What is Global Wire Rods for Automotive Electronics Market?

The Global Wire Rods for Automotive Electronics Market is a crucial segment within the automotive industry, focusing on the production and supply of wire rods used in various electronic components of vehicles. These wire rods are essential for the efficient functioning of automotive electronics, which include systems for engine management, safety, infotainment, and more. As vehicles become increasingly sophisticated with advanced electronic systems, the demand for high-quality wire rods has surged. These rods are typically made from materials like copper and aluminum, known for their excellent conductivity and durability. The market is driven by the growing trend of vehicle electrification and the integration of smart technologies in automobiles. Additionally, stringent regulations regarding vehicle emissions and fuel efficiency are pushing manufacturers to adopt advanced electronic systems, further boosting the demand for wire rods. The market is characterized by continuous innovation, with manufacturers focusing on developing wire rods that offer better performance, reliability, and cost-effectiveness. As the automotive industry continues to evolve, the Global Wire Rods for Automotive Electronics Market is expected to play a pivotal role in supporting the transition towards more efficient and technologically advanced vehicles.

Copper Core Wire, Aluminum Core Wire, Other in the Global Wire Rods for Automotive Electronics Market:

In the Global Wire Rods for Automotive Electronics Market, wire rods are primarily categorized based on the core material used, with copper core wire and aluminum core wire being the most prevalent. Copper core wire is highly favored due to its superior electrical conductivity, which ensures efficient power transmission and minimal energy loss. This makes it an ideal choice for critical automotive applications where reliability and performance are paramount. Copper's excellent thermal conductivity also aids in heat dissipation, enhancing the durability and longevity of electronic components. However, copper is relatively heavy and expensive, which can be a drawback in applications where weight and cost are significant considerations. On the other hand, aluminum core wire offers a lightweight and cost-effective alternative to copper. Although aluminum has lower electrical conductivity compared to copper, advancements in technology have enabled the development of aluminum alloys that improve its performance. Aluminum core wires are particularly advantageous in applications where weight reduction is crucial, such as in electric vehicles, where minimizing weight can enhance battery efficiency and overall vehicle performance. Additionally, aluminum's resistance to corrosion makes it suitable for use in harsh automotive environments. Beyond copper and aluminum, other materials are also being explored for wire rod production, driven by the need for improved performance and sustainability. These include composite materials and advanced alloys that offer a balance between conductivity, weight, and cost. The choice of core material often depends on the specific requirements of the automotive application, with manufacturers carefully considering factors such as conductivity, weight, cost, and environmental impact. As the automotive industry continues to innovate, the development of new materials and technologies for wire rods is expected to play a crucial role in meeting the evolving demands of automotive electronics.

Engine, Ventilation System, Sensor, Other in the Global Wire Rods for Automotive Electronics Market:

The usage of Global Wire Rods for Automotive Electronics Market extends across various critical areas within a vehicle, including the engine, ventilation system, sensors, and other electronic components. In the engine, wire rods are integral to the functioning of the engine control unit (ECU), which manages various engine parameters to optimize performance, fuel efficiency, and emissions. High-quality wire rods ensure reliable communication between the ECU and other engine components, enabling precise control over ignition timing, fuel injection, and other critical functions. In the ventilation system, wire rods are used in the electronic control units that regulate airflow and temperature within the vehicle cabin. These systems rely on accurate and efficient electrical connections to maintain a comfortable environment for passengers. Wire rods also play a vital role in the operation of sensors, which are increasingly used in modern vehicles for various applications, including safety, navigation, and performance monitoring. Sensors require reliable electrical connections to transmit data accurately and efficiently, and high-quality wire rods are essential in ensuring the integrity of these connections. Beyond these specific areas, wire rods are used in a wide range of other automotive electronic applications, including lighting systems, infotainment systems, and advanced driver-assistance systems (ADAS). In each of these applications, the quality and performance of the wire rods are critical to the overall functionality and reliability of the electronic systems. As vehicles become more advanced and reliant on electronic systems, the demand for high-quality wire rods is expected to continue growing, driving innovation and development in the Global Wire Rods for Automotive Electronics Market.

Global Wire Rods for Automotive Electronics Market Outlook:

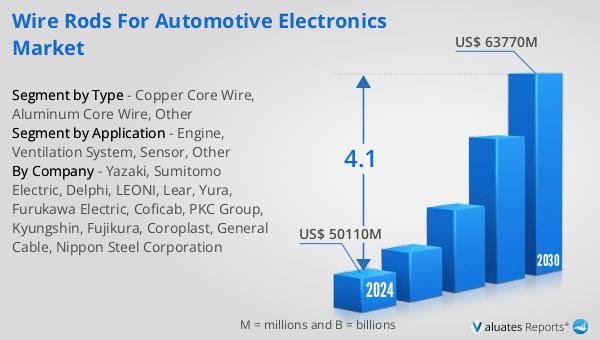

The global market for Wire Rods for Automotive Electronics was valued at approximately $51,960 million in 2024. This market is anticipated to expand significantly, reaching an estimated size of $68,560 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.1% over the forecast period. The steady increase in market size reflects the rising demand for advanced automotive electronics, driven by the ongoing trends of vehicle electrification and the integration of smart technologies. As automotive manufacturers strive to meet stringent regulatory requirements for emissions and fuel efficiency, the adoption of sophisticated electronic systems is becoming increasingly essential. This, in turn, fuels the demand for high-quality wire rods that can support the complex electrical architectures of modern vehicles. The market's growth is also supported by continuous innovation in wire rod materials and manufacturing processes, aimed at enhancing performance, reliability, and cost-effectiveness. As the automotive industry continues to evolve, the Global Wire Rods for Automotive Electronics Market is poised to play a crucial role in enabling the transition towards more efficient and technologically advanced vehicles. The projected growth underscores the importance of wire rods in supporting the development of next-generation automotive electronics, ensuring that vehicles are equipped with the necessary infrastructure to meet the demands of the future.

| Report Metric | Details |

| Report Name | Wire Rods for Automotive Electronics Market |

| Accounted market size in year | US$ 51960 million |

| Forecasted market size in 2031 | US$ 68560 million |

| CAGR | 4.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Yazaki, Sumitomo Electric, Delphi, LEONI, Lear, Yura, Furukawa Electric, Coficab, PKC Group, Kyungshin, Fujikura, Coroplast, General Cable, Nippon Steel Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |