What is Global Channel Loyalty Management Software Market?

The Global Channel Loyalty Management Software Market refers to the industry focused on developing and providing software solutions that help businesses manage and enhance their channel partner relationships. These software solutions are designed to improve partner engagement, streamline communication, and ultimately drive sales through various channels. By offering tools for tracking partner performance, managing incentives, and analyzing data, these platforms enable companies to build stronger, more productive partnerships. The market is driven by the increasing need for businesses to maintain competitive advantages and foster loyalty among their channel partners. As companies expand globally, the complexity of managing diverse partner networks grows, making channel loyalty management software an essential tool for success. This market encompasses a wide range of industries, including technology, manufacturing, retail, and more, each seeking to optimize their channel strategies and maximize returns on investment. The software solutions offered in this market can be tailored to meet the specific needs of different industries, ensuring that businesses can effectively manage their partner relationships and achieve their strategic goals. As a result, the Global Channel Loyalty Management Software Market continues to evolve, offering innovative solutions to meet the changing demands of businesses worldwide.

On-Premise, Cloud-based in the Global Channel Loyalty Management Software Market:

On-premise and cloud-based solutions are two primary deployment models for Global Channel Loyalty Management Software, each offering distinct advantages and considerations for businesses. On-premise solutions involve installing the software on a company's own servers and infrastructure. This model provides businesses with greater control over their data and software environment, as they can customize the system to meet their specific needs and security requirements. Companies with strict data privacy policies or those operating in regulated industries often prefer on-premise solutions because they can ensure compliance with internal and external standards. However, on-premise solutions typically require a significant upfront investment in hardware and software, as well as ongoing maintenance and IT support. This can be a barrier for smaller businesses or those with limited IT resources. Additionally, on-premise solutions may lack the flexibility and scalability of cloud-based alternatives, as they require physical infrastructure upgrades to accommodate growth or changes in business needs.

BFSI, Travel & Hospitality, Consumer goods & Retail, Other in the Global Channel Loyalty Management Software Market:

In contrast, cloud-based solutions offer a more flexible and scalable approach to channel loyalty management. These solutions are hosted on the vendor's servers and accessed via the internet, allowing businesses to quickly deploy and scale their software without the need for significant upfront investments. Cloud-based solutions are typically offered on a subscription basis, which can be more cost-effective for businesses with limited budgets or those looking to minimize capital expenditures. The cloud model also provides businesses with the ability to access their software from anywhere, making it easier for remote teams or global operations to collaborate and manage their channel relationships. Additionally, cloud-based solutions often come with automatic updates and maintenance, reducing the burden on internal IT teams and ensuring that businesses always have access to the latest features and security enhancements.

Global Channel Loyalty Management Software Market Outlook:

However, cloud-based solutions may raise concerns about data security and privacy, as businesses must trust their vendor to protect sensitive information. To address these concerns, many cloud providers offer robust security measures and compliance certifications to reassure customers. Ultimately, the choice between on-premise and cloud-based solutions depends on a company's specific needs, resources, and strategic goals. Businesses must carefully evaluate their requirements and consider factors such as cost, scalability, security, and ease of use when selecting a channel loyalty management software deployment model. As the Global Channel Loyalty Management Software Market continues to grow, both on-premise and cloud-based solutions will play a crucial role in helping businesses optimize their channel strategies and drive success.

| Report Metric | Details |

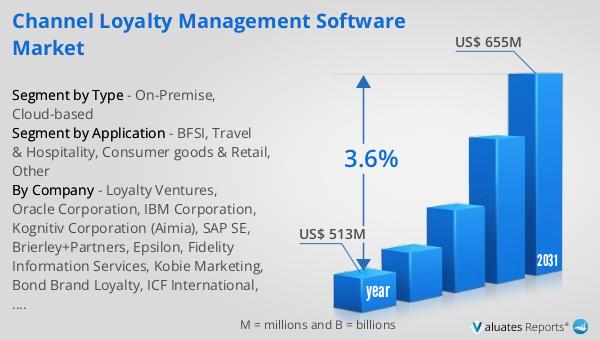

| Report Name | Channel Loyalty Management Software Market |

| Accounted market size in year | US$ 513 million |

| Forecasted market size in 2031 | US$ 655 million |

| CAGR | 3.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Loyalty Ventures, Oracle Corporation, IBM Corporation, Kognitiv Corporation (Aimia), SAP SE, Brierley+Partners, Epsilon, Fidelity Information Services, Kobie Marketing, Bond Brand Loyalty, ICF International, Tibco Software, Comarch |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |