What is Global Digital Dental Equipment Market?

The Global Digital Dental Equipment Market is a rapidly evolving sector within the broader medical device industry, focusing on the integration of digital technology into dental care. This market encompasses a wide range of equipment designed to enhance the precision, efficiency, and outcomes of dental procedures. Digital dental equipment includes tools like intraoral scanners, milling machines, 3D printers, and CAD/CAM systems, which are used to create highly accurate dental restorations such as crowns, bridges, and dentures. The adoption of digital technology in dentistry allows for more streamlined workflows, reduced treatment times, and improved patient experiences. As dental professionals increasingly recognize the benefits of digital solutions, the demand for these advanced tools continues to grow. This market is driven by factors such as the rising prevalence of dental disorders, increasing awareness of oral health, and the growing demand for cosmetic dentistry. Additionally, technological advancements and the integration of artificial intelligence in dental equipment are further propelling the market forward. As a result, the Global Digital Dental Equipment Market is poised for significant growth, offering numerous opportunities for innovation and development in the field of dentistry.

Scanners, Milling Equipment, 3D Printing in the Global Digital Dental Equipment Market:

Scanners, milling equipment, and 3D printing are pivotal components of the Global Digital Dental Equipment Market, each playing a crucial role in modernizing dental practices. Scanners, particularly intraoral scanners, are used to capture detailed 3D images of a patient's teeth and gums. These images are then used to create digital impressions, which are more accurate and comfortable for patients compared to traditional methods. The precision of digital impressions reduces the likelihood of errors in dental restorations, leading to better-fitting crowns, bridges, and other prosthetics. Milling equipment, on the other hand, is used to fabricate dental restorations from materials such as ceramics, composites, and metals. These machines are capable of producing highly precise and durable restorations in a fraction of the time it would take using traditional methods. The integration of CAD/CAM technology with milling equipment allows for the design and production of complex dental structures with ease. 3D printing is another revolutionary technology in the dental field, offering unparalleled flexibility and customization. It enables the production of dental models, surgical guides, aligners, and even dentures with high precision and speed. The ability to quickly produce prototypes and final products reduces the time patients spend waiting for their dental appliances. Moreover, 3D printing allows for the use of a wide range of materials, including biocompatible resins, which are essential for creating safe and effective dental products. The combination of these technologies not only enhances the efficiency of dental practices but also improves patient outcomes by providing more accurate and personalized treatments. As the Global Digital Dental Equipment Market continues to expand, the integration of scanners, milling equipment, and 3D printing will remain at the forefront of dental innovation, driving the industry towards a more digital and patient-centric future.

Hospital, Dental Clinic in the Global Digital Dental Equipment Market:

The usage of Global Digital Dental Equipment Market in hospitals and dental clinics is transforming the landscape of dental care, offering numerous benefits to both healthcare providers and patients. In hospitals, digital dental equipment is used to streamline complex dental procedures, improve diagnostic accuracy, and enhance patient care. The integration of digital technology allows for more precise treatment planning and execution, reducing the risk of complications and improving surgical outcomes. For instance, digital imaging systems provide high-resolution images that aid in the accurate diagnosis of dental conditions, while CAD/CAM systems enable the rapid production of custom dental prosthetics. This not only improves the efficiency of dental departments within hospitals but also enhances the overall patient experience by reducing wait times and improving the quality of care. In dental clinics, digital dental equipment is revolutionizing the way dentists diagnose and treat patients. The use of intraoral scanners, for example, eliminates the need for traditional impression materials, providing a more comfortable experience for patients and reducing the likelihood of errors. Digital workflows also allow for faster turnaround times for dental restorations, enabling dentists to offer same-day services for procedures like crowns and veneers. Additionally, the use of digital technology in dental clinics enhances patient communication and education. Dentists can use digital images and models to explain treatment options and outcomes to patients, improving their understanding and satisfaction with the care they receive. The adoption of digital dental equipment in both hospitals and dental clinics is driven by the need for more efficient, accurate, and patient-centered care. As the Global Digital Dental Equipment Market continues to grow, the integration of these advanced technologies will play a crucial role in shaping the future of dental care, offering new opportunities for innovation and improvement in the field.

Global Digital Dental Equipment Market Outlook:

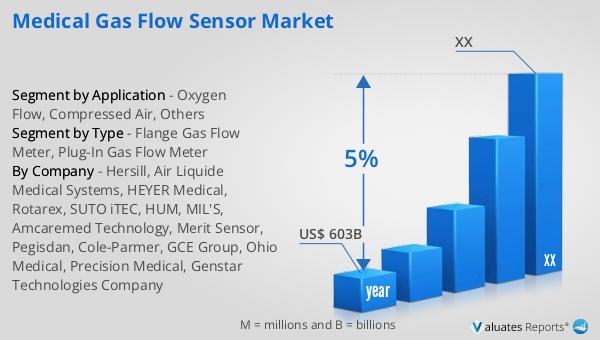

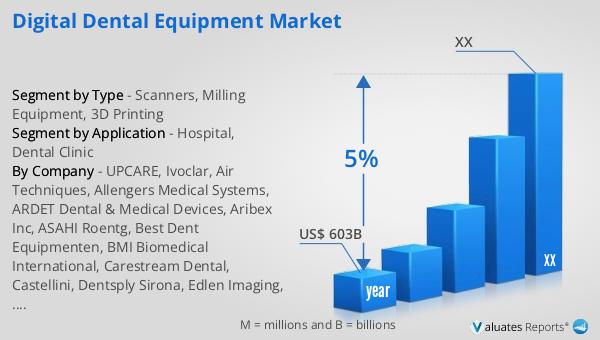

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth trajectory underscores the increasing demand for advanced medical technologies and innovations across various healthcare sectors. The expansion of the medical device market is driven by several factors, including the rising prevalence of chronic diseases, an aging global population, and the growing emphasis on early diagnosis and preventive healthcare. Additionally, technological advancements in medical devices, such as the integration of artificial intelligence, machine learning, and the Internet of Things (IoT), are further propelling market growth. These innovations are enhancing the capabilities of medical devices, improving patient outcomes, and reducing healthcare costs. The increasing adoption of minimally invasive procedures and the growing demand for personalized medicine are also contributing to the expansion of the medical device market. As healthcare systems worldwide continue to evolve, the need for efficient, accurate, and patient-centered medical devices will remain a key driver of market growth. The projected growth of the global medical device market highlights the significant opportunities for innovation and development in the healthcare industry, paving the way for a more advanced and accessible healthcare system.

| Report Metric | Details |

| Report Name | Digital Dental Equipment Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | UPCARE, Ivoclar, Air Techniques, Allengers Medical Systems, ARDET Dental & Medical Devices, Aribex Inc, ASAHI Roentg, Best Dent Equipmenten, BMI Biomedical International, Carestream Dental, Castellini, Dentsply Sirona, Edlen Imaging, FONA Dental, Genoray, Gnatus |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |