing on devices that help measure electrical current. Shunt resistors are precision components used to create a low-resistance path for current to flow, allowing for accurate current measurement by measuring the voltage drop across the resistor. These resistors are essential in various applications, including automotive, industrial, and consumer electronics, where precise current measurement is critical for performance and safety. The market for shunt resistors is driven by the increasing demand for efficient energy management and the growing adoption of electric vehicles, which require precise current monitoring for battery management systems. Additionally, advancements in technology have led to the development of more accurate and reliable shunt resistors, further fueling market growth. The global market is characterized by a diverse range of products catering to different current ratings and applications, with manufacturers focusing on innovation and quality to meet the evolving needs of end-users. As industries continue to prioritize energy efficiency and precision in electrical systems, the demand for shunt resistors is expected to remain strong, supporting the market's steady growth.

Below 100A, 100 to 400A, 400 to 750A, 750 to 1000A in the Global Shunt Resistor Market:

In the Global Shunt Resistor Market, products are categorized based on their current rating, which determines their suitability for various applications. The "Below 100A" category includes shunt resistors designed for low-current applications, often found in consumer electronics and small-scale industrial equipment. These resistors are crucial for devices that require precise current measurement without handling high power levels. The "100 to 400A" segment caters to medium-current applications, such as larger industrial machinery and some automotive systems. These resistors offer a balance between size and performance, making them ideal for applications where space is limited but accurate current measurement is necessary. The "400 to 750A" category represents the largest segment in terms of product rated current, as it encompasses a wide range of industrial and automotive applications. These shunt resistors are designed to handle higher power levels, making them suitable for heavy-duty equipment and electric vehicles, where precise current monitoring is essential for safety and efficiency. Finally, the "750 to 1000A" segment includes shunt resistors for high-current applications, often used in large-scale industrial systems and advanced automotive technologies. These resistors are built to withstand significant power loads while maintaining accuracy and reliability, ensuring optimal performance in demanding environments. Each of these categories plays a vital role in the Global Shunt Resistor Market, catering to the diverse needs of industries that rely on precise current measurement for their operations. As technology continues to advance, the demand for shunt resistors across these categories is expected to grow, driven by the increasing complexity and power requirements of modern electronic systems.

Automotive, Ammeter, Communication, Consumer Electronics, Others in the Global Shunt Resistor Market:

The Global Shunt Resistor Market finds extensive usage across various sectors, each with unique requirements for current measurement and management. In the automotive industry, shunt resistors are integral to the operation of electric and hybrid vehicles, where they are used in battery management systems to monitor current flow and ensure efficient energy use. Accurate current measurement is crucial for optimizing battery performance and extending the lifespan of electric vehicles, making shunt resistors a key component in automotive applications. In ammeters, shunt resistors are used to measure electrical current by creating a known voltage drop, which is then used to calculate the current flowing through the circuit. This application is essential for both industrial and consumer-grade ammeters, where precision and reliability are paramount. In the communication sector, shunt resistors are used in various devices to manage power distribution and ensure stable operation. As communication technologies continue to evolve, the demand for precise current measurement and management solutions is expected to increase, further driving the need for shunt resistors. In consumer electronics, shunt resistors are used in a wide range of devices, from smartphones to home appliances, where they help manage power consumption and improve energy efficiency. The growing emphasis on energy-efficient consumer electronics is expected to boost the demand for shunt resistors in this sector. Additionally, shunt resistors are used in various other applications, including renewable energy systems and industrial automation, where they play a critical role in ensuring accurate current measurement and efficient power management. As industries continue to prioritize precision and efficiency in their operations, the Global Shunt Resistor Market is poised for sustained growth, driven by the diverse applications and increasing demand for reliable current measurement solutions.

Global Shunt Resistor Market Outlook:

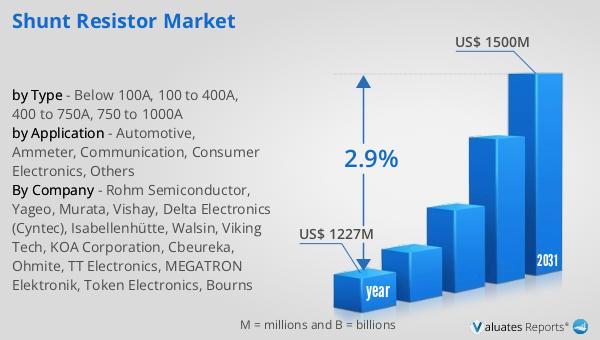

The global market for shunt resistors was valued at $1,227 million in 2024 and is anticipated to expand to a revised size of $1,500 million by 2031, reflecting a compound annual growth rate (CAGR) of 2.9% over the forecast period. The top five manufacturers globally hold a significant share, exceeding 53% of the market. China stands out as the largest producer of shunt resistors, contributing over 52% of the global production. When examining product rated current, the 400 to 750A segment emerges as the largest, capturing over 26% of the market share. In terms of application, the automotive sector is the leading segment, also holding a share of over 26%. This data underscores the importance of shunt resistors in various high-demand applications, particularly in automotive and industrial sectors, where precise current measurement is crucial for performance and safety. The market's steady growth is driven by the increasing demand for efficient energy management and the adoption of advanced technologies across industries. As manufacturers continue to innovate and improve the quality of shunt resistors, the market is expected to maintain its upward trajectory, supported by the growing need for reliable current measurement solutions in diverse applications.

| Report Metric | Details |

| Report Name | Shunt Resistor Market |

| Accounted market size in year | US$ 1227 million |

| Forecasted market size in 2031 | US$ 1500 million |

| CAGR | 2.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Rohm Semiconductor, Yageo, Murata, Vishay, Delta Electronics (Cyntec), Isabellenhütte, Walsin, Viking Tech, KOA Corporation, Cbeureka, Ohmite, TT Electronics, MEGATRON Elektronik, Token Electronics, Bourns |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |