What is Global HPPD Inhibitor Herbicide Market?

The Global HPPD Inhibitor Herbicide Market refers to the worldwide industry focused on herbicides that inhibit the enzyme 4-hydroxyphenylpyruvate dioxygenase (HPPD). These herbicides are crucial in agriculture as they help control a wide range of weeds that compete with crops for nutrients, water, and sunlight. HPPD inhibitors work by disrupting the synthesis of carotenoids, which are essential for plant growth and survival. This disruption leads to the bleaching and eventual death of the weeds, allowing crops to thrive. The market for these herbicides is driven by the increasing demand for high crop yields and the need for effective weed management solutions. As global populations grow, the pressure on agricultural systems to produce more food intensifies, making efficient herbicides like HPPD inhibitors indispensable. Additionally, the shift towards sustainable farming practices and the need to reduce the environmental impact of agriculture further propel the adoption of these herbicides. The market encompasses various products, each with specific applications and benefits, catering to different crop types and farming conditions. Overall, the Global HPPD Inhibitor Herbicide Market plays a vital role in modern agriculture, supporting food security and sustainable farming practices worldwide.

Mesotrione, Tembotrione, Isoxaflutole, Topramezone, Others in the Global HPPD Inhibitor Herbicide Market:

Mesotrione, Tembotrione, Isoxaflutole, and Topramezone are key products within the Global HPPD Inhibitor Herbicide Market, each offering unique benefits and applications. Mesotrione is a selective herbicide widely used in corn production. It is effective against a broad spectrum of broadleaf and grass weeds, making it a popular choice among farmers. Mesotrione works by inhibiting the HPPD enzyme, leading to the depletion of carotenoids and the subsequent death of the target weeds. Its selectivity ensures that it targets weeds without harming the corn crop, making it an essential tool for corn farmers seeking to maximize yields. Tembotrione, another prominent HPPD inhibitor, is known for its rapid action and broad-spectrum control. It is particularly effective against tough-to-control weeds, providing farmers with a reliable solution for maintaining clean fields. Tembotrione's fast-acting nature allows for timely weed management, ensuring that crops have minimal competition during critical growth stages. Isoxaflutole is a pre-emergence herbicide that offers long-lasting residual control of weeds. It is commonly used in corn and soybean production, providing farmers with a proactive approach to weed management. By applying Isoxaflutole before weeds emerge, farmers can prevent weed establishment and reduce the need for post-emergence treatments. This not only saves time and resources but also minimizes the risk of crop damage. Topramezone is another effective HPPD inhibitor, known for its versatility and broad-spectrum control. It is used in various crops, including corn, sugarcane, and cereals, offering farmers a flexible solution for managing diverse weed populations. Topramezone's ability to control both broadleaf and grass weeds makes it a valuable tool for integrated weed management strategies. In addition to these key products, the Global HPPD Inhibitor Herbicide Market includes other formulations that cater to specific regional needs and crop types. These products are developed to address unique weed challenges and environmental conditions, ensuring that farmers have access to effective solutions tailored to their specific requirements. Overall, the diverse range of HPPD inhibitor herbicides available in the market provides farmers with the tools they need to optimize crop production and maintain sustainable farming practices.

Corn, Sugarcane, Rice, Cereals, Others in the Global HPPD Inhibitor Herbicide Market:

The usage of Global HPPD Inhibitor Herbicide Market products spans various crops, including corn, sugarcane, rice, cereals, and others, each benefiting from the unique properties of these herbicides. In corn production, HPPD inhibitors like Mesotrione and Tembotrione are widely used due to their effectiveness against a broad spectrum of weeds. Corn is a major crop globally, and effective weed management is crucial for maximizing yields. HPPD inhibitors provide corn farmers with a reliable solution for controlling both broadleaf and grass weeds, ensuring that the crop has minimal competition for resources. This is particularly important during the early growth stages when weeds can significantly impact corn development. In sugarcane cultivation, HPPD inhibitors play a vital role in maintaining clean fields and optimizing yields. Sugarcane is a long-duration crop, and effective weed management is essential to prevent yield losses. Products like Topramezone offer sugarcane farmers a versatile solution for controlling diverse weed populations, ensuring that the crop has access to the nutrients and sunlight it needs to thrive. In rice production, HPPD inhibitors are used to manage weeds that compete with rice plants for resources. Rice is a staple food for a large portion of the global population, and effective weed control is crucial for ensuring food security. HPPD inhibitors provide rice farmers with a reliable tool for managing weeds, allowing them to maintain high yields and meet the growing demand for rice. In cereal production, HPPD inhibitors are used to control a wide range of weeds that can impact crop yields. Cereals are a major source of food and feed globally, and effective weed management is essential for ensuring high-quality harvests. HPPD inhibitors offer cereal farmers a reliable solution for controlling both broadleaf and grass weeds, ensuring that the crop has minimal competition for resources. In addition to these major crops, HPPD inhibitors are also used in other agricultural systems, providing farmers with effective weed management solutions tailored to their specific needs. The versatility and effectiveness of HPPD inhibitors make them a valuable tool for modern agriculture, supporting sustainable farming practices and ensuring food security.

Global HPPD Inhibitor Herbicide Market Outlook:

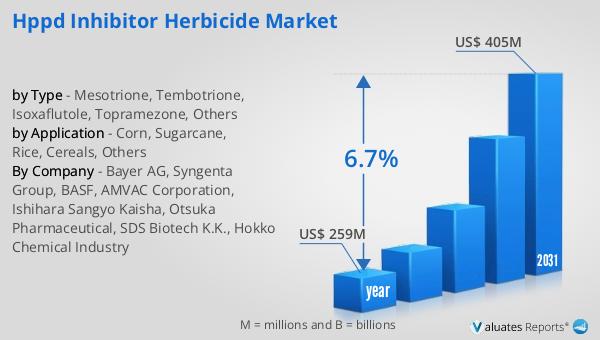

The global market for HPPD Inhibitor Herbicide was valued at $259 million in 2024, and it is anticipated to expand to a revised size of $405 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.7% during the forecast period. This growth trajectory underscores the increasing demand for effective weed management solutions in agriculture. As the global population continues to rise, the pressure on agricultural systems to produce more food intensifies, driving the need for efficient herbicides like HPPD inhibitors. These herbicides play a crucial role in modern agriculture by providing farmers with reliable tools for controlling a wide range of weeds that compete with crops for resources. The projected growth of the HPPD Inhibitor Herbicide Market highlights the importance of these products in supporting sustainable farming practices and ensuring food security. As farmers seek to optimize crop production and minimize environmental impact, the demand for HPPD inhibitors is expected to continue rising. This growth is further supported by advancements in herbicide formulations and the development of new products tailored to specific regional needs and crop types. Overall, the market outlook for HPPD Inhibitor Herbicides reflects the critical role these products play in modern agriculture and their potential to drive sustainable growth in the industry.

| Report Metric | Details |

| Report Name | HPPD Inhibitor Herbicide Market |

| Accounted market size in year | US$ 259 million |

| Forecasted market size in 2031 | US$ 405 million |

| CAGR | 6.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bayer AG, Syngenta Group, BASF, AMVAC Corporation, Ishihara Sangyo Kaisha, Otsuka Pharmaceutical, SDS Biotech K.K., Hokko Chemical Industry |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |