What is Global Liquid Caprolactam Market?

The Global Liquid Caprolactam Market is a significant segment within the chemical industry, primarily driven by its extensive use in the production of nylon 6 fibers and resins. Caprolactam is a colorless organic compound and a precursor to nylon 6, a widely used synthetic polymer. The market for liquid caprolactam is influenced by the demand for nylon 6, which is utilized in various applications such as textiles, carpets, industrial yarns, and engineering plastics. The growth of industries like automotive, textiles, and electronics, which heavily rely on nylon 6, directly impacts the demand for liquid caprolactam. Additionally, the market is shaped by factors such as technological advancements in production processes, environmental regulations, and the availability of raw materials. The global liquid caprolactam market is characterized by a competitive landscape with several key players striving to enhance their production capacities and expand their geographical reach. As industries continue to innovate and develop new applications for nylon 6, the demand for liquid caprolactam is expected to grow, making it a crucial component in the global chemical market.

Low Purity Caprolactam, High Purity Caprolactam in the Global Liquid Caprolactam Market:

Low Purity Caprolactam and High Purity Caprolactam are two distinct categories within the Global Liquid Caprolactam Market, each serving different industrial needs based on their purity levels. Low Purity Caprolactam typically contains a higher level of impurities, which can affect its performance in certain applications. This type of caprolactam is often used in applications where the presence of impurities does not significantly impact the end product's quality or performance. For instance, it might be used in the production of certain types of nylon 6 where high precision and performance are not critical. On the other hand, High Purity Caprolactam is characterized by its minimal impurity content, making it suitable for applications that demand high performance and precision. This type of caprolactam is essential in the production of high-quality nylon 6 fibers and resins, which are used in demanding applications such as automotive components, electrical and electronic parts, and high-performance textiles. The production of High Purity Caprolactam involves advanced purification processes to ensure that the final product meets stringent quality standards. The choice between Low Purity and High Purity Caprolactam depends on the specific requirements of the application, with considerations for cost, performance, and quality. The market dynamics for these two types of caprolactam are influenced by factors such as technological advancements in purification processes, cost of production, and the specific demands of end-use industries. As industries continue to evolve and demand higher quality materials, the demand for High Purity Caprolactam is expected to grow, while Low Purity Caprolactam will continue to serve applications where cost-effectiveness is a priority. The balance between these two types of caprolactam is crucial for meeting the diverse needs of the global market, ensuring that manufacturers can provide solutions that align with the varying demands of different industries.

Nylon 6, Polyamide Resins, Chemical Solvent, Others in the Global Liquid Caprolactam Market:

The Global Liquid Caprolactam Market finds its usage in several key areas, including Nylon 6, Polyamide Resins, Chemical Solvents, and other applications. Nylon 6 is one of the primary applications of liquid caprolactam, as it serves as a monomer in the polymerization process to produce this versatile synthetic polymer. Nylon 6 is widely used in the textile industry for manufacturing fibers and fabrics due to its excellent strength, elasticity, and abrasion resistance. It is also used in the production of industrial yarns, carpets, and various consumer goods. The automotive industry benefits from nylon 6's lightweight and durable properties, making it suitable for manufacturing components such as gears, bearings, and under-the-hood parts. In the realm of Polyamide Resins, liquid caprolactam is a crucial raw material. Polyamide resins, derived from nylon 6, are used in the production of engineering plastics, which are essential in the automotive, electrical, and electronics industries. These resins offer high mechanical strength, thermal stability, and chemical resistance, making them ideal for demanding applications. Liquid caprolactam is also used as a Chemical Solvent in various industrial processes. Its solvent properties make it suitable for applications in the pharmaceutical and agrochemical industries, where it is used in the synthesis of active ingredients and intermediates. Additionally, liquid caprolactam is employed in the production of coatings, adhesives, and sealants, where its chemical properties enhance the performance and durability of the final products. Beyond these primary applications, liquid caprolactam is utilized in other areas such as the production of synthetic leather, films, and packaging materials. Its versatility and adaptability make it a valuable component in the global chemical market, catering to a wide range of industrial needs. As industries continue to innovate and develop new applications, the demand for liquid caprolactam is expected to grow, further solidifying its position as a key player in the global market.

Global Liquid Caprolactam Market Outlook:

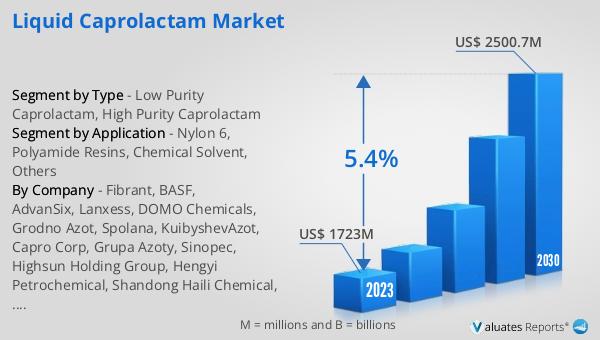

In 2024, the global market for Liquid Caprolactam was valued at approximately $1,913 million. Looking ahead, this market is anticipated to expand significantly, reaching an estimated value of $2,750 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.4% over the forecast period. The steady increase in market size can be attributed to the rising demand for nylon 6 and its derivatives across various industries. As industries such as automotive, textiles, and electronics continue to grow and innovate, the need for high-quality materials like liquid caprolactam becomes more pronounced. This demand is further fueled by advancements in production technologies and the development of new applications for nylon 6. The market's expansion is also supported by the efforts of key players to enhance their production capacities and expand their geographical reach. As a result, the global liquid caprolactam market is poised for sustained growth, driven by the increasing demand for nylon 6 and its applications. This growth not only highlights the importance of liquid caprolactam in the global chemical industry but also underscores its potential as a key driver of innovation and development in various sectors.

| Report Metric | Details |

| Report Name | Liquid Caprolactam Market |

| Accounted market size in year | US$ 1913 million |

| Forecasted market size in 2031 | US$ 2750 million |

| CAGR | 5.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Fibrant, BASF, AdvanSix, Lanxess, DOMO Chemicals, Grodno Azot, Spolana, KuibyshevAzot, Capro Corp, Grupa Azoty, Sinopec, Highsun Holding Group, Hengyi Petrochemical, Shandong Haili Chemical, Fujian Tianchen Yaolong New Material Ltd, Luxi Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |