What is Global Blood Collection Tubes Sales Market?

The Global Blood Collection Tubes Sales Market refers to the worldwide industry focused on the production, distribution, and sale of blood collection tubes. These tubes are essential components in medical diagnostics and research, used to collect, store, and transport blood samples from patients to laboratories. The market encompasses a variety of tube types, each designed for specific purposes, such as serum separation, plasma separation, and whole blood collection. The demand for blood collection tubes is driven by the increasing prevalence of diseases, advancements in healthcare infrastructure, and the growing need for accurate diagnostic testing. As healthcare systems worldwide continue to expand and improve, the market for blood collection tubes is expected to grow, driven by technological innovations and the rising importance of preventive healthcare. The market is characterized by a mix of established players and new entrants, each striving to offer high-quality, reliable products that meet the stringent standards of the medical industry.

in the Global Blood Collection Tubes Sales Market:

In the Global Blood Collection Tubes Sales Market, various types of tubes are utilized by different customers based on their specific needs and applications. One of the most common types is the serum separation tube, which contains a clot activator and a gel for serum separation. These tubes are widely used in clinical chemistry tests, where the serum is required for analysis. Another popular type is the plasma separation tube, which contains anticoagulants such as EDTA, heparin, or citrate to prevent blood clotting. These tubes are essential for tests that require plasma, such as coagulation tests and certain biochemical assays. Whole blood collection tubes, which do not contain any additives, are used when the entire blood sample is needed for analysis, such as in blood typing and cross-matching. Additionally, there are specialized tubes designed for specific tests, such as glucose tubes that contain sodium fluoride to preserve glucose levels, and ESR tubes used for erythrocyte sedimentation rate tests. The choice of tube depends on the test requirements, the type of sample needed, and the preferences of the healthcare provider. Customers in this market include hospitals, diagnostic laboratories, blood banks, and research institutions, each with unique needs and preferences. Hospitals and diagnostic laboratories are the largest consumers, as they perform a wide range of tests that require different types of blood collection tubes. Blood banks primarily use tubes for blood typing and cross-matching, while research institutions may require specialized tubes for specific studies. The market is also influenced by regulatory standards and guidelines, which dictate the types of tubes that can be used for certain tests and the quality standards they must meet. Manufacturers in this market must ensure that their products comply with these regulations to ensure safety and accuracy in blood sample collection and analysis. As the demand for accurate and reliable diagnostic testing continues to grow, the Global Blood Collection Tubes Sales Market is expected to expand, with new innovations and advancements in tube design and materials.

in the Global Blood Collection Tubes Sales Market:

The Global Blood Collection Tubes Sales Market serves a wide range of applications across various sectors, each requiring specific types of tubes for different purposes. In the healthcare sector, blood collection tubes are primarily used for diagnostic testing, which includes routine blood tests, biochemical assays, and specialized tests for detecting diseases and monitoring health conditions. These tests are crucial for diagnosing conditions such as diabetes, cardiovascular diseases, infections, and cancers. In addition to diagnostics, blood collection tubes are also used in therapeutic applications, such as blood transfusions and stem cell therapies. Blood banks rely on these tubes for collecting and storing blood samples for transfusions, ensuring that the blood is safe and compatible with the recipient. In research and development, blood collection tubes play a vital role in clinical trials and studies aimed at understanding diseases and developing new treatments. Researchers use these tubes to collect and analyze blood samples from study participants, enabling them to gather valuable data on the efficacy and safety of new drugs and therapies. The pharmaceutical industry also utilizes blood collection tubes for pharmacokinetic studies, which involve analyzing blood samples to understand how drugs are absorbed, distributed, metabolized, and excreted in the body. This information is critical for determining the appropriate dosage and administration of new medications. Furthermore, blood collection tubes are used in forensic science for collecting and analyzing blood samples in criminal investigations. Forensic experts use these samples to identify suspects, determine the cause of death, and gather evidence for legal proceedings. The versatility and reliability of blood collection tubes make them indispensable tools in various fields, contributing to advancements in healthcare, research, and forensic science. As the demand for accurate and efficient blood sample collection continues to rise, the Global Blood Collection Tubes Sales Market is poised for growth, driven by innovations in tube design and materials that enhance their performance and usability.

Global Blood Collection Tubes Sales Market Outlook:

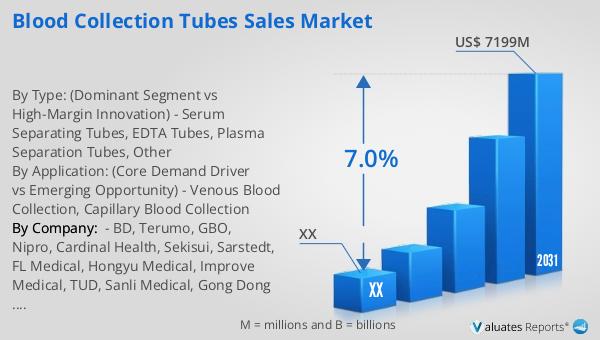

The global Blood Collection Tubes market was valued at approximately US$ 4501 million in 2024, and it is projected to grow to an adjusted size of around US$ 7199 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.0% during the forecast period from 2025 to 2031. This growth is indicative of the increasing demand for blood collection tubes driven by advancements in healthcare and the rising need for diagnostic testing. The market is highly competitive, with the top four players accounting for about 50% of the total market share, highlighting the dominance of key players in the industry. Europe stands out as the largest consumer of blood collection tubes, with a consumption market share of nearly 36.2% in 2023. This significant share can be attributed to the well-established healthcare infrastructure in Europe, coupled with the high prevalence of chronic diseases that necessitate regular blood testing. The market dynamics are influenced by various factors, including technological advancements, regulatory standards, and the growing emphasis on preventive healthcare. As the market continues to evolve, companies are focusing on developing innovative products that meet the changing needs of healthcare providers and patients. The competitive landscape is characterized by strategic collaborations, mergers, and acquisitions, as companies strive to expand their market presence and enhance their product offerings. Overall, the Global Blood Collection Tubes Sales Market is poised for significant growth, driven by the increasing demand for accurate and reliable diagnostic testing and the continuous advancements in healthcare technology.

| Report Metric | Details |

| Report Name | Blood Collection Tubes Sales Market |

| Forecasted market size in 2031 | US$ 7199 million |

| CAGR | 7.0% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | BD, Terumo, GBO, Nipro, Cardinal Health, Sekisui, Sarstedt, FL Medical, Hongyu Medical, Improve Medical, TUD, Sanli Medical, Gong Dong Medical, CDRICH, Xinle Medical, Lingen Precision Medical, WEGO, Kang Jian Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |