What is Global Venipuncture Needle Market?

The Global Venipuncture Needle Market is a crucial segment within the broader medical device industry, focusing on the production and distribution of needles specifically designed for venipuncture, which is the process of obtaining intravenous access for the purpose of intravenous therapy or venous blood sampling. These needles are essential tools in healthcare settings, facilitating the collection of blood samples for diagnostic purposes, administration of medications, and other therapeutic interventions. The market is driven by the increasing prevalence of chronic diseases, rising demand for blood tests, and advancements in healthcare infrastructure across the globe. Additionally, the growing awareness about the importance of early diagnosis and preventive healthcare has further fueled the demand for venipuncture needles. Manufacturers in this market are continually innovating to improve the safety, comfort, and efficiency of these needles, addressing concerns such as needle stick injuries and patient discomfort. The market is characterized by a diverse range of products, including different sizes and types of needles, catering to various medical needs and patient demographics. Overall, the Global Venipuncture Needle Market plays a vital role in supporting healthcare systems worldwide by ensuring the availability of reliable and effective tools for blood collection and intravenous access.

Soft Needle, Rigid Needle in the Global Venipuncture Needle Market:

In the Global Venipuncture Needle Market, two primary types of needles are commonly used: soft needles and rigid needles. Soft needles are designed with flexibility in mind, often featuring a thin, pliable structure that allows for easier insertion and reduced discomfort for patients. These needles are particularly beneficial in situations where multiple venipunctures are required, such as in patients undergoing chemotherapy or those with fragile veins. The flexibility of soft needles minimizes the risk of vein damage and reduces the likelihood of complications, making them a preferred choice in pediatric and geriatric care. On the other hand, rigid needles are characterized by their sturdier construction, providing greater control and precision during insertion. These needles are typically used in procedures where accuracy is paramount, such as in blood donation or when accessing deep veins. The rigidity of these needles ensures that they maintain their shape during insertion, reducing the risk of bending or breaking. Both soft and rigid needles are available in various gauges and lengths, allowing healthcare providers to select the most appropriate needle for each specific procedure. The choice between soft and rigid needles often depends on the patient's condition, the type of procedure being performed, and the healthcare provider's preference. In recent years, there has been a growing emphasis on the development of needles that incorporate safety features, such as retractable or shielded designs, to prevent needle stick injuries and enhance patient safety. These innovations are particularly important in the context of the Global Venipuncture Needle Market, where the demand for safer and more efficient needles continues to rise. As healthcare systems around the world strive to improve patient outcomes and reduce the risk of complications, the role of both soft and rigid needles in the venipuncture process remains critical. Manufacturers are continually exploring new materials and technologies to enhance the performance and safety of these needles, ensuring that they meet the evolving needs of healthcare providers and patients alike. The Global Venipuncture Needle Market is poised for continued growth as advancements in medical technology and increasing healthcare demands drive the need for high-quality, reliable venipuncture solutions.

Hospital and Clinics, Diagnostic Centers, Others in the Global Venipuncture Needle Market:

The usage of venipuncture needles is widespread across various healthcare settings, including hospitals and clinics, diagnostic centers, and other medical facilities. In hospitals and clinics, venipuncture needles are indispensable tools for a wide range of medical procedures. They are used for drawing blood samples for laboratory tests, administering intravenous medications, and conducting blood transfusions. The efficiency and reliability of venipuncture needles are crucial in these settings, as they directly impact patient care and treatment outcomes. In diagnostic centers, venipuncture needles play a vital role in the collection of blood samples for various diagnostic tests. These centers rely on the accuracy and precision of venipuncture needles to obtain high-quality samples that can be analyzed for a wide range of medical conditions. The demand for venipuncture needles in diagnostic centers is driven by the increasing prevalence of chronic diseases and the growing emphasis on preventive healthcare. In addition to hospitals, clinics, and diagnostic centers, venipuncture needles are also used in other medical settings, such as blood donation centers and research laboratories. In blood donation centers, venipuncture needles are essential for collecting blood from donors, ensuring that the process is safe and efficient. Research laboratories also utilize venipuncture needles for various studies and experiments, where precise blood sampling is required. The versatility and reliability of venipuncture needles make them indispensable tools in the healthcare industry, supporting a wide range of medical procedures and contributing to improved patient outcomes. As the demand for healthcare services continues to grow, the Global Venipuncture Needle Market is expected to expand, driven by the need for high-quality, reliable venipuncture solutions in various medical settings.

Global Venipuncture Needle Market Outlook:

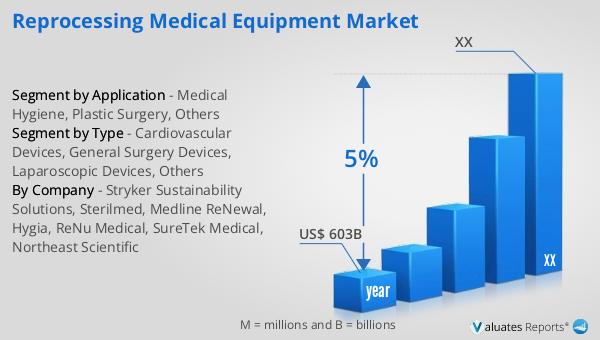

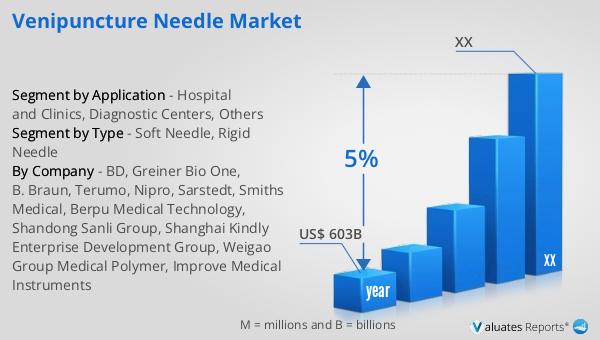

Based on our analysis, the global market for medical devices is projected to reach approximately $603 billion in 2023. This substantial market size reflects the growing demand for medical devices across various healthcare sectors. Over the next six years, the market is anticipated to experience a compound annual growth rate (CAGR) of 5%. This growth trajectory underscores the increasing reliance on medical devices to enhance patient care, improve diagnostic accuracy, and streamline therapeutic interventions. The expansion of the medical device market is driven by several factors, including technological advancements, rising healthcare expenditures, and the growing prevalence of chronic diseases. As healthcare systems worldwide strive to improve patient outcomes and reduce healthcare costs, the demand for innovative and efficient medical devices continues to rise. The Global Venipuncture Needle Market, as a segment of the broader medical device industry, is poised to benefit from these trends, with increasing demand for high-quality, reliable venipuncture solutions in various healthcare settings. The projected growth of the medical device market highlights the critical role that these devices play in modern healthcare, supporting a wide range of medical procedures and contributing to improved patient outcomes.

| Report Metric | Details |

| Report Name | Venipuncture Needle Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | BD, Greiner Bio One, B. Braun, Terumo, Nipro, Sarstedt, Smiths Medical, Berpu Medical Technology, Shandong Sanli Group, Shanghai Kindly Enterprise Development Group, Weigao Group Medical Polymer, Improve Medical Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |