What is Global PGA Plastic Market?

The Global PGA Plastic Market is an intriguing segment within the broader plastics industry, characterized by its unique properties and diverse applications. PGA, or polyglycolic acid, is a biodegradable thermoplastic that has gained significant attention due to its environmental benefits and versatility. This market is driven by the increasing demand for sustainable materials that can replace traditional plastics, which are often non-biodegradable and harmful to the environment. PGA plastic is particularly valued for its high strength, excellent gas barrier properties, and biodegradability, making it suitable for a wide range of applications. The market is witnessing growth due to the rising awareness about environmental issues and the push for greener alternatives in various industries. Additionally, advancements in production technologies and the development of new applications are further propelling the market forward. As industries continue to seek eco-friendly solutions, the demand for PGA plastic is expected to rise, offering promising opportunities for manufacturers and stakeholders in the market. The global PGA plastic market is thus poised for significant growth, driven by its potential to address environmental concerns while meeting the functional requirements of various applications.

Industrial Grade, Medical Grade in the Global PGA Plastic Market:

In the Global PGA Plastic Market, two primary grades are prominently utilized: Industrial Grade and Medical Grade. Industrial Grade PGA plastic is primarily used in applications where durability and performance are crucial. This grade is known for its high mechanical strength and excellent gas barrier properties, making it ideal for packaging applications, particularly in the food and beverage industry. Its ability to decompose naturally without leaving harmful residues makes it a preferred choice for companies aiming to reduce their environmental footprint. Industrial Grade PGA is also used in agriculture, where it serves as a biodegradable alternative to traditional plastics in mulch films and other agricultural products. Its biodegradability ensures that it does not contribute to soil pollution, aligning with the growing trend towards sustainable farming practices. On the other hand, Medical Grade PGA plastic is tailored for applications within the healthcare sector. This grade is highly valued for its biocompatibility and biodegradability, making it suitable for use in medical devices and implants. Medical Grade PGA is often used in the production of sutures, tissue engineering scaffolds, and drug delivery systems. Its ability to safely degrade within the body without causing adverse reactions is a significant advantage, particularly in surgical applications. The use of PGA in medical applications is driven by the need for materials that can provide temporary support or function and then safely dissolve, eliminating the need for additional surgical procedures to remove them. The development of Medical Grade PGA has opened new avenues in the field of regenerative medicine, where it is used to create scaffolds that support the growth of new tissues. This application is particularly promising in the treatment of injuries and degenerative diseases, where the regeneration of damaged tissues is crucial. The versatility of PGA plastic, in both its Industrial and Medical Grades, highlights its potential to address diverse needs across various sectors. As the demand for sustainable and biocompatible materials continues to grow, the Global PGA Plastic Market is expected to expand, offering innovative solutions that cater to the evolving requirements of industries worldwide.

Package, Medical, Agriculture, Oil and Gas, Others in the Global PGA Plastic Market:

The usage of Global PGA Plastic Market spans several key areas, including Packaging, Medical, Agriculture, Oil and Gas, and others. In the Packaging sector, PGA plastic is highly valued for its excellent gas barrier properties and biodegradability. It is used in the production of films and containers that require high strength and the ability to preserve the freshness of perishable goods. The environmental benefits of PGA plastic, such as its ability to decompose naturally, make it an attractive option for companies looking to reduce their carbon footprint and meet consumer demand for sustainable packaging solutions. In the Medical field, PGA plastic is utilized in the production of biodegradable sutures, implants, and drug delivery systems. Its biocompatibility and ability to safely degrade within the body make it an ideal material for temporary medical applications, eliminating the need for additional surgeries to remove devices. This property is particularly beneficial in surgical procedures and regenerative medicine, where PGA scaffolds support tissue growth and healing. In Agriculture, PGA plastic is used in mulch films and other products that require biodegradability to prevent soil pollution. Its use aligns with sustainable farming practices, as it reduces the environmental impact of traditional plastic materials. In the Oil and Gas industry, PGA plastic is employed in applications that require high strength and resistance to harsh conditions. Its biodegradability is an added advantage, as it minimizes environmental impact in sensitive areas. Other applications of PGA plastic include its use in consumer goods and electronics, where its properties are leveraged to create sustainable and high-performance products. The versatility of PGA plastic across these sectors underscores its potential to address diverse needs while promoting environmental sustainability. As industries continue to seek eco-friendly solutions, the demand for PGA plastic is expected to grow, driving innovation and development in the Global PGA Plastic Market.

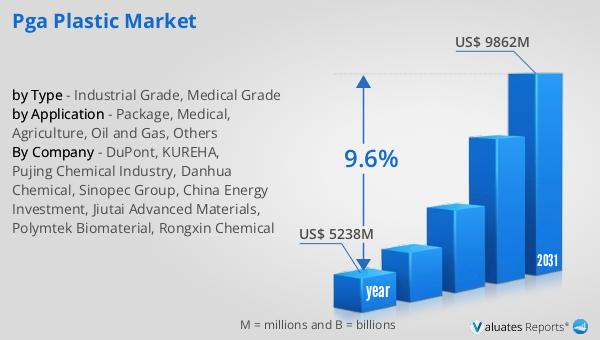

Global PGA Plastic Market Outlook:

The global market for PGA Plastic, initially valued at approximately US$ 5,238 million in 2024, is on a trajectory of significant growth. By 2031, it is anticipated to reach an impressive revised size of US$ 9,862 million, reflecting a robust compound annual growth rate (CAGR) of 9.6% over the forecast period. This growth is indicative of the increasing demand for sustainable and biodegradable materials across various industries. The rising awareness of environmental issues and the push for greener alternatives are key drivers of this market expansion. As industries strive to reduce their carbon footprint and meet consumer demand for eco-friendly products, the adoption of PGA plastic is expected to rise. The market's growth is further supported by advancements in production technologies and the development of new applications that leverage the unique properties of PGA plastic. This upward trend highlights the potential of PGA plastic to address environmental concerns while meeting the functional requirements of diverse applications. As the market continues to evolve, stakeholders and manufacturers are poised to benefit from the opportunities presented by this dynamic and rapidly growing segment. The Global PGA Plastic Market is thus set to play a pivotal role in the transition towards more sustainable and environmentally friendly materials.

| Report Metric | Details |

| Report Name | PGA Plastic Market |

| Accounted market size in year | US$ 5238 million |

| Forecasted market size in 2031 | US$ 9862 million |

| CAGR | 9.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | DuPont, KUREHA, Pujing Chemical Industry, Danhua Chemical, Sinopec Group, China Energy Investment, Jiutai Advanced Materials, Polymtek Biomaterial, Rongxin Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |