What is Global Plasma Donor Chairs Market?

The Global Plasma Donor Chairs Market is a specialized segment within the broader medical furniture industry, focusing on the design and manufacture of chairs used in plasma donation centers. Plasma donation is a critical process in healthcare, as plasma is used to create therapies for various medical conditions, including immune deficiencies and bleeding disorders. The chairs used in this process must be designed to ensure donor comfort and safety, as well as facilitate the efficient collection of plasma. These chairs are typically adjustable, allowing donors to recline comfortably during the donation process, which can take up to an hour. They are also equipped with features such as armrests and footrests to enhance comfort and support. The market for plasma donor chairs is driven by the increasing demand for plasma-derived therapies, advancements in chair design and technology, and the expansion of plasma donation centers globally. Manufacturers in this market are focused on developing chairs that are not only comfortable and functional but also durable and easy to clean, meeting the stringent hygiene standards required in medical settings. As the demand for plasma continues to grow, the Global Plasma Donor Chairs Market is expected to expand, offering opportunities for innovation and growth.

Electrical Plasma Donor Chairs, Hydraulic Plasma Donor Chairs, Manual Plasma Donor Chairs in the Global Plasma Donor Chairs Market:

In the Global Plasma Donor Chairs Market, there are three main types of chairs: Electrical Plasma Donor Chairs, Hydraulic Plasma Donor Chairs, and Manual Plasma Donor Chairs. Each type has its unique features and benefits, catering to different needs and preferences of plasma donation centers. Electrical Plasma Donor Chairs are equipped with electric motors that allow for easy adjustment of the chair's position with the push of a button. This type of chair is highly preferred in modern plasma donation centers due to its convenience and ease of use. Donors can be comfortably positioned with minimal effort, and the chair can be adjusted to various angles to facilitate the plasma collection process. These chairs often come with additional features such as built-in massagers and heating elements to enhance donor comfort. Hydraulic Plasma Donor Chairs, on the other hand, use a hydraulic system to adjust the chair's position. While they may not offer the same level of convenience as their electrical counterparts, they are still highly functional and reliable. The hydraulic mechanism allows for smooth and precise adjustments, ensuring that donors are positioned correctly for the plasma donation process. These chairs are often more affordable than electrical chairs, making them a popular choice for smaller donation centers or those with budget constraints. Manual Plasma Donor Chairs are the most basic type, requiring manual adjustment of the chair's position. While they may lack the advanced features of electrical and hydraulic chairs, they are still widely used due to their simplicity and cost-effectiveness. Manual chairs are typically lightweight and easy to move, making them ideal for donation centers with limited space. Despite their simplicity, these chairs are designed to provide adequate comfort and support to donors during the plasma collection process. In summary, the choice between electrical, hydraulic, and manual plasma donor chairs depends on the specific needs and budget of the plasma donation center. Each type of chair offers distinct advantages, and the right choice can enhance the efficiency and comfort of the plasma donation process.

Blood Center, Hospital, Other in the Global Plasma Donor Chairs Market:

The usage of Global Plasma Donor Chairs Market extends across various settings, including Blood Centers, Hospitals, and other healthcare facilities. In Blood Centers, plasma donor chairs are essential for facilitating the plasma donation process. These centers are specifically designed for the collection of blood and plasma, and the chairs play a crucial role in ensuring donor comfort and safety. The chairs are typically arranged in a way that maximizes space and allows for efficient workflow, enabling staff to attend to multiple donors simultaneously. In Hospitals, plasma donor chairs are used in blood banks and transfusion departments. Hospitals often have dedicated areas for blood and plasma collection, and the chairs are an integral part of these setups. The chairs must be versatile and adjustable to accommodate donors of different sizes and preferences. Additionally, hospitals may require chairs with advanced features such as electronic controls and built-in monitoring systems to ensure the safety and comfort of donors. In other healthcare facilities, such as clinics and mobile donation units, plasma donor chairs are used to facilitate plasma collection in a variety of settings. These chairs must be portable and easy to set up, allowing for flexibility in different environments. Mobile donation units, in particular, require chairs that are lightweight and compact, enabling them to be transported easily from one location to another. Overall, the usage of plasma donor chairs in these settings is driven by the need for efficient and comfortable plasma collection processes. The chairs must be designed to meet the specific requirements of each setting, ensuring that donors have a positive experience and that the plasma collection process is carried out smoothly and safely.

Global Plasma Donor Chairs Market Outlook:

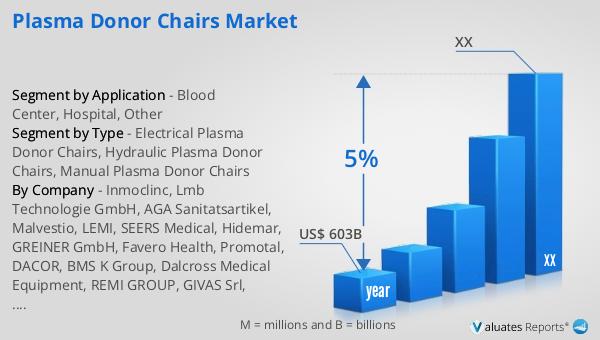

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is indicative of the increasing demand for advanced medical technologies and devices across the globe. The medical device industry encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices, all of which play a crucial role in modern healthcare. The steady growth rate reflects the ongoing advancements in medical technology, as well as the rising prevalence of chronic diseases that require sophisticated medical interventions. As healthcare systems worldwide continue to evolve and expand, the demand for innovative medical devices is expected to rise, driving further growth in the market. This growth also highlights the importance of continued investment in research and development to bring new and improved medical devices to market. The expansion of the medical device market presents significant opportunities for manufacturers, healthcare providers, and patients alike, as it promises to enhance the quality of care and improve patient outcomes.

| Report Metric | Details |

| Report Name | Plasma Donor Chairs Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Inmoclinc, Lmb Technologie GmbH, AGA Sanitatsartikel, Malvestio, LEMI, SEERS Medical, Hidemar, GREINER GmbH, Favero Health, Promotal, DACOR, BMS K Group, Dalcross Medical Equipment, REMI GROUP, GIVAS Srl, Brandt Industries, Zhangjiagang Medi Medical Equipment, Wuhan Bio Kingmaker, BIOBASE |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |