What is Global Non-woven Unidirectional Carbon Fiber Cloth Market?

The Global Non-woven Unidirectional Carbon Fiber Cloth Market is a specialized segment within the broader carbon fiber industry, focusing on materials that are engineered for high-performance applications. These cloths are made from carbon fibers aligned in a single direction, which enhances their strength and stiffness while minimizing weight. This unique alignment makes them ideal for industries that require materials with high tensile strength and low weight, such as aerospace, automotive, and wind energy. The non-woven aspect refers to the manufacturing process, where fibers are bonded together without weaving, resulting in a fabric that is both lightweight and incredibly strong. This market is driven by the increasing demand for advanced materials that can improve fuel efficiency and reduce emissions in various sectors. As industries continue to seek sustainable and efficient solutions, the demand for non-woven unidirectional carbon fiber cloth is expected to grow. This growth is further supported by technological advancements in manufacturing processes, which are making these materials more accessible and cost-effective. Overall, the Global Non-woven Unidirectional Carbon Fiber Cloth Market represents a critical component in the development of next-generation materials that meet the evolving needs of modern industries.

Weft Free Unidirectional Cloth, Sewing Unidirectional Fabric Cloth, Other in the Global Non-woven Unidirectional Carbon Fiber Cloth Market:

Weft Free Unidirectional Cloth, Sewing Unidirectional Fabric Cloth, and other types of non-woven unidirectional carbon fiber cloths each serve distinct purposes within the market. Weft Free Unidirectional Cloth is designed without cross fibers, which means that the fibers run parallel in one direction. This design maximizes the strength and stiffness of the material along the fiber direction, making it ideal for applications where directional strength is crucial. The absence of weft fibers also reduces the weight of the cloth, which is a significant advantage in industries like aerospace and automotive, where every gram counts. This type of cloth is often used in the construction of components that require high tensile strength and minimal weight, such as aircraft wings and car body panels. On the other hand, Sewing Unidirectional Fabric Cloth incorporates stitching to hold the fibers in place. This stitching can be done using various materials, including polyester or nylon threads, which add a layer of stability to the fabric. The sewing process allows for more complex shapes and forms to be created, which is beneficial in applications that require intricate designs or where the fabric needs to conform to specific contours. This type of cloth is often used in the production of sports equipment, such as bicycles and tennis rackets, where both strength and flexibility are required. Other types of non-woven unidirectional carbon fiber cloths include hybrid fabrics, which combine carbon fibers with other materials like glass or aramid fibers. These hybrid fabrics offer a balance of properties, such as improved impact resistance or enhanced thermal stability, making them suitable for a wide range of applications. For instance, in the marine industry, hybrid fabrics are used to construct lightweight yet durable hulls for boats and yachts. The versatility of these materials allows manufacturers to tailor the properties of the fabric to meet specific requirements, whether it's for increased durability, flexibility, or resistance to environmental factors. As the demand for high-performance materials continues to rise, the market for these specialized cloths is expected to expand, driven by innovations in material science and manufacturing techniques. The ability to customize the properties of these fabrics makes them invaluable in industries that are constantly pushing the boundaries of what is possible, from creating more efficient vehicles to developing cutting-edge sports equipment. Overall, the diversity of products within the Global Non-woven Unidirectional Carbon Fiber Cloth Market highlights the adaptability and potential of these advanced materials in meeting the complex demands of modern engineering and design.

Wind Energy, Automotive, Other in the Global Non-woven Unidirectional Carbon Fiber Cloth Market:

The Global Non-woven Unidirectional Carbon Fiber Cloth Market finds extensive usage across various industries, with wind energy and automotive being two of the most significant areas of application. In the wind energy sector, these carbon fiber cloths are used to manufacture wind turbine blades. The lightweight yet strong nature of the material allows for the production of longer and more efficient blades, which can capture more wind energy and convert it into electricity. This is crucial for improving the efficiency and output of wind turbines, making renewable energy sources more viable and competitive with traditional energy sources. The use of non-woven unidirectional carbon fiber cloth in wind energy not only enhances the performance of the turbines but also contributes to the reduction of greenhouse gas emissions by promoting cleaner energy production. In the automotive industry, the demand for lightweight materials is driven by the need to improve fuel efficiency and reduce emissions. Non-woven unidirectional carbon fiber cloth is used in the production of various automotive components, including body panels, chassis, and interior parts. The material's high strength-to-weight ratio allows manufacturers to reduce the overall weight of vehicles without compromising on safety or performance. This is particularly important as automotive companies strive to meet stringent environmental regulations and consumer demand for more sustainable vehicles. The use of carbon fiber cloth in automotive applications also enhances the aesthetic appeal of vehicles, as it can be molded into complex shapes and finished with a high-quality surface. Beyond wind energy and automotive, non-woven unidirectional carbon fiber cloth is also used in other industries such as aerospace, sports equipment, and construction. In aerospace, the material is used to manufacture aircraft components that require high strength and low weight, such as fuselage sections and wing structures. The use of carbon fiber cloth in aerospace applications contributes to the development of more fuel-efficient aircraft, which is essential for reducing the environmental impact of air travel. In the sports equipment industry, the material is used to produce high-performance gear such as bicycles, golf clubs, and tennis rackets, where the combination of strength, flexibility, and lightweight properties enhances the performance of athletes. In construction, non-woven unidirectional carbon fiber cloth is used to reinforce concrete structures, providing additional strength and durability to buildings and infrastructure. This is particularly beneficial in areas prone to natural disasters, where reinforced structures can withstand extreme forces and protect lives and property. Overall, the versatility and superior properties of non-woven unidirectional carbon fiber cloth make it an invaluable material across a wide range of industries, driving innovation and sustainability in modern engineering and design.

Global Non-woven Unidirectional Carbon Fiber Cloth Market Outlook:

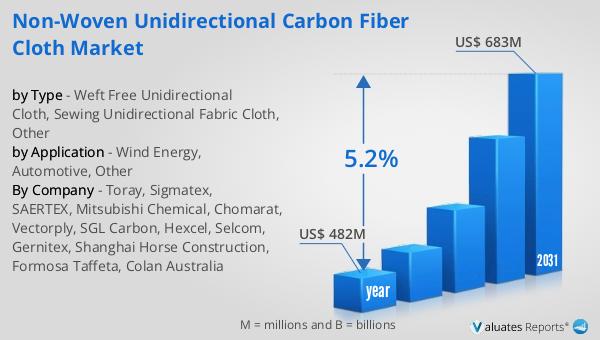

In 2024, the global market for Nonwoven Unidirectional Carbon Fiber Cloth was valued at approximately $482 million. Looking ahead, this market is anticipated to grow significantly, reaching an estimated size of $683 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.2% over the forecast period. This upward trend is indicative of the increasing demand for advanced materials that offer high strength and low weight, which are essential for industries such as aerospace, automotive, and renewable energy. The projected growth of this market is driven by several factors, including technological advancements in manufacturing processes, which are making these materials more accessible and cost-effective. Additionally, the growing emphasis on sustainability and the need for materials that can improve fuel efficiency and reduce emissions are contributing to the rising demand for nonwoven unidirectional carbon fiber cloth. As industries continue to seek innovative solutions to meet the evolving needs of consumers and regulatory requirements, the market for these advanced materials is expected to expand further. This growth not only highlights the importance of nonwoven unidirectional carbon fiber cloth in modern engineering and design but also underscores its potential to drive innovation and sustainability across various sectors.

| Report Metric | Details |

| Report Name | Non-woven Unidirectional Carbon Fiber Cloth Market |

| Accounted market size in year | US$ 482 million |

| Forecasted market size in 2031 | US$ 683 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Toray, Sigmatex, SAERTEX, Mitsubishi Chemical, Chomarat, Vectorply, SGL Carbon, Hexcel, Selcom, Gernitex, Shanghai Horse Construction, Formosa Taffeta, Colan Australia |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |