What is Global Frameless Full Glass Balcony Railings Market?

The Global Frameless Full Glass Balcony Railings Market represents a niche yet growing segment within the architectural and construction industries. These railings are characterized by their sleek, modern design, which eliminates the need for traditional frames, offering an unobstructed view and a minimalist aesthetic. This market is driven by the increasing demand for contemporary architectural designs that emphasize transparency and open spaces. Frameless full glass railings are particularly popular in urban areas where maximizing views and natural light is a priority. They are used in both residential and commercial buildings, providing safety without compromising on style. The market is also influenced by advancements in glass technology, which have improved the durability and safety of these railings, making them a viable option for various applications. As urbanization continues to rise, the demand for such innovative architectural solutions is expected to grow, further propelling the market.

Below 1/4 inch, 1/4-3/8 inch, 3/8-1/2 inch, Above 1/2 inch in the Global Frameless Full Glass Balcony Railings Market:

In the Global Frameless Full Glass Balcony Railings Market, the thickness of the glass used is a critical factor that influences both the aesthetic appeal and the structural integrity of the railings. Glass thickness is categorized into four main segments: below 1/4 inch, 1/4-3/8 inch, 3/8-1/2 inch, and above 1/2 inch. Each thickness category serves different purposes and is chosen based on specific requirements of strength, safety, and design. Glass below 1/4 inch is typically used in applications where weight is a concern, and the railing is not subjected to heavy loads or high impact. This thinner glass is often used in interior applications or in areas where the railing is more decorative than functional. However, it offers less resistance to impact and may not be suitable for high-traffic areas. The 1/4-3/8 inch category is more robust and is commonly used in residential settings where moderate strength is required. This thickness provides a balance between weight and durability, making it a popular choice for homeowners looking to enhance their property's aesthetic without compromising safety. The 3/8-1/2 inch glass is a standard choice for both residential and commercial applications. It offers a higher level of safety and can withstand greater impact, making it suitable for balconies and terraces that experience regular use. This thickness is often preferred in commercial settings where safety regulations are stringent, and the risk of impact is higher. Glass above 1/2 inch is the thickest category and is used in high-risk areas where maximum safety is paramount. This includes high-rise buildings, commercial complexes, and areas exposed to extreme weather conditions. The added thickness provides superior strength and impact resistance, ensuring the safety of occupants and passersby. Additionally, thicker glass can also offer better sound insulation, which is an added advantage in noisy urban environments. The choice of glass thickness in frameless full glass balcony railings is a crucial decision that impacts not only the safety and functionality of the railing but also its aesthetic appeal. As such, manufacturers and designers must carefully consider the specific needs of each project to select the appropriate glass thickness.

Residential, Commercial in the Global Frameless Full Glass Balcony Railings Market:

The usage of Global Frameless Full Glass Balcony Railings Market in residential and commercial areas highlights the versatility and appeal of these modern architectural elements. In residential settings, frameless full glass railings are increasingly popular for their ability to enhance the aesthetic appeal of homes while providing safety and functionality. Homeowners appreciate the unobstructed views these railings offer, allowing them to enjoy their surroundings without visual barriers. This is particularly beneficial in homes with scenic views, such as those overlooking the ocean, mountains, or cityscapes. The transparency of the glass also allows for more natural light to enter the home, creating a brighter and more inviting living space. In addition to their aesthetic benefits, frameless glass railings are also valued for their low maintenance requirements. Unlike traditional railings that may require regular painting or staining, glass railings are easy to clean and maintain, making them a practical choice for busy homeowners. In commercial settings, frameless full glass railings are used to create a modern and sophisticated atmosphere. They are commonly found in office buildings, shopping malls, hotels, and restaurants, where they contribute to an open and airy environment. The sleek design of these railings complements contemporary architectural styles and can enhance the overall ambiance of a commercial space. In addition to their aesthetic appeal, frameless glass railings also provide safety and security in commercial environments. They are often used in areas with high foot traffic, such as staircases, balconies, and terraces, where they help prevent accidents while maintaining a stylish appearance. The use of tempered or laminated glass in these railings ensures that they are strong and durable, capable of withstanding the demands of a busy commercial setting. Furthermore, frameless glass railings can be customized to meet the specific needs of a commercial space, with options for different glass thicknesses, finishes, and hardware. This flexibility allows businesses to create a unique and personalized look that aligns with their brand identity. Overall, the use of frameless full glass balcony railings in both residential and commercial areas underscores their appeal as a modern and functional design element.

Global Frameless Full Glass Balcony Railings Market Outlook:

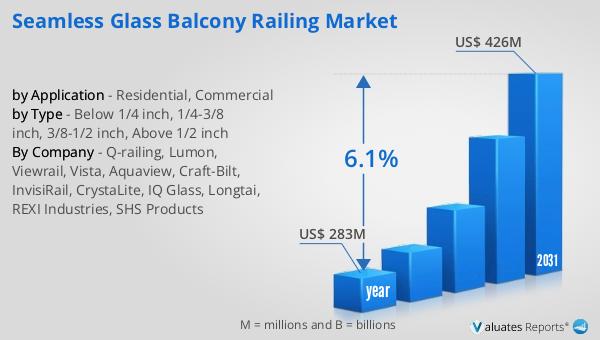

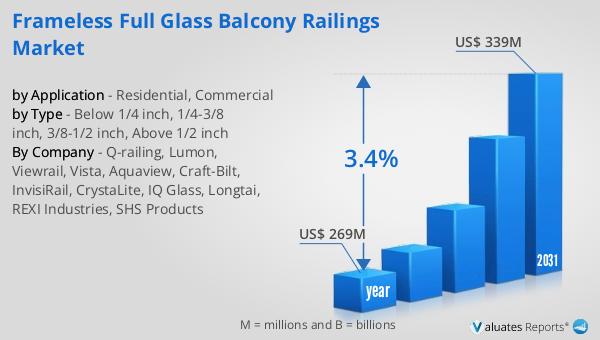

The global market for Frameless Full Glass Balcony Railings was valued at approximately $269 million in 2024, and it is anticipated to expand to a revised size of around $339 million by 2031. This growth trajectory reflects a compound annual growth rate (CAGR) of 3.4% over the forecast period. The market's expansion is indicative of the increasing demand for modern architectural solutions that prioritize aesthetics and functionality. Frameless full glass railings are gaining popularity due to their ability to provide unobstructed views and a sleek, contemporary look, which is highly sought after in both residential and commercial construction projects. The market is also characterized by a competitive landscape, with the top four manufacturers holding a combined market share of about 30%. This concentration of market power suggests that these leading companies have a significant influence on market trends and innovations. As the market continues to grow, it is likely that these manufacturers will continue to play a pivotal role in shaping the future of frameless full glass balcony railings. The projected growth of this market underscores the ongoing shift towards modern architectural designs that emphasize transparency, open spaces, and a seamless integration with the surrounding environment.

| Report Metric | Details |

| Report Name | Frameless Full Glass Balcony Railings Market |

| Accounted market size in year | US$ 269 million |

| Forecasted market size in 2031 | US$ 339 million |

| CAGR | 3.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Q-railing, Lumon, Viewrail, Vista, Aquaview, Craft-Bilt, InvisiRail, CrystaLite, IQ Glass, Longtai, REXI Industries, SHS Products |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |