What is Global Wet Electronic Chemicals for Integrated Circuits Market?

The Global Wet Electronic Chemicals for Integrated Circuits Market is a specialized segment within the broader chemical industry, focusing on the production and supply of chemicals used in the manufacturing of integrated circuits (ICs). These chemicals are crucial in the semiconductor fabrication process, where they are used for cleaning, etching, and other processes that require high precision and purity. The market is driven by the increasing demand for electronic devices, which in turn fuels the need for more advanced and efficient ICs. As technology continues to evolve, the complexity of ICs increases, necessitating the use of high-quality wet electronic chemicals to ensure optimal performance and reliability. The market is characterized by rapid technological advancements and a high degree of competition among key players, who are constantly innovating to meet the stringent requirements of the semiconductor industry. The growth of this market is also supported by the expansion of the electronics industry in emerging economies, where the demand for consumer electronics and advanced technologies is on the rise. Overall, the Global Wet Electronic Chemicals for Integrated Circuits Market plays a vital role in the electronics supply chain, ensuring the production of high-performance and reliable electronic components.

General Wet Electronic Chemicals, Functional Wet Electronic Chemicals in the Global Wet Electronic Chemicals for Integrated Circuits Market:

General Wet Electronic Chemicals are a broad category of chemicals used in various stages of semiconductor manufacturing. These chemicals include acids, bases, solvents, and other compounds that are essential for cleaning, etching, and developing processes in the production of integrated circuits. The primary function of these chemicals is to prepare the silicon wafers for subsequent processing steps by removing impurities and creating the desired patterns on the wafer surface. For instance, acids like hydrofluoric acid are used for etching silicon dioxide layers, while solvents are employed to clean the wafers and remove any organic residues. The quality and purity of these chemicals are critical, as any contamination can lead to defects in the final product, affecting the performance and reliability of the integrated circuits. On the other hand, Functional Wet Electronic Chemicals are more specialized and are designed to perform specific functions in the semiconductor manufacturing process. These chemicals include photoresists, developers, and strippers, which are used in the photolithography process to create intricate patterns on the silicon wafers. Photoresists are light-sensitive materials that form a protective layer on the wafer, allowing selective exposure to light to create the desired circuit patterns. Developers are then used to remove the exposed or unexposed areas of the photoresist, depending on the type of photoresist used. Strippers are employed to remove the remaining photoresist after the etching process is complete. The development of these functional chemicals requires a deep understanding of the semiconductor manufacturing process and the specific requirements of each application. Manufacturers of wet electronic chemicals must continuously innovate to keep up with the rapid advancements in semiconductor technology, ensuring that their products meet the ever-increasing demands for precision and performance. The Global Wet Electronic Chemicals for Integrated Circuits Market is highly competitive, with numerous players vying for market share by offering a wide range of products tailored to the needs of semiconductor manufacturers. Companies in this market invest heavily in research and development to create new formulations and improve existing products, aiming to enhance the efficiency and effectiveness of their chemicals. The market is also influenced by regulatory requirements, as the use of certain chemicals is subject to strict environmental and safety regulations. Manufacturers must ensure compliance with these regulations while maintaining the quality and performance of their products. In summary, General and Functional Wet Electronic Chemicals are indispensable components of the semiconductor manufacturing process, playing a crucial role in the production of high-performance integrated circuits. The Global Wet Electronic Chemicals for Integrated Circuits Market is driven by the continuous demand for advanced electronic devices and the need for more efficient and reliable semiconductor manufacturing processes.

Consumer Electronics, Semiconductor, Photovoltaic Solar, LED in the Global Wet Electronic Chemicals for Integrated Circuits Market:

The usage of Global Wet Electronic Chemicals for Integrated Circuits Market spans several key areas, including consumer electronics, semiconductors, photovoltaic solar, and LED technologies. In the realm of consumer electronics, these chemicals are vital for the production of integrated circuits that power a wide range of devices, from smartphones and tablets to laptops and wearable technology. The demand for smaller, faster, and more efficient electronic devices drives the need for high-quality wet electronic chemicals that can support the production of advanced integrated circuits with intricate designs and high performance. In the semiconductor industry, wet electronic chemicals are used throughout the fabrication process, from wafer cleaning and etching to photolithography and doping. These chemicals are essential for creating the precise patterns and structures required for modern integrated circuits, which are the building blocks of all electronic devices. The semiconductor industry is characterized by rapid technological advancements, and the demand for more powerful and efficient chips continues to grow, driving the need for innovative wet electronic chemicals that can meet the stringent requirements of semiconductor manufacturers. In the photovoltaic solar industry, wet electronic chemicals are used in the production of solar cells, which convert sunlight into electricity. These chemicals are employed in various stages of the manufacturing process, including wafer cleaning, texturing, and doping, to enhance the efficiency and performance of solar cells. As the demand for renewable energy sources increases, the photovoltaic solar industry continues to expand, creating new opportunities for the Global Wet Electronic Chemicals for Integrated Circuits Market. Finally, in the LED industry, wet electronic chemicals are used in the production of light-emitting diodes, which are widely used in lighting, displays, and other applications. These chemicals are essential for creating the precise patterns and structures required for LED chips, which are known for their energy efficiency and long lifespan. The growing demand for energy-efficient lighting solutions and high-quality displays drives the need for advanced wet electronic chemicals that can support the production of high-performance LED chips. In conclusion, the Global Wet Electronic Chemicals for Integrated Circuits Market plays a crucial role in supporting the growth and development of several key industries, including consumer electronics, semiconductors, photovoltaic solar, and LED technologies. The demand for advanced electronic devices and renewable energy solutions continues to drive the need for high-quality wet electronic chemicals that can meet the stringent requirements of these industries.

Global Wet Electronic Chemicals for Integrated Circuits Market Outlook:

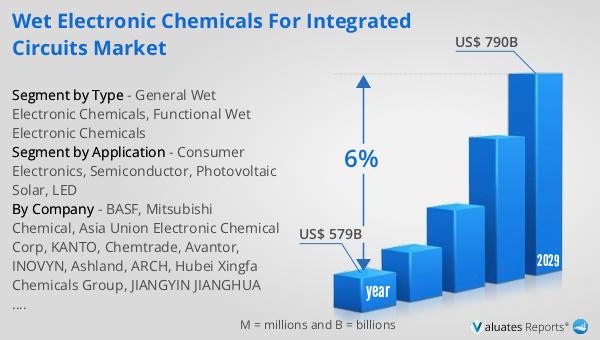

The global semiconductor market, valued at approximately $579 billion in 2022, is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth trajectory underscores the increasing demand for semiconductors, which are integral to a wide array of electronic devices and systems. The expansion of the semiconductor market is driven by several factors, including the proliferation of consumer electronics, advancements in technology, and the growing adoption of renewable energy solutions. As the world becomes more interconnected and reliant on digital technologies, the demand for semiconductors continues to rise, fueling the need for innovative and efficient manufacturing processes. The Global Wet Electronic Chemicals for Integrated Circuits Market plays a pivotal role in supporting this growth by providing the essential chemicals required for semiconductor fabrication. These chemicals are crucial for ensuring the precision and performance of integrated circuits, which are the building blocks of all electronic devices. As the semiconductor market continues to expand, the demand for high-quality wet electronic chemicals is expected to grow, driving innovation and competition within the industry. The future of the semiconductor market looks promising, with continued advancements in technology and increasing demand for electronic devices and renewable energy solutions.

| Report Metric | Details |

| Report Name | Wet Electronic Chemicals for Integrated Circuits Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | BASF, Mitsubishi Chemical, Asia Union Electronic Chemical Corp, KANTO, Chemtrade, Avantor, INOVYN, Ashland, ARCH, Hubei Xingfa Chemicals Group, JIANGYIN JIANGHUA MICRO-ELECTRONIC MATERIALS, Grandit, Jiangsu Denoir Technology, Dow Chemical Company, Zhejiang Kaisn Fluorochemical, Crystal Clear Electronic Material |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |