What is Global Inositol Sales Market?

The Global Inositol Sales Market refers to the worldwide trade and distribution of inositol, a naturally occurring compound found in various foods and produced by the human body. Inositol is a type of sugar alcohol with several health benefits, including supporting mental health, improving metabolic conditions, and enhancing fertility. The market encompasses the production, distribution, and sale of inositol in various forms, such as powders, capsules, and liquids, catering to diverse industries like pharmaceuticals, food and beverages, and dietary supplements. The demand for inositol is driven by its increasing application in health and wellness products, as consumers become more health-conscious and seek natural alternatives for managing conditions like anxiety, depression, and polycystic ovary syndrome (PCOS). The market is characterized by a competitive landscape with several key players striving to innovate and expand their product offerings to meet the growing consumer demand. Additionally, the market is influenced by factors such as regulatory policies, technological advancements in production processes, and the rising awareness of inositol's health benefits. As a result, the Global Inositol Sales Market is poised for steady growth, with opportunities for expansion in emerging markets and the potential for new applications in various sectors.

in the Global Inositol Sales Market:

In the Global Inositol Sales Market, various types of inositol are utilized by different customers based on their specific needs and preferences. The most common form of inositol is myo-inositol, which is widely used due to its effectiveness in treating conditions like PCOS, anxiety, and depression. Myo-inositol is often preferred by consumers seeking natural remedies for hormonal imbalances and mental health issues, as it is known to improve insulin sensitivity and support neurotransmitter function. Another popular type is D-chiro-inositol, which is frequently used in combination with myo-inositol to enhance its therapeutic effects, particularly in managing PCOS and improving ovarian function. This combination is favored by women looking to regulate their menstrual cycles and boost fertility. Additionally, inositol hexaphosphate (IP6), also known as phytic acid, is used for its antioxidant properties and potential cancer-fighting benefits. IP6 is commonly consumed by individuals seeking to enhance their immune system and protect against chronic diseases. Furthermore, inositol is available in various forms, such as powders, capsules, and liquids, catering to different consumer preferences and usage requirements. Powders are often chosen by those who prefer to mix inositol with beverages or food, while capsules offer a convenient and precise dosage option for on-the-go consumption. Liquid inositol is favored by individuals who have difficulty swallowing pills or prefer a faster absorption rate. The diverse range of inositol types and forms available in the market allows consumers to select products that best suit their health goals and lifestyle needs. Moreover, the increasing awareness of inositol's health benefits has led to its incorporation into various health and wellness products, such as dietary supplements, functional foods, and beverages. This trend is driven by the growing demand for natural and effective solutions for managing health conditions and improving overall well-being. As a result, manufacturers are continuously innovating and expanding their product offerings to meet the evolving needs of consumers in the Global Inositol Sales Market.

in the Global Inositol Sales Market:

Inositol finds applications across a wide range of industries, driven by its versatile health benefits and functional properties. One of the primary applications of inositol is in the pharmaceutical industry, where it is used as an active ingredient in medications for mental health disorders, such as anxiety and depression. Inositol's ability to support neurotransmitter function and improve mood makes it a valuable component in the formulation of antidepressants and anti-anxiety drugs. Additionally, inositol is used in the treatment of metabolic disorders, such as diabetes and insulin resistance, due to its role in enhancing insulin sensitivity and regulating blood sugar levels. Another significant application of inositol is in the dietary supplements industry, where it is marketed as a natural remedy for various health conditions, including PCOS, infertility, and high cholesterol. Inositol supplements are popular among consumers seeking to improve their reproductive health, manage hormonal imbalances, and support cardiovascular health. Furthermore, inositol is incorporated into functional foods and beverages, such as energy drinks, protein bars, and fortified cereals, to enhance their nutritional profile and offer additional health benefits. The food and beverage industry utilizes inositol for its potential to improve mental clarity, boost energy levels, and support overall well-being. Inositol is also used in the cosmetic industry, where it is added to skincare and haircare products for its moisturizing and anti-aging properties. Its ability to promote healthy skin and hair makes it a sought-after ingredient in beauty and personal care formulations. Moreover, inositol is employed in the animal feed industry to improve the health and productivity of livestock. It is used as a feed additive to enhance growth, boost immunity, and improve reproductive performance in animals. The diverse applications of inositol across various industries highlight its versatility and growing importance in the global market. As consumer awareness of inositol's health benefits continues to rise, its demand is expected to increase, driving further innovation and expansion in the Global Inositol Sales Market.

Global Inositol Sales Market Outlook:

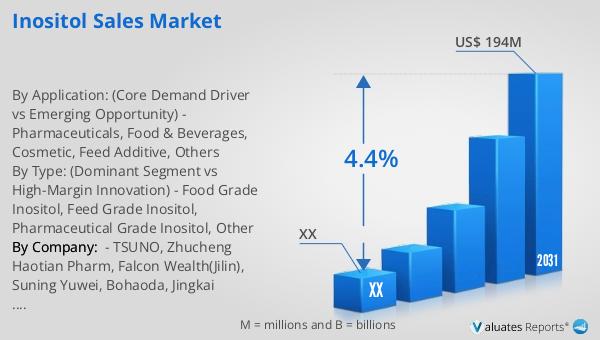

The global inositol market was valued at approximately $144 million in 2024, and it is projected to grow to an estimated $194 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.4% during the forecast period from 2025 to 2031. This growth is indicative of the increasing demand for inositol across various industries, driven by its health benefits and versatile applications. The market is dominated by the top three players, who collectively hold about 73% of the market share, highlighting the competitive nature of the industry. China emerges as the largest market for inositol, accounting for approximately 27% of the global share, followed by Europe and North America, with shares of 24% and 13%, respectively. This regional distribution underscores the widespread adoption of inositol in different parts of the world, with China leading the charge due to its robust manufacturing capabilities and growing consumer base. In terms of application, the food and beverages sector holds a significant share of about 39%, reflecting the increasing incorporation of inositol into functional foods and drinks to enhance their nutritional value and health benefits. This trend is driven by the rising consumer demand for natural and effective solutions to improve health and well-being. As the market continues to evolve, the focus remains on innovation and expansion to meet the diverse needs of consumers and capitalize on the growing opportunities in the Global Inositol Sales Market.

| Report Metric | Details |

| Report Name | Inositol Sales Market |

| Forecasted market size in 2031 | US$ 194 million |

| CAGR | 4.4% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | TSUNO, Zhucheng Haotian Pharm, Falcon Wealth(Jilin), Suning Yuwei, Bohaoda, Jingkai Biotechnology, Zouping Chenshi Bio-engineering, Huaheng Biotechnology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |