What is Global Medical Gas Flow Sensor Market?

The Global Medical Gas Flow Sensor Market is a specialized segment within the broader medical equipment industry, focusing on devices that measure and monitor the flow of medical gases. These sensors are crucial in various healthcare settings, including hospitals, clinics, and home care, where they ensure the accurate delivery of gases like oxygen, nitrous oxide, and carbon dioxide to patients. The sensors are designed to provide precise measurements, which are vital for patient safety and effective treatment outcomes. They help in maintaining the correct flow rates, preventing potential complications arising from incorrect gas delivery. The market for these sensors is driven by the increasing demand for advanced healthcare solutions, the rising prevalence of respiratory diseases, and the growing need for home healthcare services. Technological advancements have led to the development of more sophisticated and reliable sensors, further propelling market growth. Additionally, stringent regulations and standards in the healthcare industry necessitate the use of high-quality flow sensors, ensuring compliance and enhancing patient care. As healthcare systems worldwide continue to evolve, the importance of accurate and reliable medical gas flow sensors is expected to grow, making this market a critical component of modern medical infrastructure.

Flange Type, Plug-In Type in the Global Medical Gas Flow Sensor Market:

In the Global Medical Gas Flow Sensor Market, two prominent types of sensors are Flange Type and Plug-In Type, each serving distinct purposes and offering unique advantages. Flange Type sensors are typically used in applications where a permanent and secure installation is required. These sensors are mounted using flanges, which provide a stable and robust connection to the gas supply system. The design of Flange Type sensors ensures minimal leakage and high accuracy in measuring gas flow, making them ideal for critical applications in hospitals and large healthcare facilities. They are often used in central gas supply systems, where the continuous and precise monitoring of gas flow is essential for patient safety and operational efficiency. The installation process for Flange Type sensors is more complex compared to other types, requiring skilled technicians to ensure proper alignment and sealing. However, once installed, they offer long-term reliability and minimal maintenance, making them a cost-effective solution for healthcare providers. On the other hand, Plug-In Type sensors offer a more flexible and convenient solution for medical gas flow measurement. These sensors are designed for easy installation and removal, allowing healthcare providers to quickly adapt to changing needs and requirements. Plug-In Type sensors are often used in portable and temporary setups, such as mobile clinics or emergency response units, where quick deployment and adaptability are crucial. The design of these sensors allows for easy integration with existing gas supply systems, providing accurate and reliable measurements without the need for extensive modifications. Plug-In Type sensors are also favored in home healthcare settings, where ease of use and minimal maintenance are important considerations for patients and caregivers. Despite their convenience, Plug-In Type sensors may not offer the same level of accuracy and stability as Flange Type sensors, particularly in high-demand or critical applications. However, their versatility and ease of use make them a popular choice for a wide range of medical gas flow measurement needs. Both Flange Type and Plug-In Type sensors play a vital role in the Global Medical Gas Flow Sensor Market, catering to different segments and requirements within the healthcare industry. The choice between these two types often depends on the specific application, installation environment, and budget considerations. As the demand for advanced medical gas flow measurement solutions continues to grow, manufacturers are focusing on developing innovative products that combine the strengths of both Flange Type and Plug-In Type sensors. This includes the integration of advanced technologies such as wireless connectivity, digital displays, and automated calibration features, which enhance the functionality and user experience of these sensors. Additionally, the increasing emphasis on patient safety and regulatory compliance is driving the adoption of high-quality sensors that meet stringent industry standards. As a result, both Flange Type and Plug-In Type sensors are expected to see continued growth and development in the coming years, contributing to the overall expansion of the Global Medical Gas Flow Sensor Market.

Oxygen Flow, Compressed Air, Others in the Global Medical Gas Flow Sensor Market:

The Global Medical Gas Flow Sensor Market finds its application in various areas, including Oxygen Flow, Compressed Air, and others, each serving critical roles in healthcare delivery. Oxygen Flow is one of the most significant applications of medical gas flow sensors, as oxygen therapy is a common treatment for patients with respiratory conditions, such as chronic obstructive pulmonary disease (COPD), asthma, and pneumonia. Accurate measurement and control of oxygen flow are essential to ensure that patients receive the appropriate concentration of oxygen, preventing complications such as hypoxemia or oxygen toxicity. Medical gas flow sensors used in oxygen therapy are designed to provide precise and reliable measurements, enabling healthcare providers to adjust flow rates according to patient needs. These sensors are often integrated into oxygen delivery systems, such as ventilators and oxygen concentrators, where they play a crucial role in monitoring and maintaining optimal oxygen levels. In addition to oxygen flow, medical gas flow sensors are also used in the measurement and control of Compressed Air, which is commonly used in various medical applications, including anesthesia delivery, respiratory therapy, and surgical procedures. Compressed air is often mixed with other gases, such as oxygen or nitrous oxide, to create specific gas mixtures required for different treatments. Accurate measurement of compressed air flow is essential to ensure the correct gas mixture and pressure, which are critical for patient safety and effective treatment outcomes. Medical gas flow sensors used in compressed air applications are designed to withstand high pressures and provide precise measurements, ensuring the safe and efficient delivery of medical gases. These sensors are often used in conjunction with other medical equipment, such as anesthesia machines and respiratory devices, where they help maintain the desired gas flow and pressure levels. Beyond oxygen and compressed air, medical gas flow sensors are also used in various other applications, including the delivery of nitrous oxide, carbon dioxide, and other specialty gases used in medical treatments. Nitrous oxide, for example, is commonly used as an anesthetic agent in dental and surgical procedures, and accurate measurement of its flow is essential to ensure patient safety and comfort. Similarly, carbon dioxide is used in certain medical procedures, such as laparoscopy, where it is used to inflate the abdominal cavity for better visualization and access. Medical gas flow sensors used in these applications are designed to provide accurate and reliable measurements, ensuring the safe and effective delivery of these gases. The versatility and precision of medical gas flow sensors make them an essential component of modern healthcare delivery, enabling healthcare providers to deliver safe and effective treatments across a wide range of medical applications.

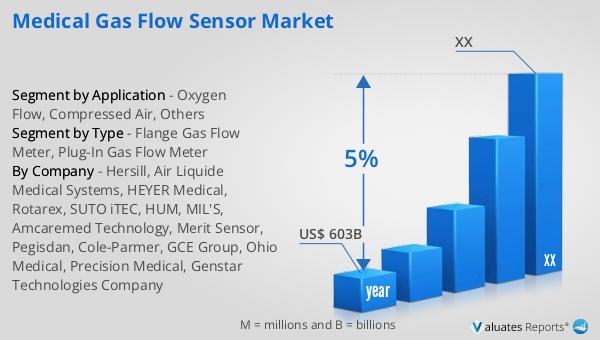

Global Medical Gas Flow Sensor Market Outlook:

The outlook for the Global Medical Gas Flow Sensor Market indicates a promising growth trajectory over the coming years. In 2024, the market was valued at approximately US$ 2,146 million, reflecting its significant role in the healthcare industry. By 2031, it is anticipated that the market will expand to a revised size of around US$ 3,314 million. This growth is expected to occur at a compound annual growth rate (CAGR) of 6.5% during the forecast period. This upward trend underscores the increasing demand for advanced medical gas flow sensors, driven by factors such as the rising prevalence of respiratory diseases, the growing need for home healthcare solutions, and the continuous advancements in sensor technology. The market's expansion is also supported by the stringent regulatory requirements in the healthcare industry, which necessitate the use of high-quality and reliable sensors to ensure patient safety and compliance. As healthcare systems worldwide continue to evolve and adapt to new challenges, the importance of accurate and reliable medical gas flow sensors is expected to grow, making this market a critical component of modern medical infrastructure. The projected growth of the Global Medical Gas Flow Sensor Market highlights the ongoing need for innovative solutions that enhance patient care and improve healthcare delivery.

| Report Metric | Details |

| Report Name | Medical Gas Flow Sensor Market |

| Accounted market size in year | US$ 2146 million |

| Forecasted market size in 2031 | US$ 3314 million |

| CAGR | 6.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Hersill, Sensirion, Renesas, Air Liquide Medical Systems, HEYER Medical, Honeywell, MIL'S, Amcaremed Technology, Rotarex, SUTO iTEC, HUM, GCE Group, Precision Medical, Genstar Technologies Company, Aceinna, Aosong |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |