What is Global Reflow Soldering Oven Market?

The Global Reflow Soldering Oven Market is a specialized segment within the electronics manufacturing industry, focusing on the equipment used for soldering electronic components onto printed circuit boards (PCBs). Reflow soldering ovens are essential in the assembly of electronic devices, as they provide the controlled heat necessary to melt solder paste and create reliable electrical connections between components and the PCB. These ovens are designed to handle various types of soldering processes, including lead-free soldering, which is increasingly important due to environmental regulations. The market for these ovens is driven by the growing demand for electronic devices across various sectors, such as consumer electronics, telecommunications, automotive, and industrial applications. As technology advances, the need for more sophisticated and efficient soldering solutions continues to rise, prompting manufacturers to innovate and improve their offerings. The market is characterized by a mix of established players and new entrants, each striving to capture a share of the growing demand for high-quality reflow soldering ovens. The competitive landscape is shaped by factors such as technological advancements, product quality, pricing strategies, and customer service.

Convection Ovens, Vapour Phase Ovens in the Global Reflow Soldering Oven Market:

Convection ovens and vapor phase ovens are two primary types of reflow soldering ovens used in the Global Reflow Soldering Oven Market. Convection ovens are the most common type, accounting for a significant portion of the market. These ovens use heated air to transfer heat to the solder paste and components on the PCB. The process involves several stages, including preheating, soaking, reflow, and cooling. During the preheating stage, the temperature is gradually increased to prevent thermal shock to the components. The soaking stage ensures that the entire assembly reaches a uniform temperature, allowing the solder paste to activate and begin melting. In the reflow stage, the temperature is raised to the point where the solder paste becomes fully liquid, forming a strong bond between the components and the PCB. Finally, the cooling stage solidifies the solder joints, ensuring their durability and reliability. Convection ovens are favored for their ability to handle a wide range of PCB sizes and component types, as well as their relatively low operating costs. On the other hand, vapor phase ovens use a different approach to reflow soldering. These ovens rely on the condensation of a vaporized heat transfer fluid to provide the necessary heat for soldering. The process begins by placing the PCB assembly into a chamber filled with the vaporized fluid. As the vapor condenses on the cooler surfaces of the PCB and components, it releases latent heat, causing the solder paste to melt and form the desired connections. Vapor phase ovens offer several advantages over convection ovens, including more uniform heat distribution, reduced risk of overheating, and the ability to solder complex assemblies with minimal thermal stress. However, they are generally more expensive to operate and maintain, which can be a limiting factor for some manufacturers. Despite these differences, both convection and vapor phase ovens play crucial roles in the reflow soldering process, each offering unique benefits that cater to specific manufacturing needs. As the demand for electronic devices continues to grow, the Global Reflow Soldering Oven Market is expected to see increased adoption of both types of ovens, driven by the need for efficient and reliable soldering solutions. Manufacturers are continually exploring new technologies and innovations to enhance the performance and capabilities of these ovens, ensuring they meet the evolving requirements of the electronics industry.

Telecommunication, Consumer Electronics, Automotive, Others in the Global Reflow Soldering Oven Market:

The Global Reflow Soldering Oven Market finds extensive usage across various industries, including telecommunications, consumer electronics, automotive, and others. In the telecommunications sector, reflow soldering ovens are crucial for assembling the complex PCBs used in communication devices such as smartphones, routers, and network infrastructure equipment. The demand for faster and more reliable communication technologies drives the need for high-quality soldering solutions, making reflow soldering ovens an essential component of the manufacturing process. In the consumer electronics industry, reflow soldering ovens are used to assemble a wide range of products, from smartphones and tablets to laptops and gaming consoles. The rapid pace of technological advancements in this sector necessitates the use of efficient and precise soldering techniques to ensure the performance and reliability of electronic devices. Reflow soldering ovens provide the controlled heat required to create strong and durable connections between components, enabling manufacturers to meet the high standards of quality expected by consumers. The automotive industry also relies heavily on reflow soldering ovens for the production of electronic components used in vehicles. As cars become increasingly equipped with advanced electronic systems, such as infotainment systems, navigation devices, and safety features, the demand for reliable soldering solutions continues to grow. Reflow soldering ovens play a vital role in ensuring the integrity and performance of these electronic systems, contributing to the overall safety and functionality of modern vehicles. Beyond these primary industries, reflow soldering ovens are also used in various other applications, including industrial equipment, medical devices, and aerospace technology. In each of these areas, the need for precise and reliable soldering solutions is paramount, driving the adoption of reflow soldering ovens as a critical component of the manufacturing process. As the Global Reflow Soldering Oven Market continues to expand, manufacturers are increasingly focused on developing innovative solutions that cater to the diverse needs of these industries, ensuring they remain competitive in an ever-evolving market landscape.

Global Reflow Soldering Oven Market Outlook:

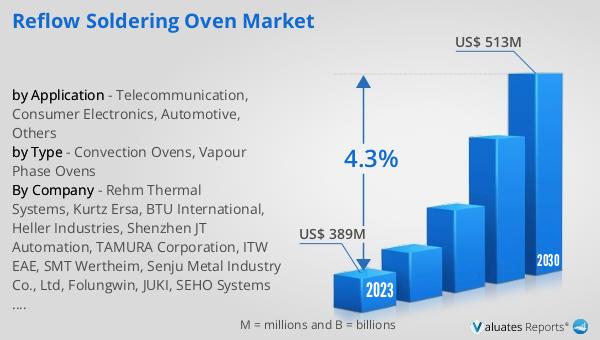

The global market for reflow soldering ovens was valued at $399 million in 2024 and is anticipated to grow to a revised size of $532 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.3% over the forecast period. The top five manufacturers in this market hold approximately 43% of the global share, indicating a competitive landscape dominated by a few key players. The Asia-Pacific region stands out as the largest production area, accounting for nearly 78% of the market share, highlighting its significance in the global electronics manufacturing industry. Within the product categories, convection ovens emerge as the largest segment, capturing over 84% of the market share. This dominance can be attributed to their widespread use and versatility in handling various PCB sizes and component types. The market dynamics are shaped by factors such as technological advancements, increasing demand for electronic devices, and the need for efficient and reliable soldering solutions. As the industry continues to evolve, manufacturers are focused on enhancing their product offerings to meet the growing demands of the market, ensuring they remain competitive in this rapidly changing landscape.

| Report Metric | Details |

| Report Name | Reflow Soldering Oven Market |

| Accounted market size in year | US$ 399 million |

| Forecasted market size in 2031 | US$ 532 million |

| CAGR | 4.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Rehm Thermal Systems, Kurtz Ersa, BTU International, Heller Industries, Shenzhen JT Automation, TAMURA Corporation, ITW EAE, SMT Wertheim, Senju Metal Industry Co., Ltd, Folungwin, JUKI, SEHO Systems GmbH, Suneast, ETA, Papaw, EIGHTECH TECTRON |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |