What is Global Ultra-high Purity Disilane Market?

The Global Ultra-high Purity Disilane Market is a specialized segment within the chemical industry that focuses on the production and distribution of disilane with extremely high purity levels. Disilane, a compound consisting of silicon and hydrogen, is used primarily in the semiconductor and solar energy industries due to its ability to deposit thin films of silicon. The term "ultra-high purity" refers to the minimal presence of impurities, which is crucial for applications that require precise and reliable performance, such as in the manufacturing of semiconductors and photovoltaic cells. The market for ultra-high purity disilane is driven by the increasing demand for advanced electronic devices and renewable energy solutions. As technology continues to evolve, the need for materials that can support smaller, faster, and more efficient electronic components grows, making ultra-high purity disilane an essential material. The market is characterized by a focus on innovation and quality, with manufacturers striving to meet the stringent purity requirements of their clients. This market is also influenced by global economic trends, technological advancements, and regulatory standards that impact the production and application of high-purity chemicals.

4.5N, 5N, 6N, 7N, Other in the Global Ultra-high Purity Disilane Market:

In the Global Ultra-high Purity Disilane Market, the purity levels of disilane are categorized into different grades, namely 4.5N, 5N, 6N, 7N, and others. These grades indicate the number of nines in the purity percentage, with higher numbers representing higher purity levels. The 4.5N grade, which stands for 99.995% purity, is often used in applications where slightly lower purity is acceptable, such as in some industrial processes or less critical semiconductor applications. This grade is typically more cost-effective and is used when the highest purity is not necessary. The 5N grade, or 99.999% purity, is a step up and is commonly used in more demanding applications within the semiconductor industry, where the presence of impurities can significantly affect the performance of electronic components. As the purity level increases to 6N, or 99.9999%, the applications become even more specialized. This grade is essential for high-performance semiconductor devices, where even the smallest impurity can lead to defects or failures in the final product. The 6N grade is also used in the production of advanced photovoltaic cells, where efficiency and reliability are paramount. The highest standard, 7N, or 99.99999% purity, is reserved for the most critical applications, such as in the production of cutting-edge semiconductor technologies and research and development projects that require the utmost precision. This level of purity ensures that the materials used do not introduce any variables that could compromise the integrity of the final product. Other grades, which may fall between these standard categories, are tailored to specific customer requirements and applications, offering a balance between cost and performance. The choice of purity level depends on the specific needs of the application, the sensitivity of the process to impurities, and the cost considerations of the end-user. As technology advances, the demand for higher purity levels is expected to increase, driving innovation and competition within the market. Manufacturers are continually investing in research and development to improve purification processes and meet the evolving needs of their customers. The ability to produce ultra-high purity disilane reliably and cost-effectively is a key competitive advantage in this market, as it directly impacts the performance and quality of the end products in which it is used.

Semiconductor Industry, Solar Energy Industry in the Global Ultra-high Purity Disilane Market:

The usage of Global Ultra-high Purity Disilane Market in the semiconductor industry is pivotal due to its role in the deposition of silicon layers, which are fundamental to the manufacturing of semiconductor devices. Disilane is used in chemical vapor deposition (CVD) processes to create thin films of silicon on semiconductor wafers. These films are essential for the production of integrated circuits, transistors, and other electronic components that form the backbone of modern electronic devices. The high purity of disilane ensures that the silicon layers are free from impurities that could affect the electrical properties of the semiconductors, leading to improved performance and reliability. As the demand for smaller, faster, and more efficient electronic devices grows, the need for ultra-high purity disilane in the semiconductor industry continues to rise. In the solar energy industry, ultra-high purity disilane is used in the production of photovoltaic cells, which convert sunlight into electricity. The purity of the disilane is crucial in this application because impurities can reduce the efficiency of the solar cells, leading to lower energy output. By using ultra-high purity disilane, manufacturers can produce solar cells with higher efficiency and longer lifespans, making solar energy a more viable and sustainable energy source. The use of disilane in the solar energy industry is driven by the global push towards renewable energy solutions and the need to reduce carbon emissions. As the world seeks to transition to cleaner energy sources, the demand for high-quality photovoltaic cells is expected to increase, further driving the need for ultra-high purity disilane. Both the semiconductor and solar energy industries are characterized by rapid technological advancements and a constant push for higher performance and efficiency. This creates a dynamic market environment where the ability to produce and supply ultra-high purity disilane is a critical factor for success. Manufacturers in this market must continuously innovate and improve their production processes to meet the stringent purity requirements and keep up with the evolving needs of their customers. The global market for ultra-high purity disilane is thus closely linked to the growth and development of these two key industries, with demand expected to rise as technology continues to advance and the world moves towards more sustainable energy solutions.

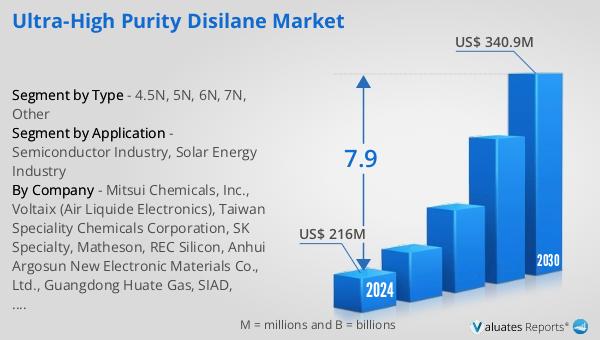

Global Ultra-high Purity Disilane Market Outlook:

The global market for ultra-high purity disilane was valued at approximately $231 million in 2024, reflecting its significant role in industries that demand high-purity materials. This market is projected to grow substantially, reaching an estimated size of $391 million by 2031. This growth represents a compound annual growth rate (CAGR) of 7.9% over the forecast period. The increasing demand for ultra-high purity disilane is driven by its critical applications in the semiconductor and solar energy industries, where the need for high-performance and efficient materials is paramount. As technology continues to advance, the requirements for purity and quality in these industries become more stringent, leading to a greater reliance on ultra-high purity disilane. The market's growth is also supported by the global trend towards renewable energy solutions and the increasing adoption of advanced electronic devices. As the world moves towards more sustainable energy sources and the demand for cutting-edge technology rises, the need for ultra-high purity disilane is expected to grow. This market outlook highlights the importance of ultra-high purity disilane in supporting technological advancements and the transition to a more sustainable future. The ability to produce and supply high-quality disilane is a key factor for success in this market, as it directly impacts the performance and reliability of the end products in which it is used.

| Report Metric | Details |

| Report Name | Ultra-high Purity Disilane Market |

| Accounted market size in year | US$ 231 million |

| Forecasted market size in 2031 | US$ 391 million |

| CAGR | 7.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Mitsui Chemicals, Inc., Voltaix (Air Liquide Electronics), Taiwan Speciality Chemicals Corporation, SK Specialty, Matheson, REC Silicon, Anhui Argosun New Electronic Materials Co., Ltd., Guangdong Huate Gas, SIAD, Spectrum Materials Corporation Limited., Xunding Semiconductor Material Technology, Baoding North Special Gases Co,ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |