What is Global LSI Test Probe Card Market?

The Global LSI Test Probe Card Market is an essential segment within the semiconductor industry, focusing on the tools used for testing integrated circuits (ICs) during the manufacturing process. These probe cards are critical for ensuring the functionality and reliability of semiconductor devices before they are packaged and shipped to customers. As the demand for more advanced and miniaturized electronic devices grows, the need for efficient and precise testing solutions becomes increasingly important. The market encompasses various types of probe cards, each designed to cater to specific testing requirements and technological advancements. With the rapid evolution of semiconductor technology, the Global LSI Test Probe Card Market is poised to play a crucial role in supporting the development and production of next-generation electronic devices. This market is driven by the continuous innovation in semiconductor manufacturing processes and the increasing complexity of IC designs, which necessitate more sophisticated testing solutions to maintain high quality and performance standards. As a result, the Global LSI Test Probe Card Market is expected to experience significant growth, driven by the ongoing advancements in semiconductor technology and the rising demand for high-performance electronic devices across various industries.

Cantilever Probe Card, Vertical Probe Card, MEMS Probe Card, Others in the Global LSI Test Probe Card Market:

Cantilever Probe Cards are one of the most traditional types of probe cards used in the Global LSI Test Probe Card Market. These cards feature a simple design where the probes are arranged in a cantilever fashion, allowing them to make contact with the semiconductor wafer. Cantilever probe cards are known for their durability and cost-effectiveness, making them a popular choice for testing less complex ICs. However, as semiconductor technology advances, the limitations of cantilever probe cards, such as their inability to handle high pin counts and fine pitches, have become more apparent. This has led to the development of more advanced probe card technologies to meet the demands of modern semiconductor testing. Vertical Probe Cards, on the other hand, are designed to address some of the limitations of cantilever probe cards. These cards feature a vertical arrangement of probes, which allows for higher pin counts and finer pitches. Vertical probe cards are particularly well-suited for testing advanced ICs with complex designs and high-density interconnections. They offer improved performance and accuracy compared to cantilever probe cards, making them a preferred choice for testing cutting-edge semiconductor devices. The development of vertical probe cards has been driven by the need for more precise and efficient testing solutions in the semiconductor industry. MEMS (Micro-Electro-Mechanical Systems) Probe Cards represent a significant advancement in probe card technology. These cards utilize MEMS technology to create highly precise and reliable probes that can handle the demands of modern semiconductor testing. MEMS probe cards offer several advantages over traditional probe card designs, including higher accuracy, better repeatability, and the ability to test at higher frequencies. They are particularly well-suited for testing advanced semiconductor devices with complex architectures and high-performance requirements. The adoption of MEMS probe cards is expected to grow as the semiconductor industry continues to push the boundaries of technology and performance. In addition to these main types of probe cards, there are also other specialized probe card designs that cater to specific testing needs. These may include advanced probe cards with unique configurations or materials designed to address particular challenges in semiconductor testing. As the Global LSI Test Probe Card Market continues to evolve, the development of new and innovative probe card technologies will be essential to meet the ever-changing demands of the semiconductor industry. The ongoing advancements in probe card technology are expected to play a crucial role in supporting the growth and development of the semiconductor market, enabling the production of more advanced and reliable electronic devices.

Integrated Device Manufacturer (IDMs), Semiconductor Assembly and Test (OSAT) in the Global LSI Test Probe Card Market:

The Global LSI Test Probe Card Market plays a vital role in the operations of Integrated Device Manufacturers (IDMs) and Semiconductor Assembly and Test (OSAT) companies. IDMs are companies that design, manufacture, and sell integrated circuits, handling the entire semiconductor production process from start to finish. For IDMs, the use of probe cards is crucial in ensuring the quality and reliability of their semiconductor products. Probe cards are used during the wafer testing phase to verify the functionality of the ICs before they are packaged and shipped to customers. This testing process is essential for maintaining high quality standards and minimizing the risk of defects in the final products. As IDMs continue to develop more advanced and complex semiconductor devices, the demand for sophisticated probe card solutions is expected to grow. Semiconductor Assembly and Test (OSAT) companies, on the other hand, specialize in the assembly, packaging, and testing of semiconductor devices. These companies often work with multiple semiconductor manufacturers, providing them with the necessary testing and packaging services to ensure the quality and performance of their products. For OSAT companies, the use of probe cards is critical in the testing phase, where they verify the functionality and reliability of the semiconductor devices before they are packaged and delivered to customers. The Global LSI Test Probe Card Market provides OSAT companies with the advanced testing solutions they need to meet the demands of their clients and maintain high quality standards. As the semiconductor industry continues to evolve, the role of probe cards in the operations of IDMs and OSAT companies is becoming increasingly important. The ongoing advancements in probe card technology are enabling these companies to test more complex and advanced semiconductor devices with greater accuracy and efficiency. This is essential for maintaining the competitiveness of IDMs and OSAT companies in the rapidly changing semiconductor market. As a result, the Global LSI Test Probe Card Market is expected to experience significant growth, driven by the increasing demand for high-performance testing solutions in the semiconductor industry. The collaboration between probe card manufacturers, IDMs, and OSAT companies is crucial in driving innovation and ensuring the continued success of the semiconductor market.

Global LSI Test Probe Card Market Outlook:

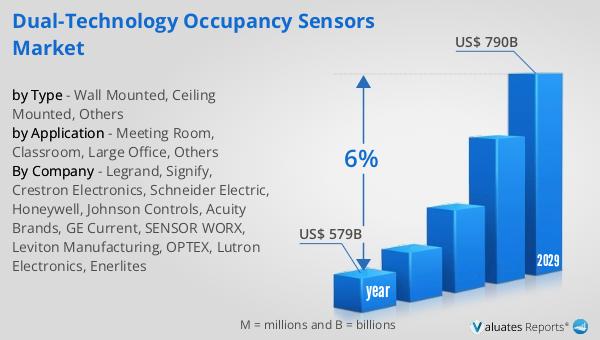

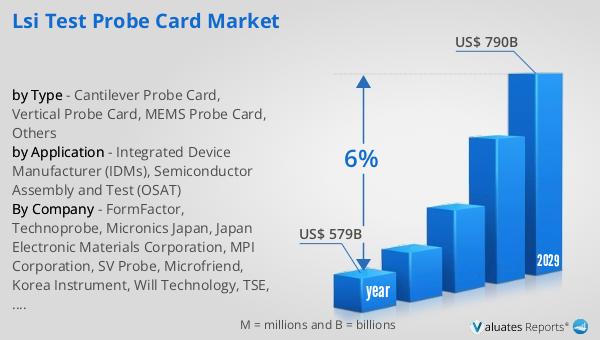

In 2022, the global semiconductor market was valued at approximately $579 billion. This figure is projected to rise significantly, reaching an estimated $790 billion by 2029. This growth trajectory represents a compound annual growth rate (CAGR) of 6% over the forecast period. The expansion of the semiconductor market is driven by several factors, including the increasing demand for advanced electronic devices, the proliferation of IoT (Internet of Things) applications, and the ongoing advancements in semiconductor technology. As the world becomes more interconnected and reliant on digital technologies, the demand for semiconductors is expected to continue its upward trend. The growth of the semiconductor market is also supported by the increasing adoption of artificial intelligence (AI), machine learning, and other emerging technologies that require high-performance semiconductor solutions. As a result, the Global LSI Test Probe Card Market is poised to benefit from this growth, as the demand for advanced testing solutions will rise in tandem with the expansion of the semiconductor market. The ongoing innovation in probe card technology will be essential in supporting the development and production of next-generation semiconductor devices, ensuring their quality and reliability in an increasingly competitive market.

| Report Metric | Details |

| Report Name | LSI Test Probe Card Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | FormFactor, Technoprobe, Micronics Japan, Japan Electronic Materials Corporation, MPI Corporation, SV Probe, Microfriend, Korea Instrument, Will Technology, TSE, Feinmetall, Synergie Cad Probe, TIPS Messtechnik GmbH, STAr Technologies, Inc., MaxOne, Shenzhen DGT, Suzhou Silicon Test System, SPEA, Probecard Technology, Suzhou UIGreen Science and Technology, FastPrint, MMK |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |