What is Global Perfluorosulfonic Acid Proton Exchange Membranes Market?

The Global Perfluorosulfonic Acid Proton Exchange Membranes Market is a specialized segment within the broader chemical and materials industry, focusing on the production and application of proton exchange membranes (PEMs) made from perfluorosulfonic acid. These membranes are crucial components in various electrochemical applications due to their excellent ionic conductivity and chemical stability. They are primarily used in fuel cells, where they facilitate the movement of protons while acting as a barrier to gases, thus enabling the generation of electricity through electrochemical reactions. The market for these membranes is driven by the increasing demand for clean energy solutions, as they play a pivotal role in hydrogen fuel cells, which are seen as a sustainable alternative to fossil fuels. Additionally, these membranes are used in water electrolysis for hydrogen production, further contributing to the green energy landscape. The market is characterized by technological advancements aimed at improving the efficiency and durability of these membranes, as well as efforts to reduce production costs. As industries and governments worldwide push for greener technologies, the demand for perfluorosulfonic acid proton exchange membranes is expected to grow, making it a dynamic and evolving market.

Extrusion, Solution, Composite in the Global Perfluorosulfonic Acid Proton Exchange Membranes Market:

Extrusion, solution, and composite methods are three primary techniques used in the production of perfluorosulfonic acid proton exchange membranes, each offering distinct advantages and challenges. The extrusion process involves melting the polymer and forcing it through a die to form thin sheets or films. This method is advantageous due to its ability to produce membranes with uniform thickness and high mechanical strength. The extrusion process is also relatively fast and cost-effective, making it suitable for large-scale production. However, the high temperatures involved can sometimes lead to degradation of the polymer, affecting the membrane's performance. On the other hand, the solution casting method involves dissolving the polymer in a suitable solvent and then casting it onto a substrate to form a film. This technique allows for better control over the membrane's microstructure, which can enhance its ionic conductivity and selectivity. Solution casting is particularly useful for producing membranes with complex compositions or those that require specific functional additives. However, the process can be more time-consuming and costly due to the need for solvent recovery and recycling. Composite membranes, which combine perfluorosulfonic acid with other materials, offer a way to enhance the properties of the membranes further. By incorporating materials such as inorganic fillers or other polymers, composite membranes can achieve improved thermal stability, mechanical strength, and chemical resistance. The composite approach allows for the tailoring of membrane properties to meet specific application requirements, such as higher operating temperatures or resistance to harsh chemical environments. However, the development of composite membranes can be complex, requiring careful selection and optimization of the materials used to ensure compatibility and performance. Each of these production methods plays a crucial role in the global perfluorosulfonic acid proton exchange membranes market, catering to different application needs and driving innovation in membrane technology. As the demand for high-performance membranes continues to grow, advancements in these production techniques are expected to play a significant role in shaping the future of the market.

Fuel Cell, Hydrogen Generation by Water Electrolysis, Chlor-Alkali Industry, Others in the Global Perfluorosulfonic Acid Proton Exchange Membranes Market:

The Global Perfluorosulfonic Acid Proton Exchange Membranes Market finds its applications in several key areas, each leveraging the unique properties of these membranes to drive technological advancements and sustainability. In the realm of fuel cells, these membranes are indispensable. They serve as the core component in proton exchange membrane fuel cells (PEMFCs), which are used in various applications ranging from portable electronics to vehicles and stationary power generation. The membranes facilitate the movement of protons from the anode to the cathode while preventing the crossover of gases, thus enabling efficient electrochemical reactions that generate electricity. The use of perfluorosulfonic acid membranes in fuel cells is driven by their high ionic conductivity, chemical stability, and durability, making them ideal for both low and high-temperature applications. In hydrogen generation by water electrolysis, these membranes play a crucial role in proton exchange membrane electrolyzers (PEMEs). They enable the efficient separation of hydrogen and oxygen during the electrolysis process, contributing to the production of high-purity hydrogen. This hydrogen can then be used as a clean energy source or as a feedstock in various industrial processes. The growing emphasis on green hydrogen as a sustainable energy carrier is expected to boost the demand for these membranes in electrolysis applications. In the chlor-alkali industry, perfluorosulfonic acid proton exchange membranes are used in membrane cell technology for the production of chlorine and caustic soda. The membranes act as a selective barrier, allowing the passage of sodium ions while preventing the mixing of chlorine and caustic soda, thus enhancing the efficiency and safety of the process. This application underscores the versatility of these membranes in facilitating electrochemical reactions across different industries. Beyond these primary applications, perfluorosulfonic acid proton exchange membranes are also used in other areas such as redox flow batteries, sensors, and electrochemical synthesis. Their ability to provide high ionic conductivity and chemical resistance makes them suitable for a wide range of electrochemical applications, driving innovation and sustainability across various sectors. As industries continue to seek cleaner and more efficient technologies, the role of these membranes in enabling such advancements is likely to expand, highlighting their importance in the global market.

Global Perfluorosulfonic Acid Proton Exchange Membranes Market Outlook:

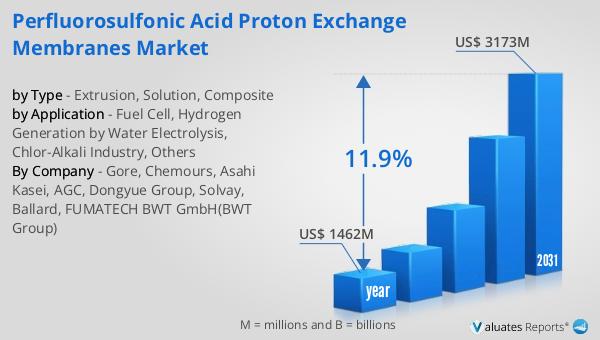

The global market for Perfluorosulfonic Acid Proton Exchange Membranes was valued at $1,462 million in 2024 and is anticipated to grow to a revised size of $3,173 million by 2031, reflecting a compound annual growth rate (CAGR) of 11.9% during the forecast period. The market is dominated by the top three companies, which collectively hold about 75% of the market share. North America stands as the largest market for these membranes, accounting for approximately 32% of the global share, followed by China and Europe with market shares of 28% and 21%, respectively. In terms of product type, the composite segment emerges as the largest, capturing around 65% of the market share. When it comes to applications, fuel cells represent the largest downstream segment, making up about 77% of the market. This significant share underscores the critical role of perfluorosulfonic acid proton exchange membranes in the fuel cell industry, driven by the increasing demand for clean and efficient energy solutions. The market dynamics reflect a growing emphasis on sustainable technologies and the pivotal role these membranes play in advancing such innovations. As the market continues to evolve, the focus remains on enhancing membrane performance and expanding their applications across various industries.

| Report Metric | Details |

| Report Name | Perfluorosulfonic Acid Proton Exchange Membranes Market |

| Accounted market size in year | US$ 1462 million |

| Forecasted market size in 2031 | US$ 3173 million |

| CAGR | 11.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Gore, Chemours, Asahi Kasei, AGC, Dongyue Group, Solvay, Ballard, FUMATECH BWT GmbH(BWT Group) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |